Any views on this?

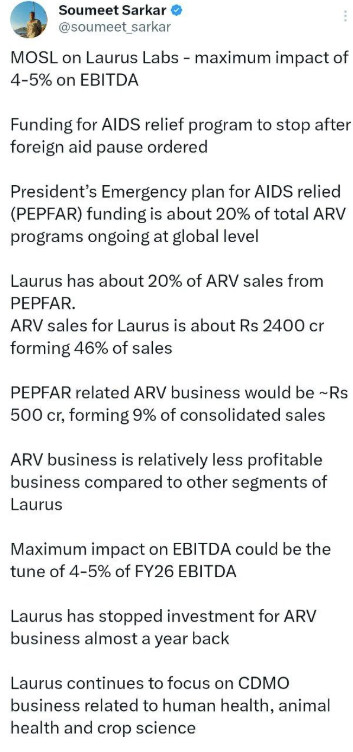

Virtually no impact for Q4 FY 2025 and Q1 to Q3 FY 2026 . Any impact even if there is any would come only in Calendar Year 2026 ie Q4 FY 2026 onwards .

Also clarified that drug cost only constitutes 10% of the PEPFAR funding for HIV . Even after 90 days review , Dr. Satya does not believe the funding to completely stop for the drug cost component .

Results will speak for themselves. In a SIP mode Disc : Highest position and biased

Love the randomness in the market ![]()

12 Likes

LAURUS LABS | CLARIFICATION

Co. Days The ARV medicine market is ~US$ 1.5bn, representing 10% of the annual HIV budget, funded by governments, PEPFAR, and the Global Fund. Global efforts have effectively controlled AIDS. Despite potential funding challenges, the Company believes medication procurement won’t be impacted.

The U.S. rejoining WHO further supports this outlook.

No significant business impact is expected.

Guidance: Retain FY 2025 Outlook, Revenue Growth & EBITDA Margin See An Improvement

4 Likes

Laurus Labs Q3FY25 Earnings

Financial Performance

Quarterly Performance (Q3FY25)

- Revenue stood at ₹1415 Cr, reflecting an 18% YoY growth.

- Growth was led by the CDMO business (+88.7% YoY), supported by the formulations division.

- Weak ARV API demand offset some of the gains.

- Gross margin improved to 56.9%.

- EBITDA increased to ₹285 Cr, with a margin of 20.1%.

- Margins remain under pressure due to operational deleverage, though asset ramp-up is expected to improve margins in Q4.

- PAT stood at ₹92 Cr.

- ROCE at 6.8%, affected by lower operating results and ongoing capex investments.

- Net debt at ₹2766 Cr, with a debt-to-EBITDA ratio of 3.1x vs 3.4x last quarter.

9M FY25 Performance

- Revenue: ₹3834 Cr (6% YoY growth).

- Gross margin: 55.8%, driven by process improvements and a better product mix.

- EBITDA: ₹638 Cr; EBITDA margin expanded to 16.6% vs 15% last year.

- PAT: ₹125 Cr.

Segment-Wise Performance

CDMO Business

- Highest sales in the last 8 quarters at ₹400 Cr.

- 9M FY25 growth of 33%, driven by asset ramp-up.

- Shift towards high-value, complex small molecules.

- Over 90 active projects, mostly in human health, with some in animal health and crop protection.

- Encouraging RFPs and multiple signings of early- to mid-stage projects.

- Supplied one commercial launch quantity and multiple registration quantities in Q3.

- Q4FY25 to witness late-stage project deliveries, reinforcing the company’s 2025 growth outlook.

Generic API

- Revenue: ₹531 Cr (-7.5% YoY).

- ARV APIs declined 10.5%, while Oncology APIs saw a sharp 50.7% drop, offsetting a 27.2% growth in Other APIs.

- 9M FY25 API revenue declined by ~3%.

- The ARV API business faces softer demand due to capital reallocation towards higher-margin businesses.

- Filed 4 DMFs in 9M FY25, with 3 in the non-ARV category, bringing total filings to 87.

- Expect flattish performance in the near term, with a focus on non-ARV opportunities.

Formulations Division

- Revenue: ₹436 Cr

- ARV formulations and developed markets business showed an uptick in activity.

- Expecting meaningful growth in FY26 with a couple of ANDA launches.

Laurus Bio

- Revenue: ₹48 Cr (+14% YoY).

- Exited low-margin, non-core nutrition businesses.

- Flat growth expected in FY26 until additional capacity comes online in FY27.

Business Outlook and Growth Strategies

- API and Formulation revenues are expected to remain steady at ₹650 Cr per quarter in the short term but should pick up in the medium term.

- Expansion of CDMO/CMO offerings in small-molecule APIs.

- ARV business is expected to remain in the range of ₹2300-2500 Cr.

- Shift towards high-value, complex APIs leveraging Bio-Catalysis, High Potent Manufacturing, Hydrogenation, and High Energy Chemistry.

- Human Health and Animal Health CDMO are expected to drive growth YoY.

- PEPFAR tender secured for 3 years, with 2 more years remaining.

R&D and Quality Initiatives

- R&D spend: 5% of sales for 9M FY25.

- 120 quality audits completed in 9M FY25, with successful clearance.

Capex Investments and Strategic Moves

- Q3FY25 capex: ₹186 Cr.

- 9M FY25 capex: ₹448 Cr.

- Strategic investment by Eight Roads in Laurus Bio, aimed at enhancing commercial-scale manufacturing.

- Plans to double fermentation capacity, expected to be operational by CY26-end.

- Focus on microbial precision fermentation and enzymatic engineering.

- Two new generic product approvals are expected in near quarter

Management Insights and Future Guidance

- CDMO growth remains the key focus area, with FY25 already proving to be strong and FY26 expected to be even better.

- Management remains committed to high-value business segments like CDMO, ensuring EBITDA margins move closer to 25%.

- Expansion into Animal Health and Crop Science, with commercial sales expected from FY26.

- Vector manufacturing facility to be commercialized in FY26 (investment of ₹120-130 Cr).

- No plans to diversify into NCE molecules, focusing on small complex molecules.

11 Likes

Company has barely given any return in last 4 years. Once P/Es are stretched, then future returns are capped

Very expensive even now

3 Likes

During this time since Mar 2023, FIIs n DIIs were regular buyers … in the last quarter even promoters bought significantly at price higher than CMP…Only time will tell who knows better

1 Like

We should be careful to look at the quantum of promoter buys. A 20 crore purchase when the promoter has 2000 crore is just to pump the stock at ATH

4 Likes

True…But in my view CDMO segment can have non-linear growth once few molecules commercialise… Then PE and other valuation metrics look completely different…ofcourse being retail have the luxury of waiting for confirmation and buy…

I am an amateur and just sharing from experience of other companies…

Disc: had good run previously and recent one also, but no position currently… hoping to enter if we get dip in this market correction

2 Likes

I hope you aren’t calling this one “expensive” by only looking at P/E. A business with massive Operating Leverage potential - the worst metric one can value such a business on is P/E!

The sheer earnings power that is to come from the CDMO segment will suprise a lot of people, including analysts. One has to just creatively imagine the non-linearity that can come into the Earnings. I say ‘creatively imagine’ because visualizing non-linearity is extremely difficult for the human mind. Your “expensive” P/E metric will crash land post this, assuming stock price remains exactly at today’s price.

Disc: invested since 2020

18 Likes

https://x.com/quest_for_value/status/1894779289385783364?s=46

“Laurus is 20 yr old company. Whatever we invested in first 15 yrs, we have invested the same amount in last 5 yrs

Whatever we invested in last 20 yrs, we will invest the same amount in next 5 yrs

We are ready for short term pain for long term gain.”

- Dr.Chava at Bioasia2025

19 Likes

Market Editor | Market In FY26: Where Are We Headed? | Madhu Kela Exclusive | CNBC TV18

Latest interview at CNBC TV 18.

2 Likes

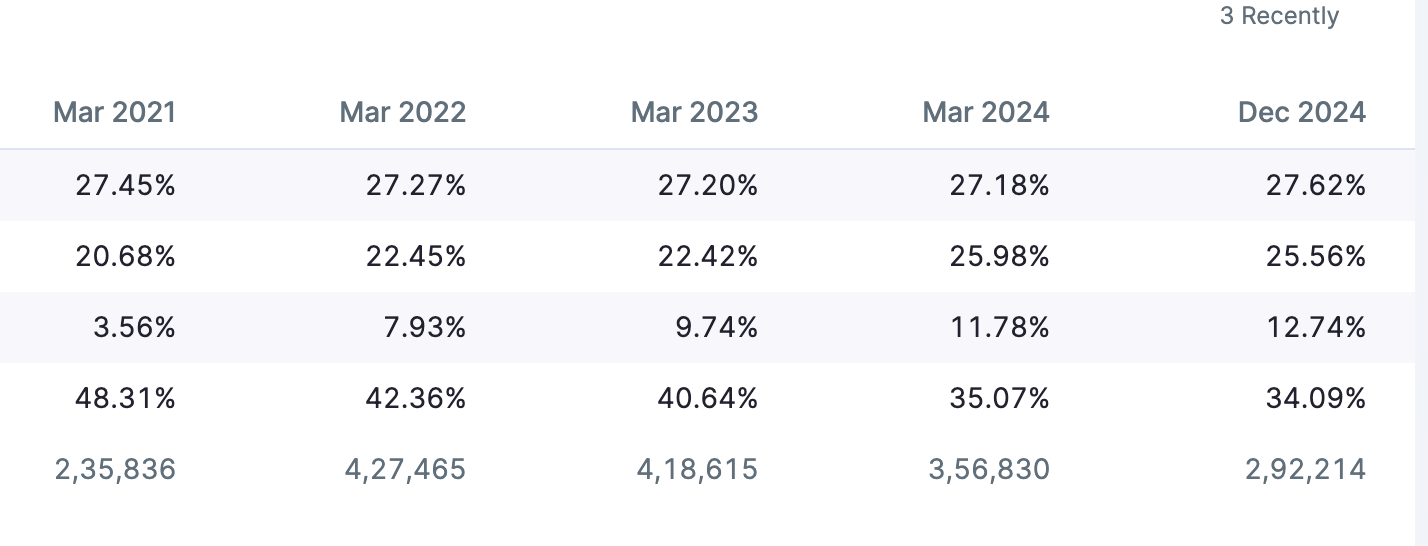

Sharing the shareholding pattern of Laurus

So classical. Institutions are adding, and retailers are selling.

The number of shareholders has reduced by almost 30% from the top.

Just sharing. Invested and Biased.

dr.vikas

11 Likes

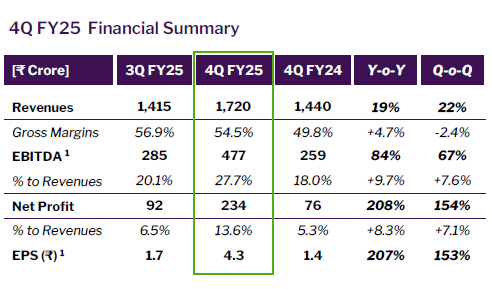

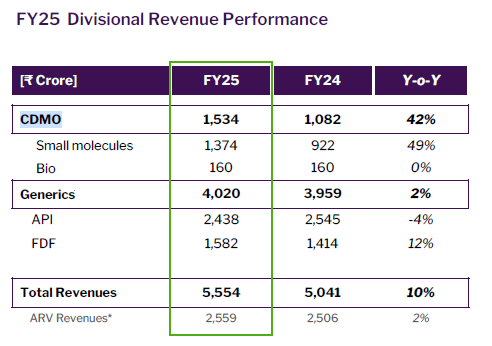

Finally, some great results from the company! The best part of the results is the strong pivot towards the CDMO segment, which seems to be happening at a rapid pace. The CDMO sales have grown an impressive 42% YoY and now contribute nearly 28% of the total revenue.

If this momentum continues, the next two years could be orbit-changing for the company — we might finally see a meaningful uptick in the asset turnover ratio, marking a new phase of growth.

Disclosure: Invested

28 Likes

During the recent earnings call, Dr. Chava shared that ImmunoACT, a Laurus Labs subsidiary, will have the capacity to treat 2,500 patients annually by Sep 2025 for its CAR-T cell therapy. The therapy, branded as NexCAR19, is priced between ₹30 lakh and ₹40 lakh (approximately USD 36,000 to 48,000) per patient. This pricing is nearly one-tenth of the global cost for similar CAR-T treatments, which can go up to ₹4 crore (around USD 500,000). Based on a price assumption of ₹30 lakh per patient, ImmunoACT could generate annual revenue of approximately ₹750 crore.

With 33.86% stake by Laurus Labs in ImmunoACT, this could be around Rs. 253.95 crore revenue for Laurus.

31 Likes

Can you guide me where Dr. Chava talked about the same. As in one interview he said that he is not expecting any meaningful revenue by FY26 or FY27… so bit surprised by this huge bump?

I might be wrong though

2 Likes

19da2c04-00b2-4c45-962b-0bb3c605244b.pdf (442.5 KB)

Very good results with margin improvement and 100% jump in CDMO revenue.

15 Likes