Cannot disagree more on this point of view. In fact reverse of this is what I believe is true- without revenue growth any profit growth has little meaning. This is because unless your topline is growing the profit/margin would certainly hit a ceiling after some time. Anyway, market and its participants have their own wisdom. We have heard similar comments on many other boards like Affle (I am not comparing business of Affle with Laurus ) where the right moves of the company were seen from the coloured lens. Let us see how this unfolds.

8 Likes

Profit will increase disproportionately due to operating leverage if revenue increases. 25% of their gross blocks did not contribute to any revenue as of Q3FY22. So due to operating de-leverage profits declined faster than revenue. Now if the revenue increases profit will even increase faster like FY21. That’s why the emphasis is on Revenue.

Anyway everybody has their own opinion.

6 Likes

Please refer above posting from nirvana_laha. He has summarized the business/revenue trend and the nos. quite nicely.

Few thoughts here

Worry many people had was

1)will Arv… Api/Fdf sales ever come back

2) will the sales get back to Q4 2021 runrate of 1400 cr

3) Will he ever reach the goal of 1 billion sales by fy23

Think this result will make even the most pessimistic person rethink , as all engines have fired but the most lucrative engine of Cdmo grew by 105%( not many companies) & Bio by 289% is really commendable, as said earlier by Mr Souresh once sales are growing operational leverage will kick in, also even 30% average Ebitda is a very good no, but this no will grow,

now to jump from 1400 to 1800+ quarterly runrate doesn’t seem that difficult , this result has removed lots of fear cause can’t think of many companies with Ebitda of minimum 30% and growth around 50% even if they achieve 30%+ will be happy.

synthesis, bio, Fdf are superbly increasing their share thus less dependence on Arv with every passing year, This result has surely increased my confidence atleast.

Cause even if you see , even in Q4 mutual funds have increased their stake, fiis despite heavy selling in Indian markets have kept stable their holdings in Laurus only public has reduced their holdings, and Laurus has also got awards in most categories in 2021 by top notch organisations this does say something.

Let’s hope for the best invested hense biased will keep tracking fundamentals…no reco take care stay safe.

15 Likes

Q4 Concall notes:

- Industry faced turbulence in RM & solvents. Disruption in logistics has increased. Expanding critical supplier base.

- Maintained profitability despite are headwinds. Invested significantly in capacity creation.

- CAR-T tech investments.

- Dolutegravir use is increasing in paediatric & 2nd line of treatement.

- Filing pace to pick up during current financial year.

- 31 ANDAs filed. 11 in Canada. 5 launched.

- Europe: 2 pdts validated. 8 approved pdts. 3 launched. More to be launched.

- Brownfield expansion proceeding as per expectations. Taking capacity to 10B units. Will be ready before Jun-22.

- Sterile r&d unit to be commercialised in this Q. 4% of sales spent on R&D. 62 pdts in R&D pipeline. 43B branded sales opportunity. 15 para 4 & 10 FTF in USA. Approach remains pdt specific.

- EUA has inspected facilities.

- ARV api biz saw some improvement. 300cr. Once apis reported 70% growth in Q.

- One of largest High potent api capacities in India. Aim to strengthen global leadership & market share.

- Filed 2DMFs. 73 DMFs filed to date. 12 in fy22. Max. Validation of 3 APIs initiated.

- Cdmo is growing fast. 100% QoQ. 75%. Dedicated r&d centre & 3 manufacturing units under laurus synthesis. Sterile, hormone, high potent molecules. Self reliant subsidiary in 2025.

- Laurus bio: 35cr revenue in Q4. 40% growth QoQ. Gradually ramping up of 180KL capacity. Enhancing R2 capacity. Before sep-22. Expanding to offer cmo for recombinant proteins.

- Fy22 sales for arv were significantly lower. All cos had inventory. ARV api & formulation were down 10% around.

- 180KL capacity is fully operational in Q4. Doing debottlenecking now to increase capacity. Significant capacity will come up in Fy24. Recombinant food proteins is major part now. Therapeutic discussions going on internally. The 1M large fermentation capacity is for food protein cmo.

- Fy23: we expect pdt mix percent to remain similar in Fy23.

- 55% of revenue came from arv in fy22.

- Similar margins in Fy23 & beyond.

- Growth will come from non-arv in both.

- Pdt, capacity, market are there. So we are confident to reach the targetare creating separate division for cdmo because of long term contract & opportunities.20Pfizer has mentioned 22B$ of sales for paxlovid. Laurus can’t give any details.

- Next 2 years capex Is 2000-2500 cr capex.

- As non arv increases, gm will also increase

- Have grown 50% in the past, will do so in Fy23.

- Europe formulations will be launched in q3.

43 Likes

A quick look for anyone looking for the latest interview of Dr Chava in Bloomberg Quint.

9 Likes

Some additional qualitative Infrences that stands out from Above interview as well as past media interactions of Dr Chava, as to how he thinks about business and growth

-

Aggressive investment and capacities, quality control ( incl audits) and supply security, deliver at scale that customers need, and achieve economies of scale that not many competitors exist in that band thus cost leadership

-

FY 22 capacities utilization- API near full, formulations at full, Synthesis and Bio demand outstrips supply, on top of this he goes on to say had they have supplies in place could have done more biz with same set of customers - demand is not an issue( ex ARV)

-

His confidence on guidance - how much of it eminate from demand visibility? - where is it headed directionally? - man has delivered in past when demand was tilted towards Tender heavy biz( ARV api), ARV biz is already near 50%, going towards 35-40 by next year and reduced ahead - now think for a minute as to does guidance quality and biz control gets better with every passing year?

-

One question we all should be also asking is - next key growth driver( Synthesis) and leadership driving it - Synthesis is headed by his son as EVP , likely he has good support but if anything the delivery has been better than expectations in this division - fast forward 2025 - Dr Chava expect it to be higher than guided 25% of total pie - can it be 30% of 10K cr revenue n 2025? I.e. 3000 cr +, high margins of 35%-40%( peers range), 1100-1200 cr EBDITA - can this biz on standalone command 25K cr+ mkt cap - in realm of possibilities - rather than worrying too much about ARV QoQ, our energy is better spent analyzing this part of biz, how do we track it? Capacity addition and utilization is a good starting point.

-

Does he cut it too close more often? - $1B rev FY 23 has sizable hevaylifting by FDF in Q3, Q4 - with critical path dependency on some pending Approvals in Q2 and 5B capacity ready by June 22. Now this has almost no buffer , Dr Chava drives and shares accordingly- how we simulate is up to us, but full marks on execution aggression part. Some miss here and there is okay rather than being conservative and loose business

-

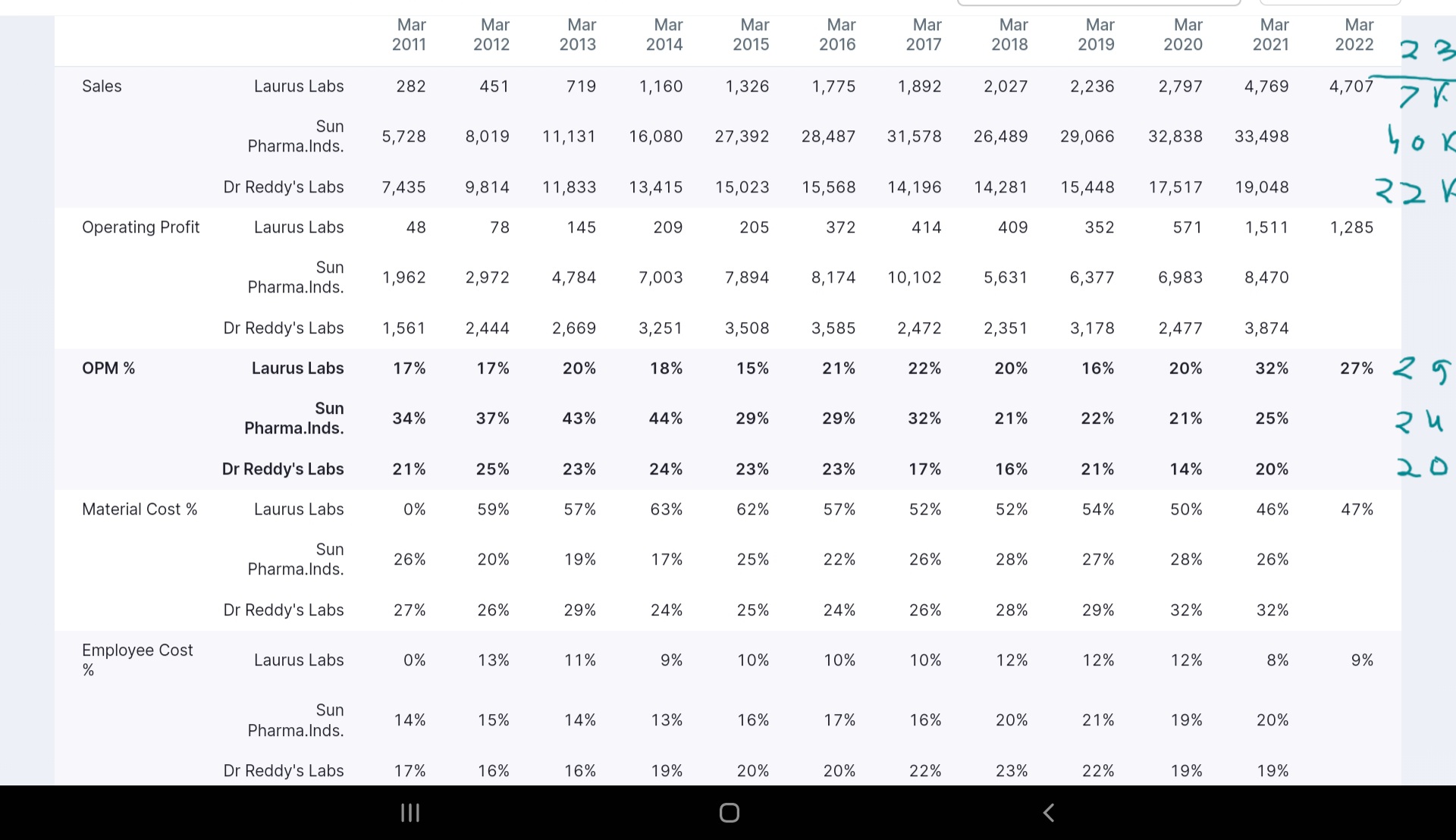

Can Laurus go on to be among top 3 pharma player from India? Dr Chava is Ex Dr Reddy employee and the organization he is building has resemblance as well, Sun is largest at 6X sales at 225K cr and Dr reddy at 4X sales at 71K cr, Laurus at 30K cr is 6X TTM, look at growth and margins trajectory especially after 2016( pain times for pharma Generics players) - excluded pure play CDMO like Divis.

If we extrapolate 1 year forward, P/S for laurus is 4.5 for much higher growth and margins, it’s a different issue as to how Laurus growth trajectory will be once it crosses $1B runrate. It’s well known that most Generics player struggled for growth in last few years, how and What Laurus do differently is something worth pondering about.( Synthesis and Bio are part of answer we seek).

Point being to be near 100000 cr mkt cap organization in next 5+ years, what Laurus needs is

- A Generics engine ( formulations +api) with 10000 cr+ revenue like Dr reddy model

- Synthesis/ CDMO engine with 4000 cr+ revenue running like Divis model ( may need spin off to avoid conflict scenarios)

- Others niche - Bio running at 1500 cr-2000 cr revenue

- In organic growth if need be - capabilities and/or assets

Above is an illustration and mix/numbers may alter per Journey, point is possibilities over med term.

Journey will not be linear, but Laurus under Dr Chava is building all foundational blocks in right direction, all we have to do is track core thesis and mgmt walk the talk, give time and some faith/rope on minor misses.

Invested

41 Likes

Laurus did Rs14 of EPS. It is trading at 42x P/E FY22. Even if it doubles profits in FY23 it will trade at 21x FY23.

It will not double profits as:

- Even if its achieves guidance of Rs75bn sales growth will be 52%,

- Profit growth will be 52% if it achieves its guidance of flat margins.

If profit growth is 60% then FY23 EPS will be 1.6 x 15.42 = Rs23.4 which implies stock trades at 25x FY24 EPS if company achieves guidance.

So it looks fairly valued to me. It all good to talk about all the qualitative positives but it’s pertinent one works out the numbers also.

And yes please don’t compare valuations to Divis. It is unlikely to trade anywhere close to that name.

Last but not the least Dr. Chava’s capex just does not seem to end. No FCF for last 10 years. Where is all this money going?

Given Rs20 to 25bn of capex over next 2 years, there will be no FCF for next 2 years.

Is Laurus really a pharma company?

11 Likes

Hi @vnktshb

I’m going to assume you are just playing devil’s advocate here since you were very bullish on Laurus up until last year too( your disclosures stopped saying that you are invested anymore but i won’t jump the gun and assume you aren’t). I’m just going to attempt to give short answers to your questions

-

Would you rather the company die a slow death in arv api and generate free cash flows or would your rather they increase capacity in cdmo/synthesis and bio and move towards higher margin growth engines? They have had to spend cash in these new areas and even now demand is exceeding their supply so they will continue spending it while de risking from the terminal business of arvs. I’d rather they spend all the cash generated in the business into these growth and de risking engines. They will have to continue spending over the next few years(it’s not like they are drowning in debt or poor return ratios). that’s just the nature of this business where multiple growth engines and economies of scale matter… so if one isnt comfortable then one needs to look elsewhere. If one were to want free cash flows and sub par growth for safety reasons then yes… looking elsewhere at bluechips who’ve already reached their end game is where one should invest. Laurus is a work in progress thats about half a decade away from reaching that position.

-

They are targetting 30% Ebitda margins this year which would lead to a near 70 percent increase in profit. That would mean it’s valued around 20 to 25 times forward eps for FY23. … while not Benjamin graham cheap… that’s still fairly priced if they pull off what they say they will(macro factors are obviously a huge risk here). Bear in mind with each passing year they’ll grow cdmo/bio even bigger with lesser and lesser reliance on arv… i dont like predicting the vagaries of the markets but i would definitely pay higher than 25 x eps for the company if they do pull of the above and are available at the same price this time next year and would double down if available at under 20 PE. So bringing valuations into this conversation is a bit speculative since that’s out of our hands… all we can do is track the business and ensure the business is getting more antifragile.

-

The Laurus of today cannot be valued like divis. However, as gross margins improve with cdmo and bio contributing more by FY25 i don’t see why they can’t be valued at divis level considering the expected growth rate (though i must admit the operating margins of divis ie 40+ maybe a step too far for Laurus as a whole and may be something for a cdmo spin-off) The company is a work in progress… and as investors here I’m sure most of us know this. It’s about what the company will be in a few years that’s interesting… and the opportunity it presents us to get onboard for the ride at an early stage. You are right regards the present though… today on April 29th it’s a bit overvalued at around 40 PE. I personally dont really care about today since it’s still fairly valued considering the possibilities by April 29th next year and the year after. This is the leap of faith us retail investors have to take(that being said i do have a big margin of safety so maybe someone investing fresh capital today may be a bit more worried)

-

Yes it is a pharma company

. I’m assuming you mean regards the valuation? For a generic api company it’s overvalued… thats for sure. Whether it is a generic api company is upto an individual to take a call depending on their timeline of investment.

. I’m assuming you mean regards the valuation? For a generic api company it’s overvalued… thats for sure. Whether it is a generic api company is upto an individual to take a call depending on their timeline of investment.

Again, i don’t mean any harm in posting this. I appreciate a bear thesis since it removes our rosy eyed spectacles on this forum. However, i don’t see any of the above as red flags currently. Cheers

Disc: Invested since much lower levels. Not a sebi advisor. Please feel free to flag this post if it’s not adding to the discussion. We have a lot of positive posts talking about what i wrote on here already so I’d understand if this post gets flagged and deleted.

42 Likes

In few days, A barrage of analyst reports will come out with decimal point EPS precision and all the number crunching for many years to come - why bother if that is what one is focused at ![]() . Some of us so like to look at thesis beyond immediate numbers.

. Some of us so like to look at thesis beyond immediate numbers.

Good to hear an opinion!

While it’s early, point is Synthesis division has potential to get there in few years, If they contnue to deliver.

Unless you have insights that can enlighten us as to why it will never happen.

Not sure what’s wrong will investments giving growth with 25%+ RoCE, funded without dilutions or stressing balance sheet.

Some of us do believe so ![]()

12 Likes

Laurus EPS for FY22 is 15.4 Rs, not 14 Rs. Please refer consolidated numbers.

If Capex is not done then people like you say that Laurus is only an ARV company, no terminal value, overvalued. If capex is done to diversify the business people like you say that Laurus is a cash burning/fraud company, where is the FCF?

Some people can never be pleased.

7 Likes

My take is…Many people respect nos a lot , understandably but what i Marvel at is the business Accumen… From a company majorly dependent on Arv, once sensing it’s somewhat bleak future in a comparatively short period they successfully diversified into Cdmo which takes real hard work and passion, then Bio which everyone agrees is the future, other APIs and FDf and immuno act which is a complementary to Bio

Infact i feel they should not give dividents and should not buyback as they are making better use of capital than i can do, Dr Chava in my opinion is a fantastic capital allocator till now.

Their OCF has also increased commendably means they are actually getting real cash which is a very good indicator in my view.

Also the hard work they had done on Cdmo,APIs,FDf for the last two years the benefits will be hugely visible from FY23 onwards and as by fy 24 onwards I feel the hard work they are putting now in Bio since acquisition of Richcore It will be the star cash spinner trying to compete with CDMO, that’s his strategy you like it or not Being proactive, sensing opportunity, building massive capacities and making the best of opportunities arising… Fortune does favour the bold😉

Also we are missing one point what makes us think the upcoming acquisitions will not be as good or better than the one he has done so far even he is improving with every acquisition, all want growth very difficult without intelligent capex for future earnings. That’s what investing is from where and how will growth come, and with 30% Ebitda net profit is not difficult to assume.

Also as well put by Mr Dev his son is leading the Synthesis division as EVP and it’s doing so well infact better than expectations…now even succession fears by a few boarders are put to rest i assume

valuations wise there are many companies trading at exorbitant valuations how they are so superior and better diversified than Laurus still not able to get my head around that, my personal thoughts looking at its future Laurus is undervalued.

As far as competition is concerned the only competition to Laurus i feel is Laurus itself trying every time to surprise and beat its own record.

Invested hence biased No reco DYOR

9 Likes

The future does look good. Growth in CDMO and Bio is the most impressive thing that happened this FY. My question is, doesn’t the valuations look like it has already factored in the future prospects of CDMO and Bio? I mean if you look at the current valuations, it is pretty high for a generic API company. The API and FDF still accounts for 80% of the revenues. And I think the market has also already factored in the 1B$ revenue target for Laurus. So I don’t expect that Laurus will “surprise” the market with it’s future growth. On the other hand, if for some reason the growth gets sluggish, the stock will be hit badly as there is no margin of safety as far as valuation goes.

I personally have been a fan of Dr. Chava and I’m sure the future of Laurus is bright. But valuations is the concern for me. These are my personal views and I may be wrong.

4 Likes

Rishav will try to answer this i think… How many companies do we know who can have Ebitda of around 30% + and let’s catch growth of 30%

Though their guidance is of 50%. And for coming years henceforth 20 to 25% conservatively i feel.

There are very very few companies who can stick their neck out and talk of such massive growth specially in such adverse geo political and inflationary circumstances, after this result atleast i feel many fund houses and big institutions might look at laurus with a totally different lense not labelling it as a net arv api company and may surely want a slice of its diverse growth story (there aren’t many such stories in the market) and might bet on its growth story, believing in it.

So many internet and other companies trading at hefty PE presently are all talking about future earnings in a few years which are presently not there… So why can’t Companies like Laurus…

and even dream of being a global giant one day from India it has all traits in it … Of course there will be many hurdles but till now they have decently navigated with governance and complaince, this gives us some assurance they might tide well over all complaince issues, fingers crossed. Minor hiccups can’t be ruled out, only if there are structural changes we have to change our mind.

As far as valuation is concerned at 37.9 PE don’t think its expensive there is room for PE expansion looking at future, plus good growth will lead to operational leverage thus margin expansion, all go hand in hand but real money will be made by patient investor down the line incase there is a demerger roughly 3 to 4 years… Can be wrong in my thesis invested hense over optimistic DYOR take care

7 Likes

After posting stupendous growth in 2021 yoy, co had a flat 2022. now targeting 50% in 2023 yoy.

Naturally the next Q is what about 2024? There doesnt seem to be much visibility on this. Atleast for now.

How can one decide what valuation multiples to assign for such chequered growth?

Discl. invested from earlier. holding on. for now.

1 Like

The only difference in commentry from management is before it was aspirational and now they have removed the word aspirational and replaced it with most likely.

How they will achive it to understand in detail you will have to go through previous concalls and his interviews with Niraj Shah on YouTube

But roughly why i feel they might hit the Bulls eye is …Dr Chava has said once in few years they do grow more than 50% and they have done this before also, of course not possible for every year

And they might do this again in future

After fy23 they have not given any guidance when asked , rightly he said once we reach q423 we will be in a position, this says he only speaks when he sees visibility not just bluff in air that’s my understanding , but i feel after fy23 as these engines of Cdmo, bio grow bigger , the rate at which they are getting new giant customers they might get 20 to 25 percent growth, after every passing quarter even their reputation in efficient delivery,complaince, reliability and goodwill are compounding,

As far as lumpiness in sales is concerned i feel what happened in fy 22 was a blessing in disguise Arv sales plummeted and they were forced to look out and maintain sales so they quite successfully diversified into sunrise sectors…viz Cdmo,Bio,other api,FDf, immuno( though relatively new but has the potential of huge growth ) , as these sectors have long, diverse visibility and less chances of plateauing down anytime soon, this should assure us investors that even in future if some obstacles like these come again which aren’t visible now, we can take comfort from this action and can rely on the management (getting new talent with every acquisition) to navigate us through rough patches, which do come once in a while.

He had said around fy25 no one will talk about arv and it’s regime think after Q4 fy22 only the concerns have drastically reduced

Other risks do remain as with all Pharma companies, the only way to judge is what they have done in past and so far it’s satisfactory, what i see with a hawks eye as an investor is above all corporate governance and so far am satisfied with their Corporate governance, transparency and teamwork, few flips, blips and misses will be part of most companies we will have to see the bigger picture , invested hense biased no reco take care

7 Likes

I think CDMO business have saved the Gross margins of this quarter with ARV forming new lower bases. Bio segment is still in nascent stage and require at least 2- 3 years to come on full scale.With drop in Margins of ARV, there will be great responsibility on CDMO segment to deliver the aspirational target of 1 billion revenue. Watching closely & will wait for lower price to add further.

1 Like

8 Likes

I’m just wondering at what stage does Laurus consider demerging Laurus Synthesis? It has touched 900 cr annual revenues in FY22 and I’m sure that number will double in next 2/3 years. The capex will also be completed by FY24.

Bundling CDMO in the main co is hampering value discovery for the standalone business, which could potentially be worth a billion dollars on its own.

7 Likes