Hi All,

This is my first post in valuepickr as well as a stock compelling analysis. I tried my level best for composing this analysis. Consider this as a novice guy analysis and please let me know about my mistakes.

About Company:

Lawreshwar polymers is a 20 year old company , which is a managed by Rajasthani based promoters ramesh chand agarwal and his family. The Company is engaged in manufacturing of light-weight hawai chappals, canvas shoes, polyvinyl chloride (PVC) shoes, synthetic leather chappals and fancy chappals. The Company offers its products under the **LEHAR **brand.

Reasons for selection:

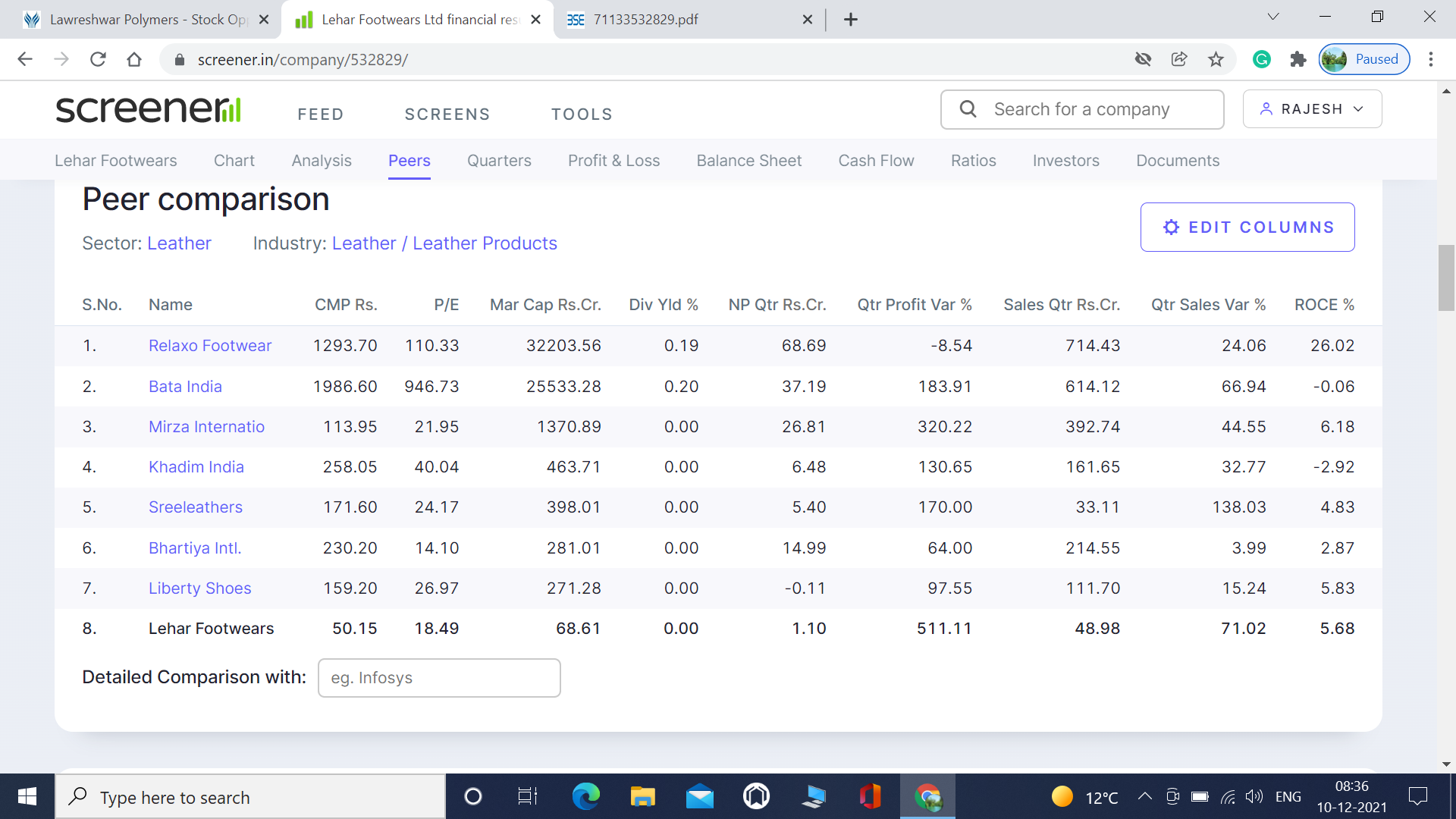

The reason behind selecting this stock is because of the segment which is operating i.e Footwear. I felt i understand their business model. The company is consistently reporting good numbers in terms of both sales and EPS from the last 3 years. Promoters pedigree is also good, they are continuously increasing their stake even in the current September they increased their stake by purchasing from open market at 14.30rs. Currently the share price is quoting at 15 rupees and commanding a PE of 11. Considering the returns provided by other listed peers such as Relaxo,Bata,Superhouse over the last three years, which is more than 500%, i feel there is clear scope for further growth in this segment for Lawreshwar Polymers.

Financials (Crores):

2012 2013 2014

Sales 52.8 68.46 77.05

EBIDT 4.45 5.41 6.47

Interest 1.46 2.16 2.50

Profit 1.22 1.37 1.78

EPS 0.89 1 1.30

Positives:

1). Promoters increased their stake from 58% to 64% in the last financial year i.e March 2014. There is no pledging. Total 1.3cr shares exist with a face value of 10rs. One more promoter ram chand agarwal is doing open market purchase very regularly.

2). They bought a land and factory by paying 11 crores last year and is part of capacity expansion and it will be commenced this year. This should reflect from 2014 Q3 onwards. They specified it as to meet the growing demand and which is good for future growth.

3). Stcok is trading at .67 times of book value.

4). Their brand LEHAR is a known one across india.

5). All the listed players are quoting at good premiums though not directly comparable to Lawreshwar Polymers currently.

Negatives:

1). The interest component is much higher 2.5cr, which is more than their profit. Considering the expansion plans seniors please comment.

2). Very small player compared to its peers

3). No dividend history

4). There is a fire accident happened in the year 2008.

*Consider this as a biased report as i am holding very few shares for tracking purpose.