Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

Read disclaimer for summaries here: https://goo.gl/HELov8

Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

Read disclaimer for summaries here: https://goo.gl/HELov8

as HFC SECTOR being widely dicussed since last 1-2 years at a length , and in euphoria as always happens majority of the HFC stock gave decent correction in last 6-7 months in the range of 10-45 % from peak .

does this correction changes the fundamental outlook on sector ??

i dont think so !!!

looking at HFC SECTOR as a whole good price correction has already happened.

considreing lic housing recent price low of 536 in dec 2017 is almost all time high it achieved in august 2015 of 526 !!!

as i have always believed that technical chart study on longer term pattern besides fundamental , work really well for investors , it gives good insight on price patterns & base formation or bottom formation process along with changes in fundamental picture of a stock/sector .

looking at technical picture of HFC SECTOR , it is reasonably appears that major price damage has happended already happend, sooner or later atleast a good bounce is in to offing ( if not new high ) ,

no one can exactly predict time/bottom price , but it is defintely a time to give serious look to LIC HOUSING FOR 2018 !!

LIC HFL during the last few months correction was trading at CMP 565 and Below, at P/E band of 14-15. Though this is not a fast growth business, as compared to Repco, Gruh, Canfin and HDFC; it has some positives at this price range.

Some Negatives :

Some Positives :

Thesis for Investing:

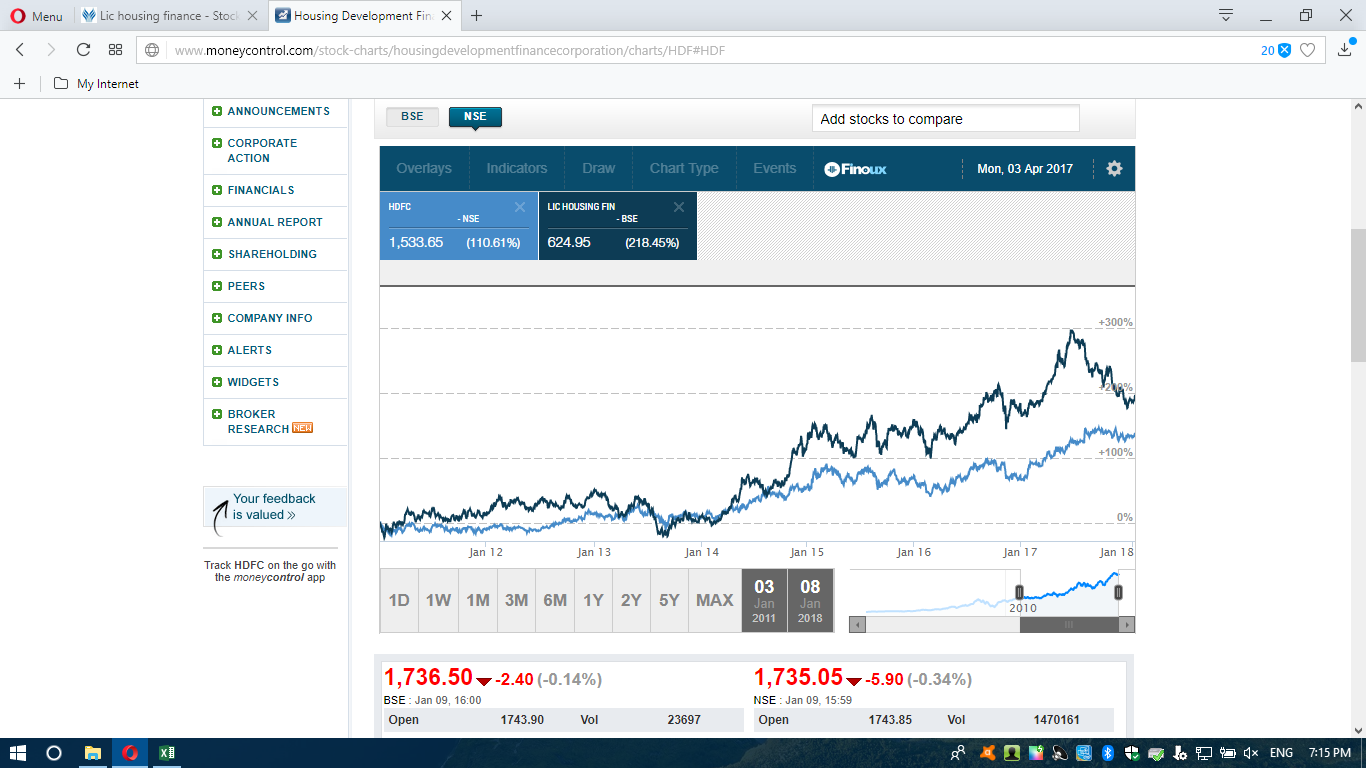

Graph showing higher Price CAGR between 2011 to 2018 in spite of recent correction:

Disc: Invested at 565 and lower levels.

LIC HFL has reported another flat quarter:

I am in the process of analyzing the result.

Disc: Invested.

At P/E=12 and P/B=1.8, LICHF again looks very attractive inspite of lower growth in FY18. In terms of valuation, it is at 4 yr low. Any view on this ?

My Thesis for Investing was:

P/E band has been 12 to 20 in past 5 years, and is trading close to 12 now.

Scope for some P/E expansion as compared to HDFC.

Though EPS CAGR may be single digits or lower double digits going forward (this is very conservative estimate), Price CAGR could be much higher than this.

One of the trusted brands in financing.

GNPA of 1.0 and Net NPA of 0.4 looks very good.

Fully dependent on Salaried Class so asset quality may remain more stable than others.

Government boost to affordable housing may help it grow better in next 2-3 years.

You can read my earlier post on this.

Probably, this is a not for investors looking for high growth stories (>20% EPS Growth). But at many times, Low growth stories come up with surprises, and it is better to be conservative in future estimates than assuming that, all others will grow above 20% for 4-5 years .

Disclosure: Invested.

Why is this priced lower than pnb hf? Is it because of lower growth rate?

PNB housing finance is gaining the overall market share since last few years (but base is low comparatively), while LIC housing finance is loosing market share marginally (to SBI and PNB)… This can be one reason that LIC Housing finance is priced lower…

From Q3 fy19 concall:

Vinay Sah: We would like to take it much higher but home loan as it is the growth rates that we are experiencing from the two, three big metros is very muted and for some of the quarters like Q4 quarter usually this Rs. 9,000 crores goes up substantially. Substantially I mean say maybe Rs.

12,000 crores or something. So this Q4 we should be able to do Rs. 11,000 crores, Rs. 12,000 crores.

3.Kunal Shah: Okay and between bonds and banks how are the rates today incremental borrowing cost?

Vinay Sah: See we are still receiving money from the banks at PLR plus MCLR plus 0 spread. So that continues and average if you look at it the banks MCLR will be in the ballpark of around 8.4 to 8.5, in terms of bond markets NCDs at the shorter end about ten days back we had done a short term issuance at around 8.5% coupon.

That was about a two-year paper, we have done a ten-year paper after that around 8.75 or 8.8 so

I would believe that the yield curve will remain within that range. That is as far as the NCDs are

concerned. Shorter end the cost of fund has come down significantly in the early parts of January we had done some commercial papers for about two-and-a-half, three months which we had raised at less than 7% or 6.85%

Disc: Invested recently

Our strategist recently increased the weightage of LICHF in our model portfolio. In our view, after a span of two years, the business environment is turning favorable for LICHF. **With liquidity tightening, we expect players with stronger parentage to disproportionately benefit because of (a) larger access to capital and (b) lesser competition from lower-rated peers**. Hence, LICHF sailed through the past quarter with ease, raising INR200b from NCDs, INR90b from CPs and INR10b from deposits.

^^From Motilal Oswal newsletter which I received in my inbox today

1. Agree with the bolded part, but LICHF has been increasing the weight of builder loans (from 5% to projected 9% iirc as per the previous concalls) where the NPAs are higher and asset quality needs to be watched.

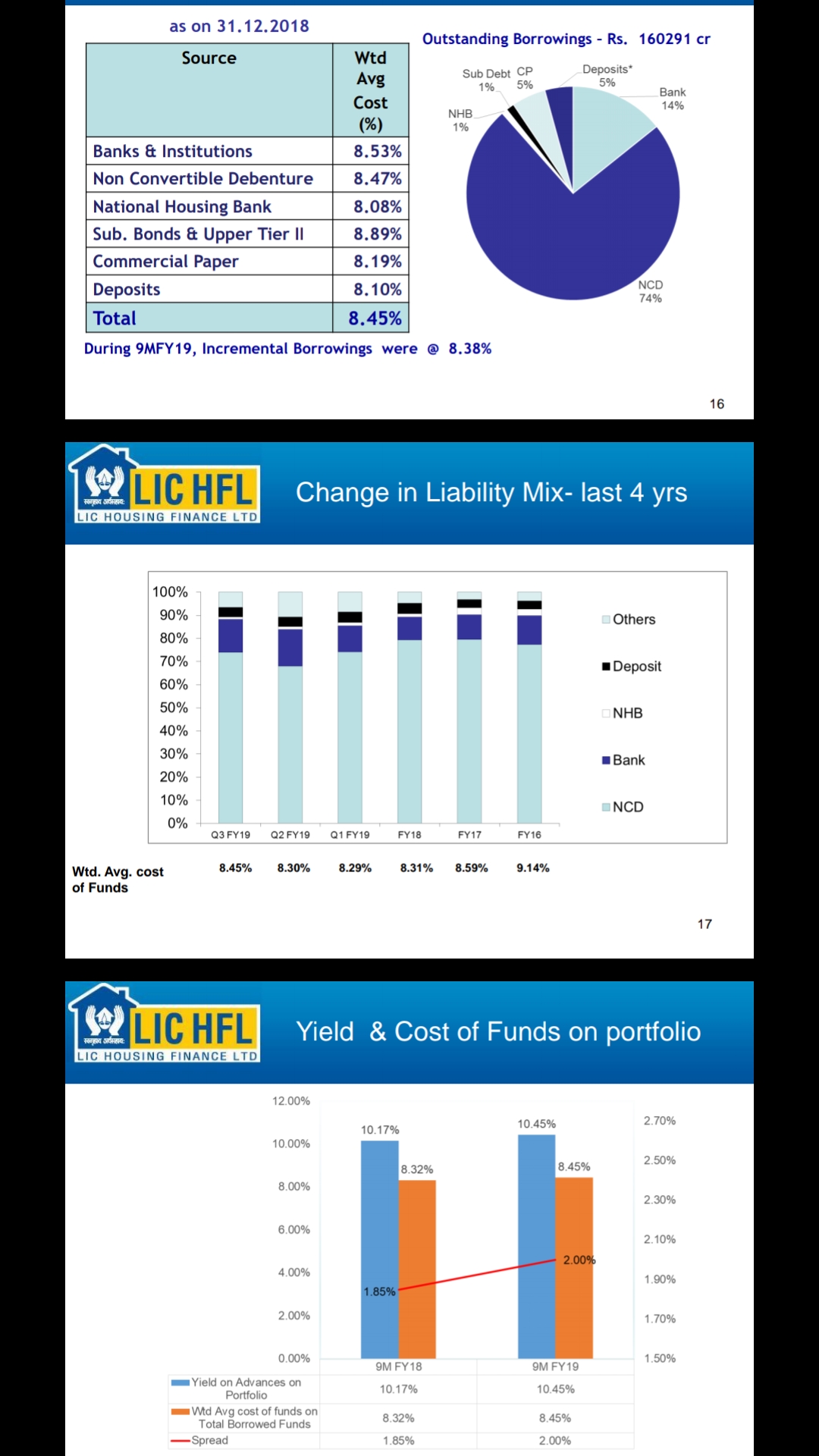

2. From past 15 years, RoE has been between 17-25% every year (no equity dilution in 15 years) and dividend payout of 17-20% of the profits. For fy19 , I would say the expected average roe could be 16.5% (networth increased as balance sheet was modified as per Ind-AS).Following is a snapshot from Q3 FY19 presentation from lic housing finance

Cost of funds of entire liabilities (1.6 lac crore) at 8.45%, is lower than the figures of FY16, FY17.

Incrementally (for borrowing in 9m fy19) , the cost of funds is 8.38%. No ALM mismatch. the company increased lending rate 60 bps in 9m Fy19 and again by 10 bps in January 2019. The margins are intact (infact improving).

Disbursements absolutely normal a. Builder loans just at 6 pc of book i.e. arnd 11 k cr. which is divided in 256 project accounts. b. LAP book quite granular with average LAP loan only at 12 lacs (iirc from concalls). So Asset quality expected to be stable (or improve as gnpa is already over 1 pc due to delayed payments, no structural issue as per the management).

PEG ratio of 0.7 suggests undervaluation and so does the historic price to book value.

Disclosure: Invested.

LIC-Housing-Finance_20032019.pdf (112.1 KB)

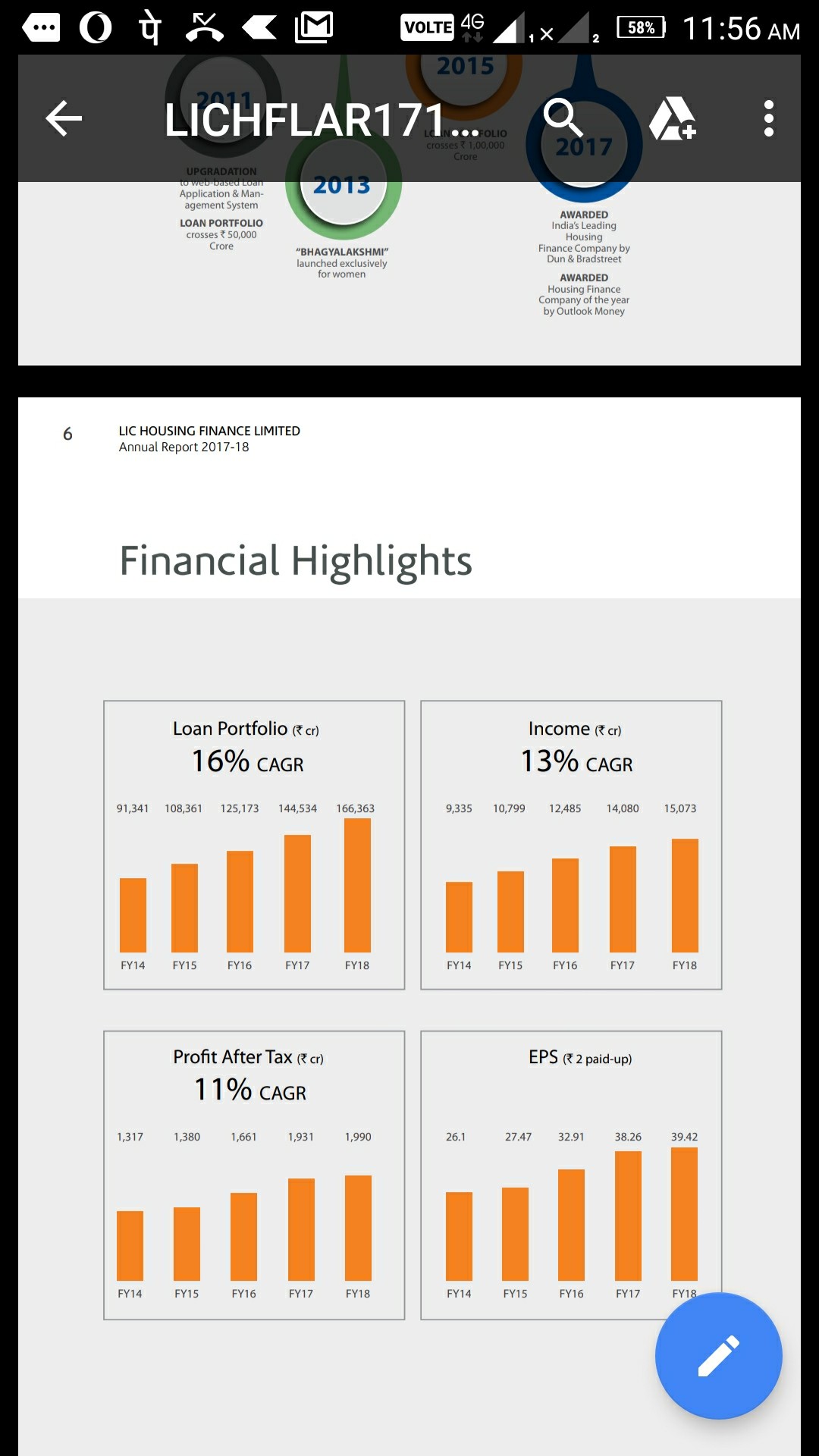

A picture from FY17-18 annual report

5 year growth rate has been 16% and expected to be stable going forward. Profitability/income growth rates have been lower till fy18 but have been increasing (as margins bottomed out some time in fy18):

YoY PBT comparison for last 3 quarters is as follows:

Q3 FY 19(860 cr. ) Vs Q3 FY 18 (718 cr)

Q2 FY 19 (745 cr.) Vs Q2 FY 18 (640 cr)

Q1 FY 19 (788 cr.) Vs Q1 FY 18( 655 cr)

Taking stable and fairly predictable growth rates of 16% , PEG ratio currently stands at somewhere close to 0.7 which imho provides very good margin of safety if one were to Invest in the co.

Disclosure: Invested.

Where can I check at how much yield LIC Housing has raised money from the market?

Good result declared

LIC Housing Finance Q2 Result Update!

https://drive.google.com/open?id=1A2Y2MWWMFUKXvn35b7RINUM4VosOD1nO

Prepared by E-Global Group of Companies!

https://www.e-global.in/about-us/#Endeavour_Wealth_Management

(Disclaimer: Not an Investment/Trading Recommendation)

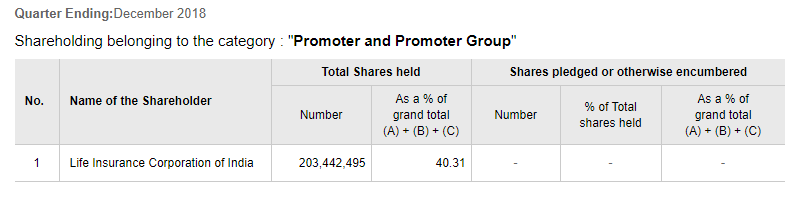

Market is talking about the value getting unlocked in IDBI by LIC in the event of an IPO. What about the LIC Housing, where the promoters holding is at 40.31% ?

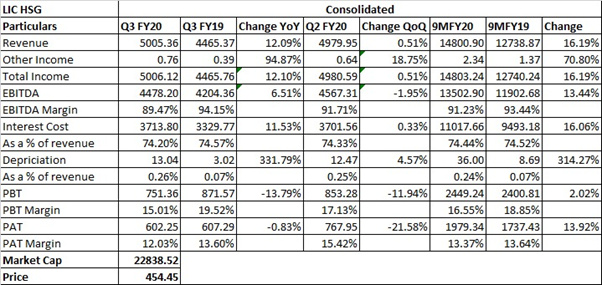

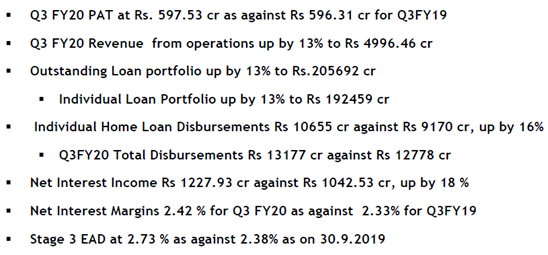

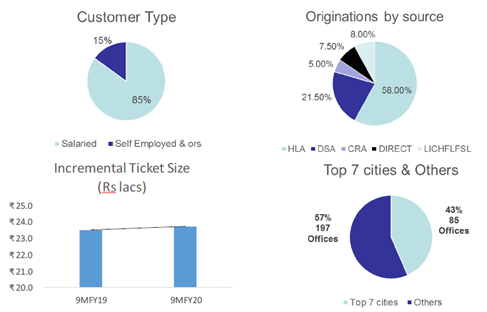

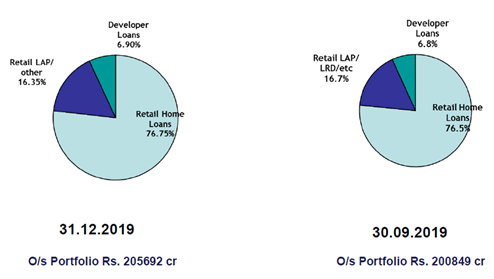

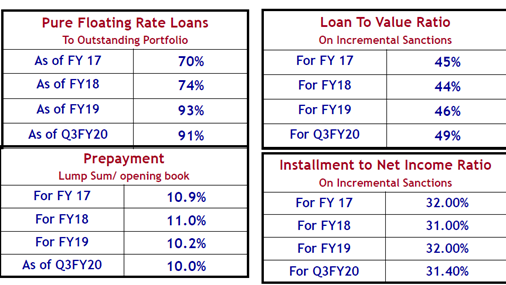

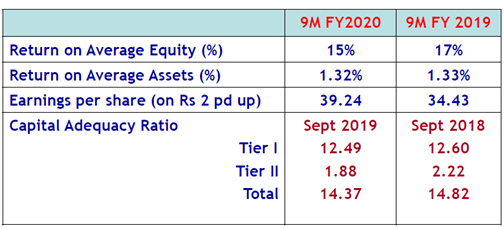

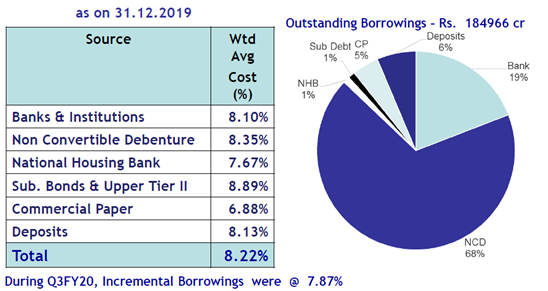

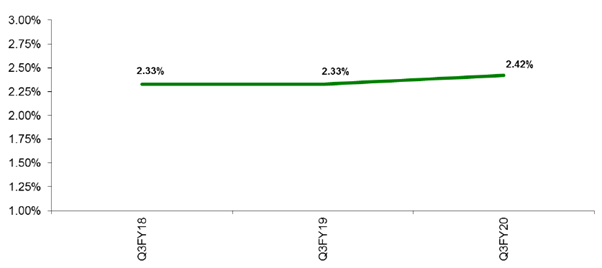

LIC Housing Q3 Results!

Q3 FY20 IP:

Q3 FY20 CC:

Disclaimer: Tracking

As per my understanding they seem to be suggesting that IDBI which has been under PCA Framework since 2017; LIC will work with RBI to get it out of PCA, so it can again start lending money and hence seem valuable to investors. LIC will then dilute its stake to retaliers and thats how they plan to unlock their investments in IDBI.

LIC HF has no such issues, they seem to be down due to poor housing environment and also recent resignations of top brass suggest one can go slow in loading this script even though it appears attractive at this price. with PB at 1.2

LIC merging IDBI Bank with LICHF has not been welcome by the markets… PSU banks with their past dubious track record of poor lending does not augur well for lichf seems the chorus view…

but could it be long term positive for lichf as it may help bring down its cost of capital though access to IDBI Banks high CASA. But RBI surely will put limits, already there are high level timelines that LICHF should bring down its shareholding by 2030 …

Also if its a share swap deal, is the market buying idbi bank instead of lich?