Market Cap- 440 cr

PE- 25

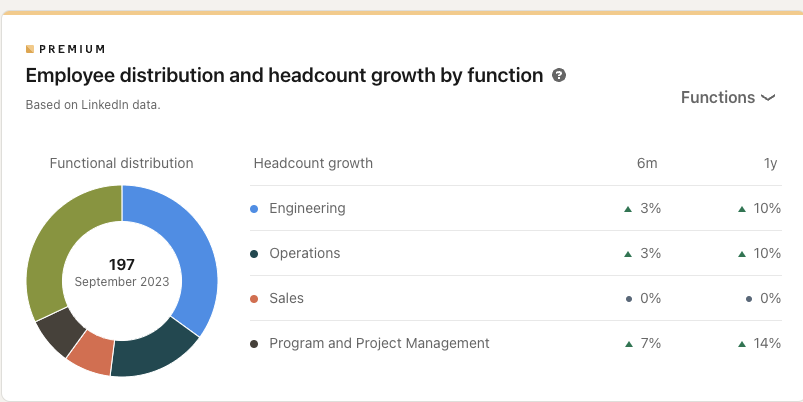

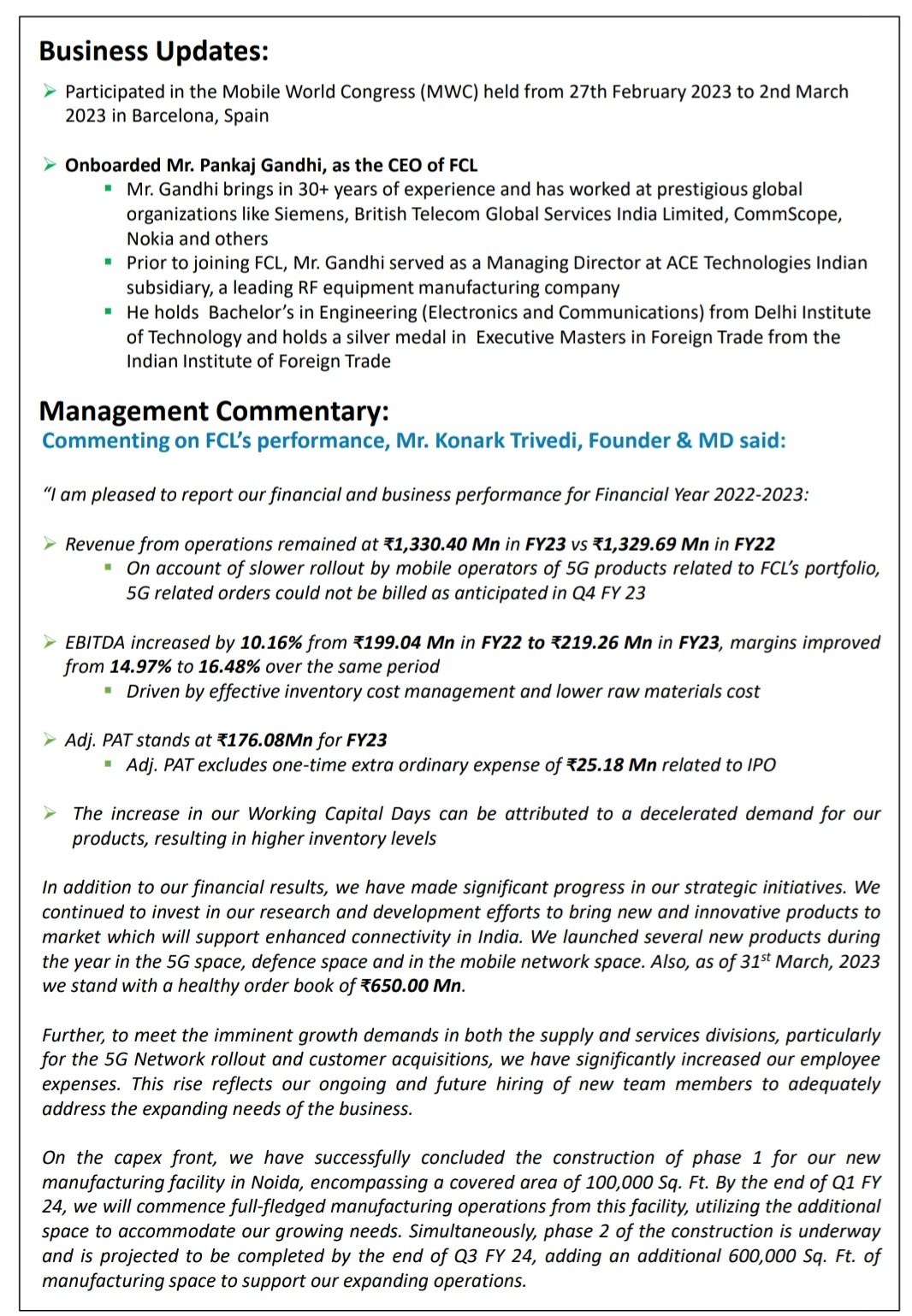

Newly appointed CEO- Pankaj Gandhi, he is formerly Managing Director, of the India subsidiary of ACE Technologies.

Read more at: Frog Cellsat Ltd appoints Pankaj Gandhi as the new CEO - CXOToday.com

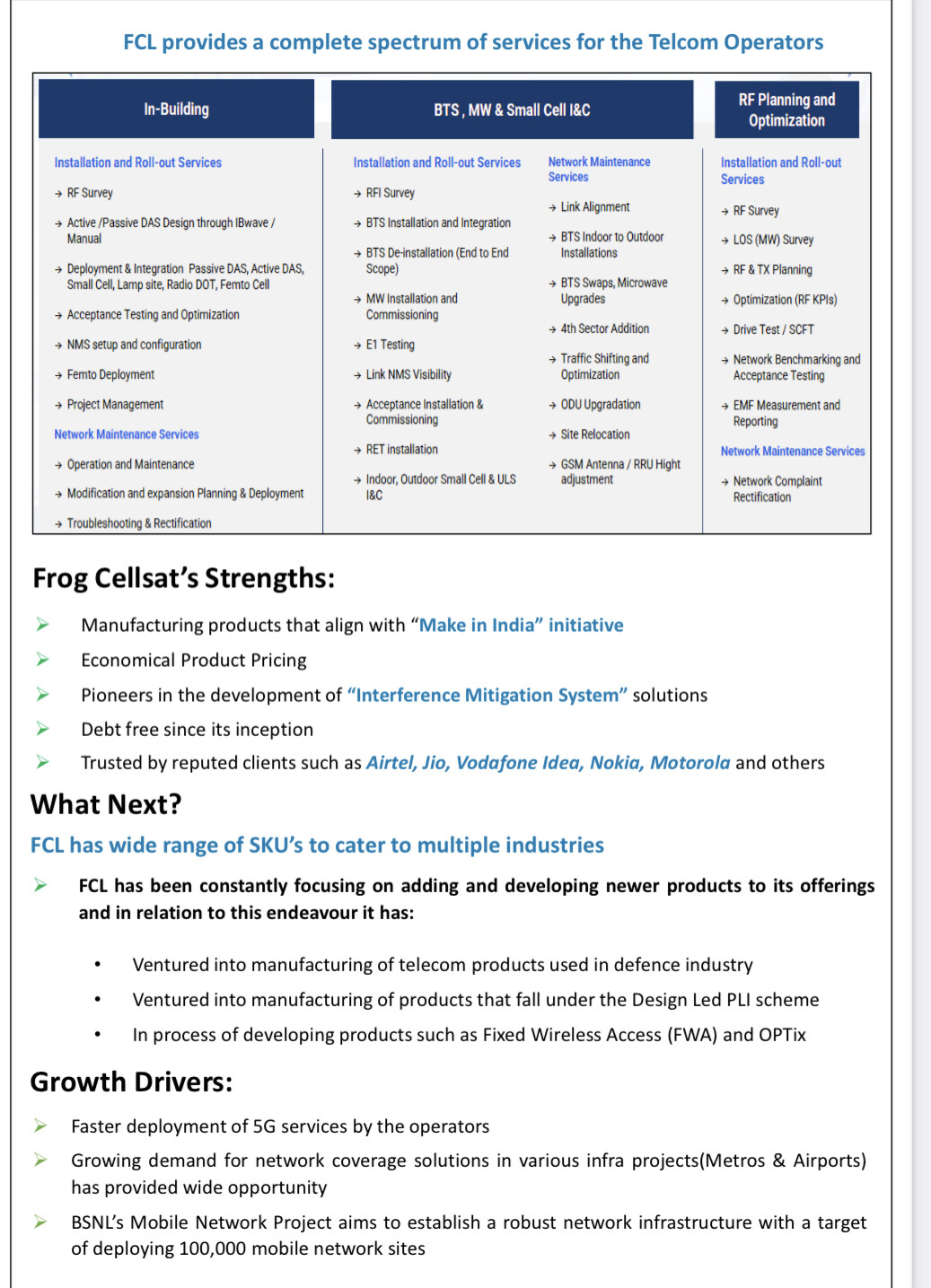

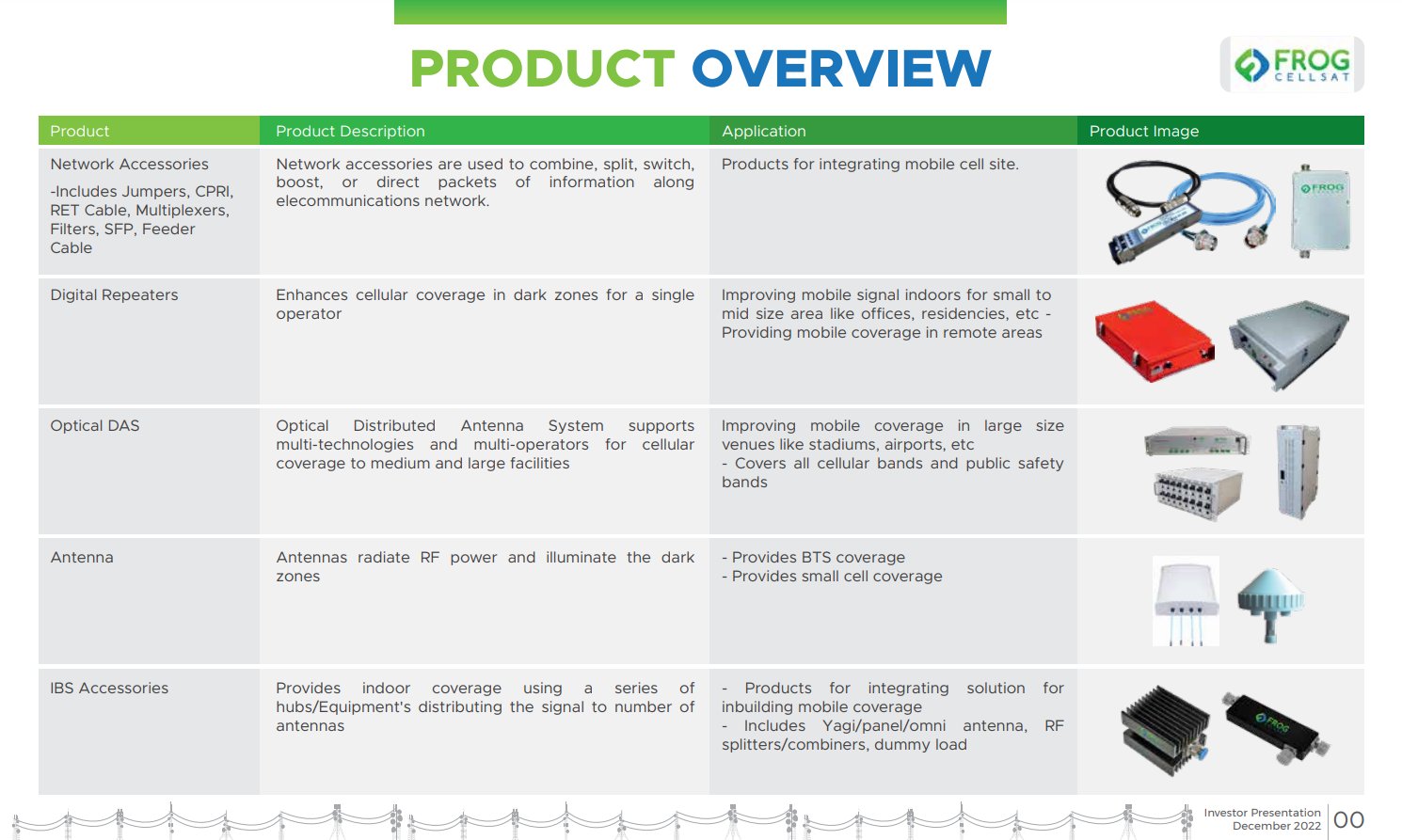

Frog Cellsat Pvt Ltd. design, manufacture and market cost-effective Repeater solutions for In-Building 2G, 3G, and 4G voice and data services for Mobile Operators.

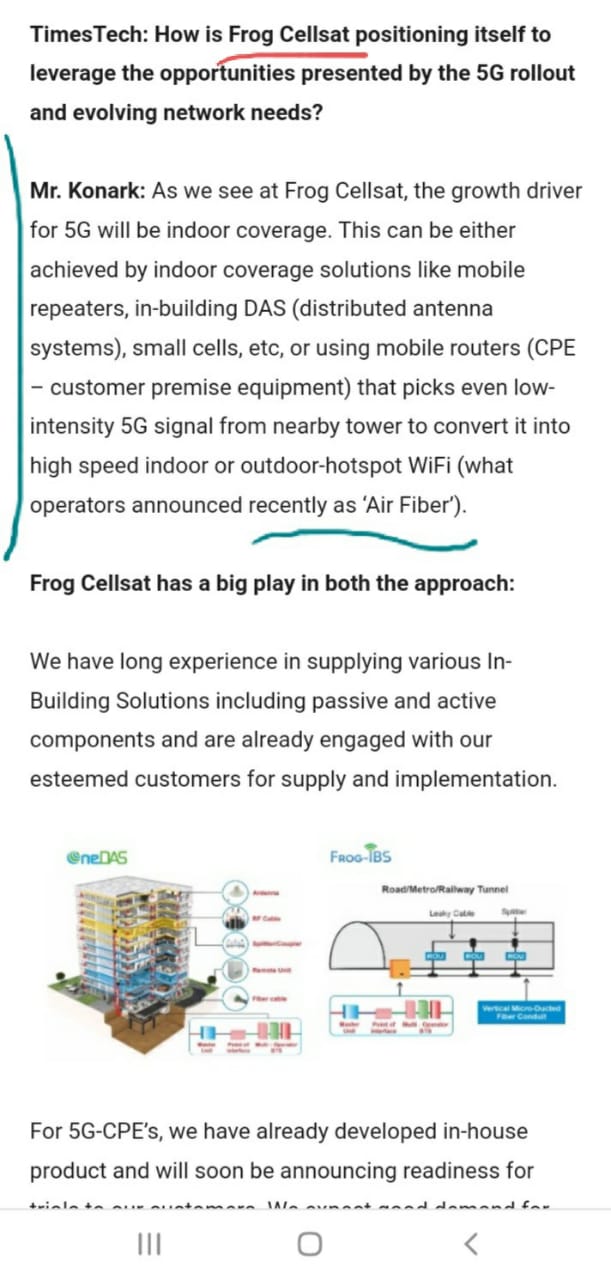

Frog Cellsat Ltd manufactures telecom equipment that goes into Telecom Towers such as 2G/3G/4G Multi-Band Digital RF Repeaters, Multi-band Frequency Shift Repeater, Multi-band Optical DAS systems, relative software, and accessories. It also offers In-Building Coverage Planning and Design services along with Radio Access Network (RAN) and Backhaul Network installation services.

The company’s customer list included Bharti Airtel, Voda-Idea, Jio, Nokia, Ericson, Adani, BSNL, etc.

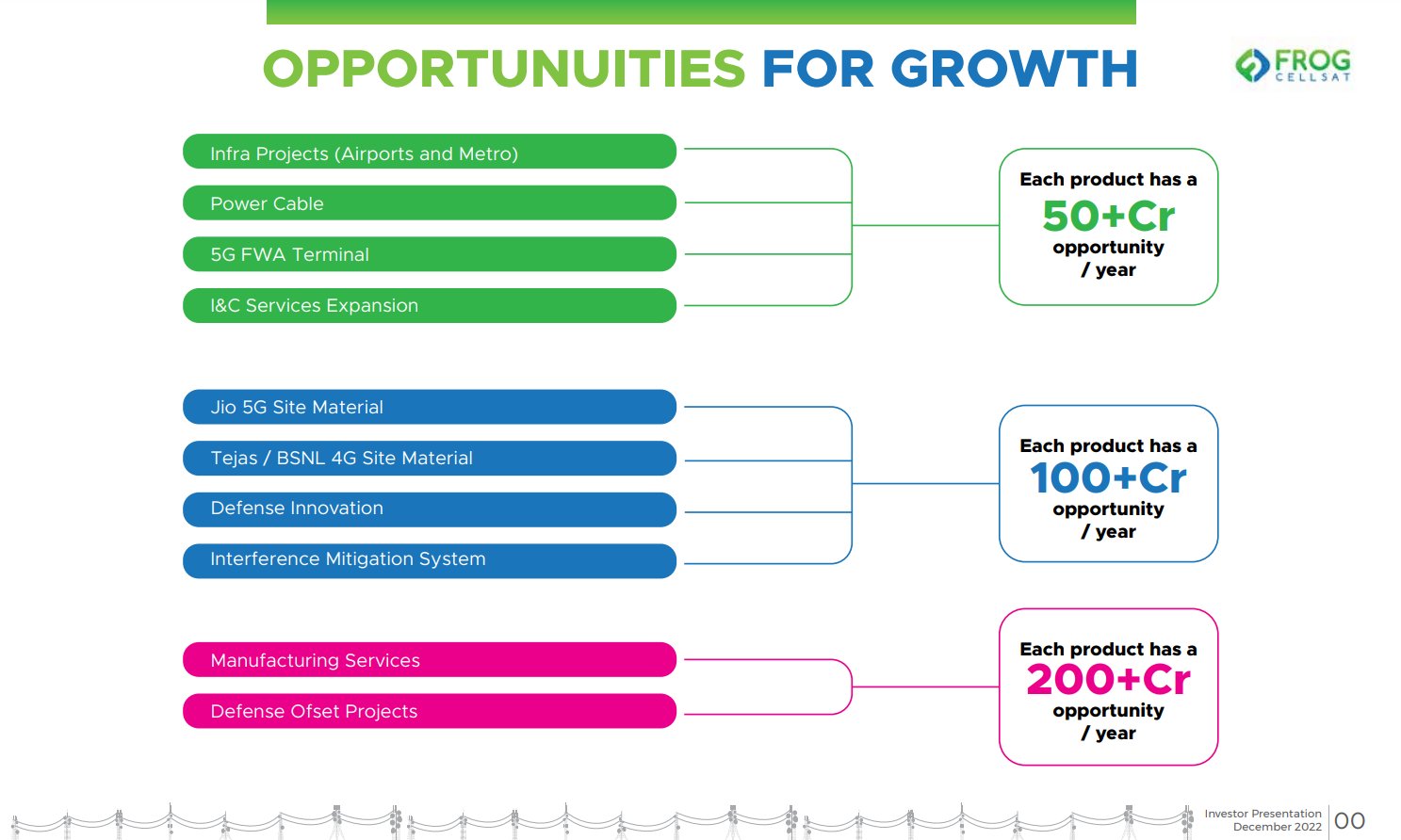

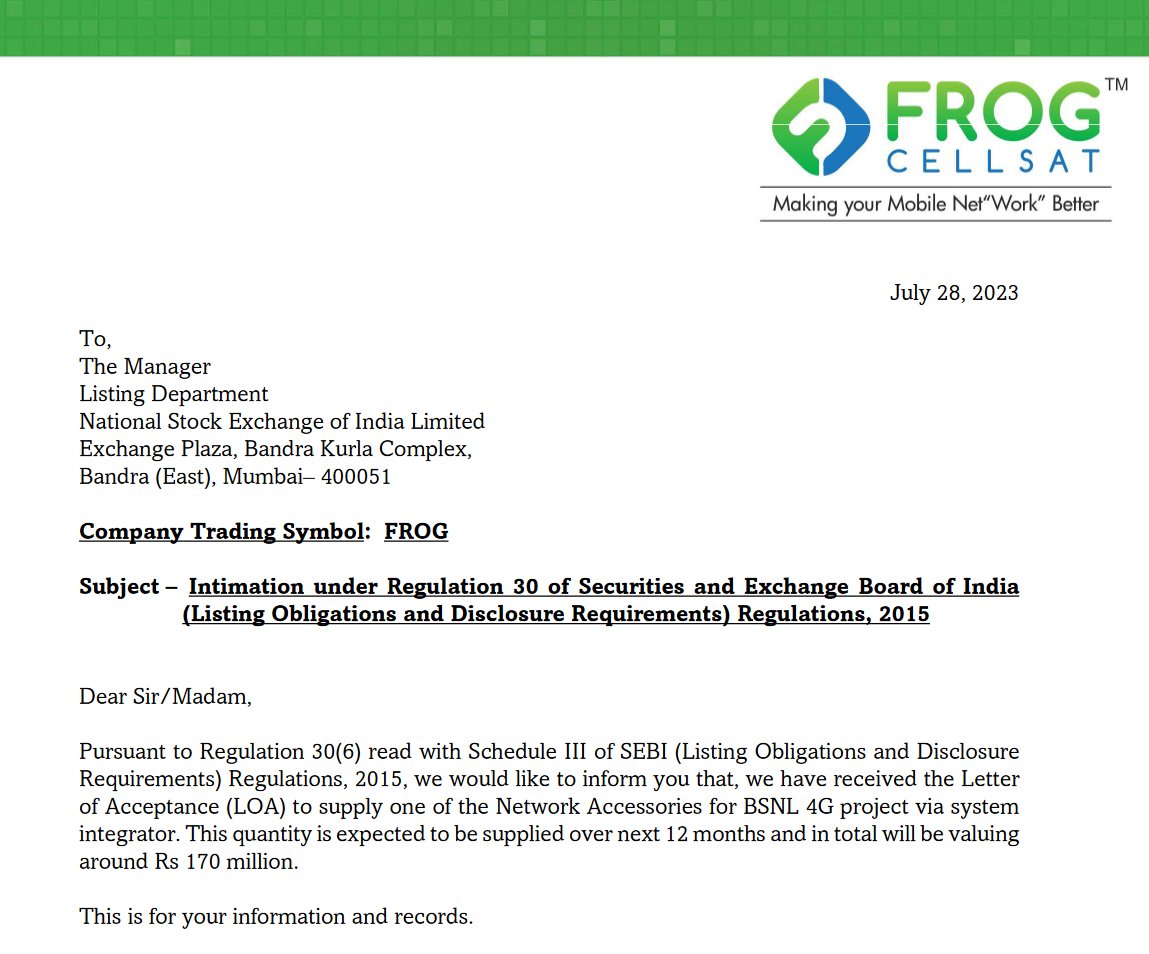

Recently they got order from BSNL for 4g equipment

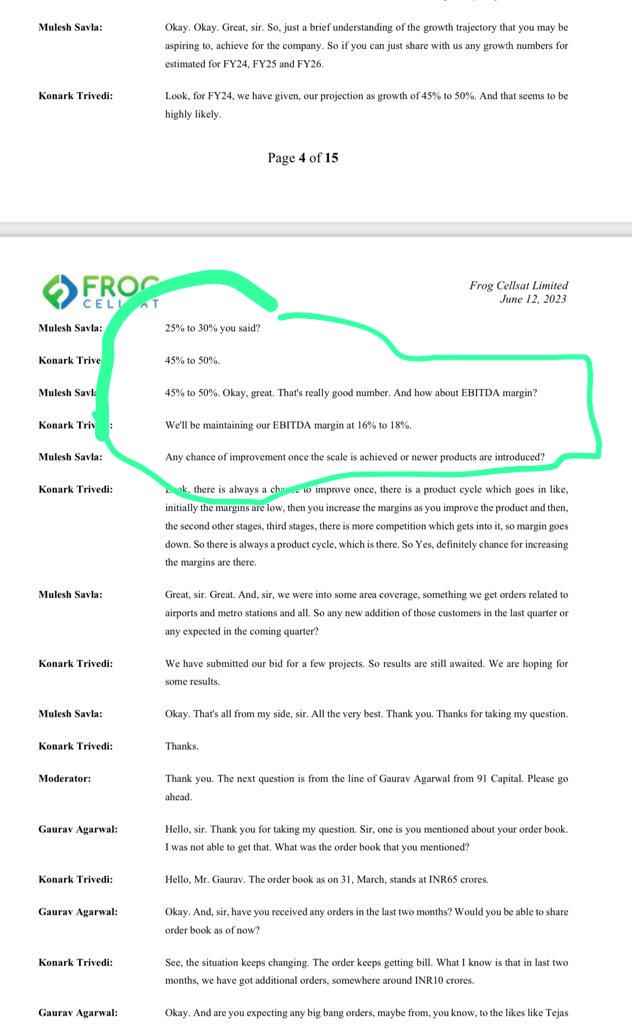

Order book- 65 + 17 cr (recent)=82 cr

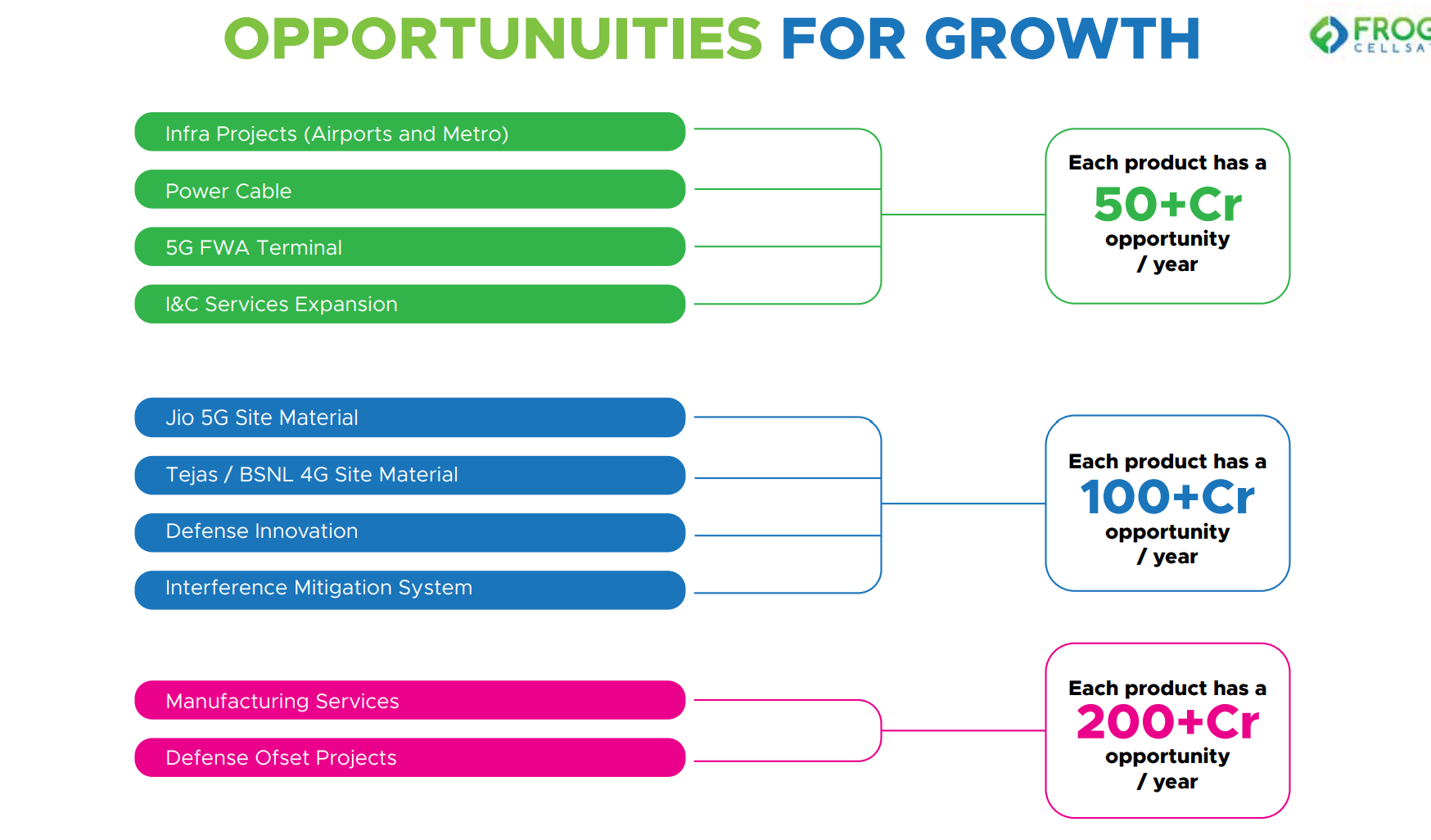

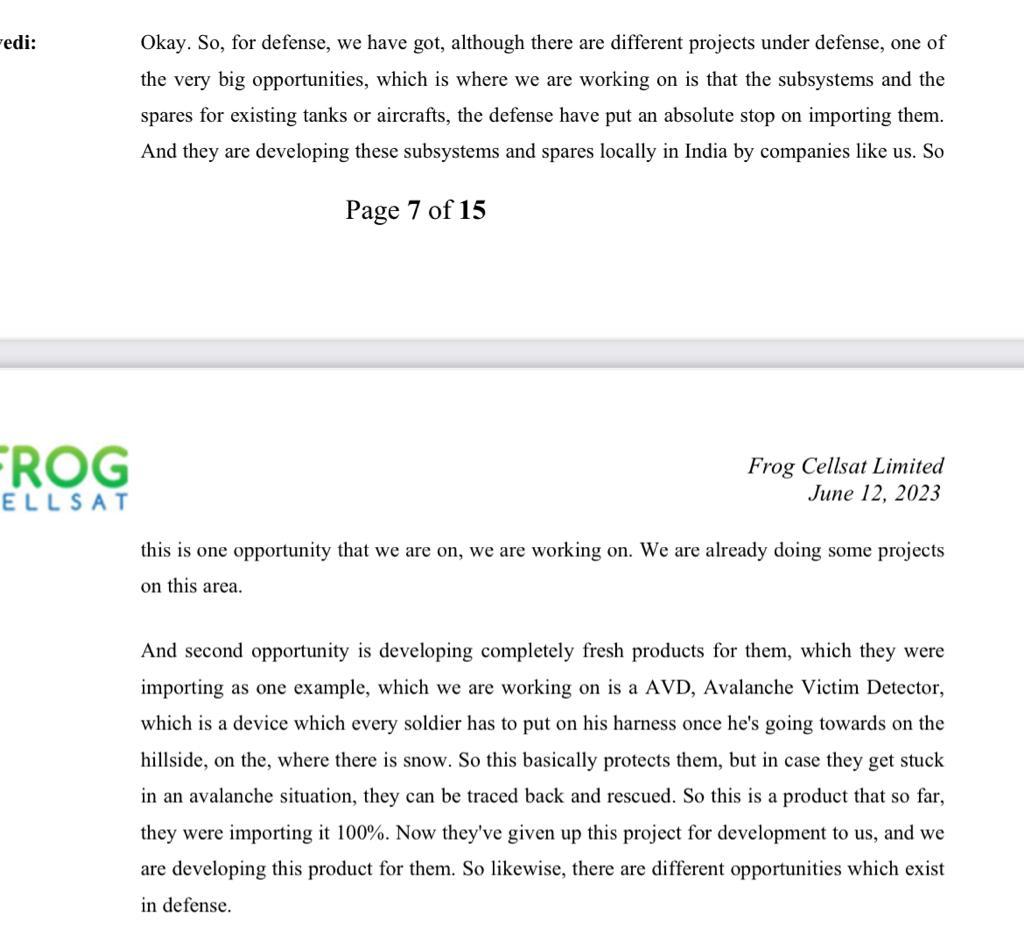

Solid R&D, Working for Defense Products

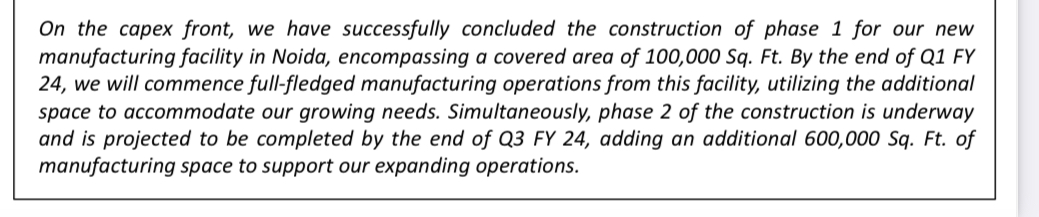

Good Expansion Plans with healthy guidance of 50% growth with 16-18% Ebidta

Working on many technology partnerships and technology transfer discussions are at a mature stage with reputed companies from UK, USA , etc- mentioned by management- Information

Anti-Thesis-

Client Concentration

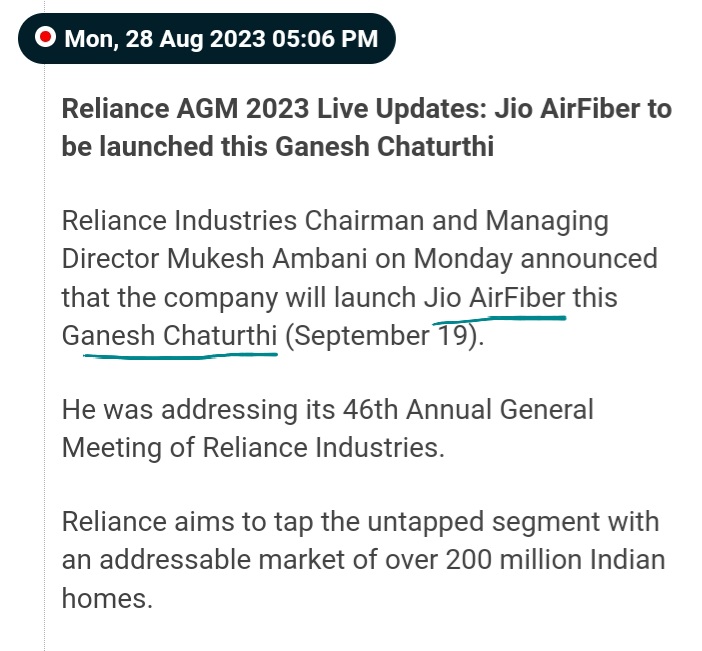

Slowdown in 5g launch in India

Healthy Competition in telecom

Please provide your thoughts on the same