Dr. Satyanarayana Chava: Formulation capacity is very fungible. So, we can use it for ARV, non-ARV, diabetes, cardiovascular. There are no challenges. Only the size of the batch determines which line we use.

This is from latest concall, but I am unable to understand why formulation capacity is very interchangeable ? I am not getting feel of this?

1 Like

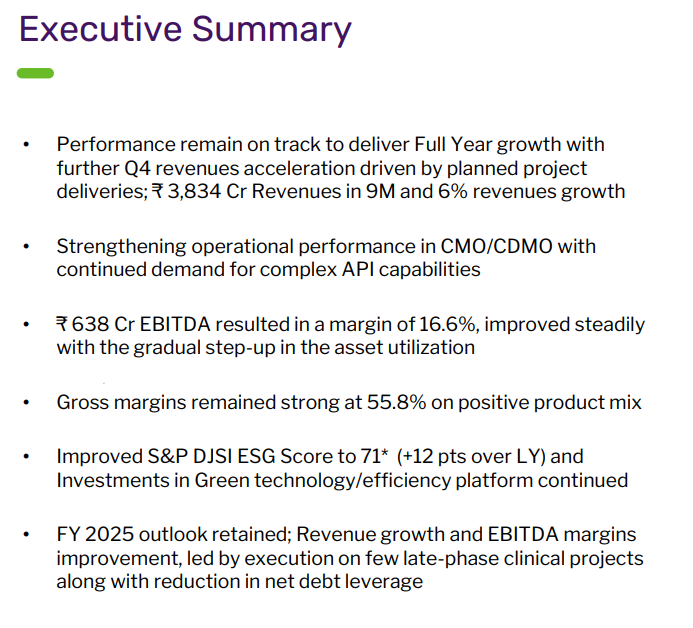

Laurus Labs -

Q1 FY 25 results and concall updates -

Revenues - 1195 vs 1182 cr

Gross margins @ 55.1 vs 50.6 pc - a key indicator of health of the business

EBITDA - 171 vs 168 cr ( margins @ 14.3 vs 14.2 pc )

PAT - 13 vs 25 pc

Revenues led by strong demand in Oncology APIs, ARVs. Delivery schedule in CDMO business in Q1 was tepid

Gross margins @ 55 pc - is a key indicator of business profitability. As the capacity utilisation of company’s assets improves, profitability can potentially show a major improvement

Spends on new initiatives - Cell and Gene therapy + Animal Health were at 15 cr

Segment wise revenues -

CDMO - 214 vs 250 cr, down 14 pc - CDMO deliveries are scheduled for key late phase NCE projects in Q4. Witnessing significant interest from new customers, momentum in RFPs continued from big Pharma and key Biotechs. Total active CDMO projects ( including intermediates @ 70 !!! ). Out of these, 10 projects are in commercial stages. 20 projects are in Animal health + Crop protection spaces. Have started supplying commercial validation batches of the Animal Health, Crop health projects

APIs - 664 vs 597 cr, up 11 pc - led by strong growth in Onco APIs ( up 120 pc YoY ). Segment wise breakup of API sales -

Onco APIs - 18 vs 9 pc YoY

ARV APIs - 60 vs 68 pc YoY

Other APIs - 22 vs 23 pc YoY ( could have grown stronger but the sales were deferred by shipment delays )

FDFs - 274 vs 285 cr, down 4 pc - fall in ARV FDF volumes ( down 20 pc ) compensated by good growth in developed market exports ( up 25 pc )

Bio - 43 vs 50 cr, down 14 pc - stable Qtr with healthy traction in bio CDMO services. Initiated discussions with several strategic customers for long term CDMO collaboration. Commercial fermentation facility build up on track in Vizag

Company’s manufacturing footprint -

Vishakhapatnam -

Unit - 1 @ Parawada - 1279 KL - APIs + CDMO

Unit -2 @ Atchutapuram - 89KL, 10 billion units - APIs + FDFs

Unit -3 @ Parawada - 2318 KL - APIs + R&D

Unit - 4 @ Atchutapuram - 1959 KL - APIs + CDMO

Unit - 5 @ Parawada - 161 KL - CDMO

Unit - 6 @ Atchutapuram - 1479 KL - APIs

LSPL - 1 @ Parawada - 139 KL - APIs + CDMO

LSPL - 2 @ Atchutapuram - 283 KL - CDMO

Hyderabad -

Sriam - 81 KL - APIs

Kilolab - 4.5 KL - APIs + CDMO + R&D

New R&D center - under development

Bengaluru -

R1 - 15 KL - Bio synthesis + R&D

R2 - 225 KL - Bio synthesis

Kanpur -

Gene Therapy - R&D

Marketing offices -

Winchester - UK

Hamburg - Germany

New Jersey - US

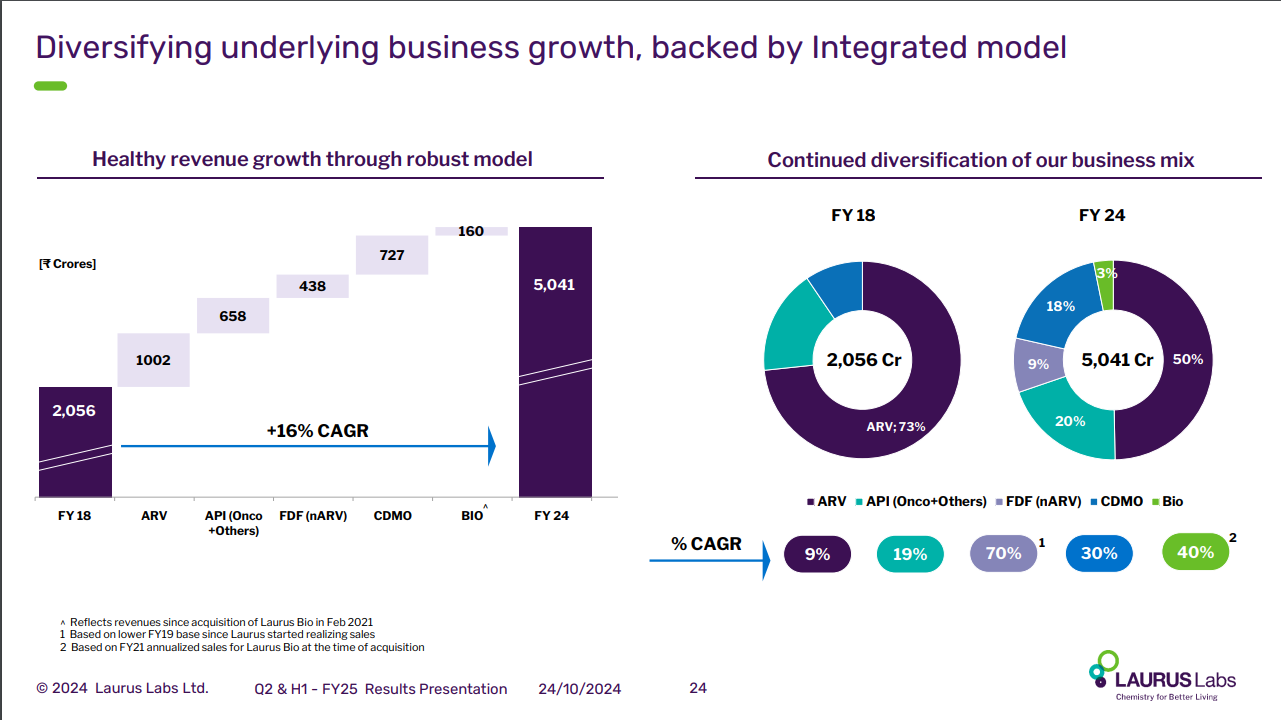

Company has spent very aggressively ( @ 2600 cr ) on Capex in last 3 yrs. Hence, most of its manufacturing facilities are under-utilised. As their capacity utilisation improves, so shall company’s profitability

Company has signed a new long term CMO contract for FDFs with a new customer. Customer is also funding CAPEX for the subject supplies that are expected to begin in FY 27

Company has also spent a lot of money ( @ 470 cr ) on cell and gene therapy + Bio catalaysis. Company is working on 10+ Bio Catalaysis projects with various customers

Animal health products - manufacturing facility is undergoing early ramp-up phase, commercial validation have started

Crop Protection products - manufacturing facility’s inspection and qualification is expected by end of FY 25

Company has formed a 49:51 JV with a Slovenian healthcare company - KRKA ( in Feb 24 ) to manufacture and market formulations in India and non EU mkts

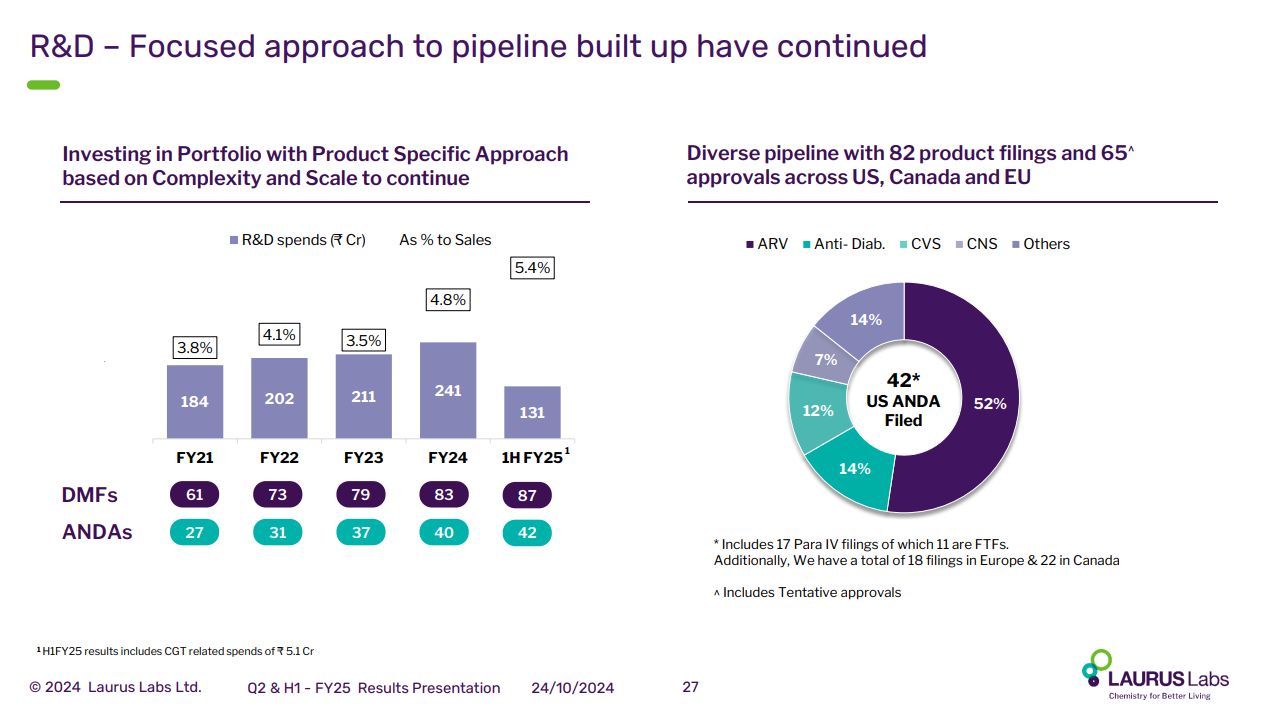

Company has - till date filed 41 ANDAs in US mkts and has obtained 21 final approvals, 14 tentative approvals. Their current formulations R&D has 62 products in the pipeline

R&D spends in Q1 were at 5.4 pc of topline ( healthy levels ) - up 35 pc YoY

Company is in the process of setting up a Bio - Fermentation manufacturing facility in Vishakhapatnam. Likely to be commissioned by June 26. Total capex requirement for this facility should be around 200 cr

Company passed 02 USFDA inspections in Q1 - at their large API manufacturing sites - Parawada -1 & 3 - without major observations - a key positive

Net Debt stands @ 2633 cr

Company also hosted / has undergone 14 customer audits by CDMO customers in Q1 ( that’s a large number ). Company is definitely seeing greater interest from customers from West for their facilities for potential award of late stage CDMO contracts

Company has increased its count of scientists working on CDMO division from 200 in 2019 to 800 scientists currently. That’s a huge jump and this also costs a lot of money ( operational expenses ). This should bear fruit as the CDMO division’s revenues pick up

ARV API + ARV Formulations sales for Q1 stand @ 552 cr ( out of a total topline of 1195 cr )

As their animal health and other important CDMO contracts pick up wef H2 this year and their crop protection product deliveries start next year, the percentage of business coming from ARVs should start to fall meaningfully - that would be a key positive for the company as ARV part of the business is unlikely to grow in future

Company is guiding for a consolidated EBITDA margin of 20 pc for full FY 25

Capex guidance for next 2 yrs @ 1800 - 2000 cr !!! ( majority of that for CDMO business )

The pickup in CDMO business in H2 that company is talking about is supply of materials for product registrations post Phase-3. Hence, logically - a lot of commercial scale manufacturing should come their way in FY 26

Disc : initiated a tracking position, intent is to hold on for next 6-9 months and look out for business improvement, not SEBI registered, not a buy/sell recommendation

20 Likes

Supplies of the HIV prevention medicine, PrEP, will begin to return to normal, with the Therapeutic Goods Administration and the Pharmaceutical Benefits Scheme listing a new manufacturer, Laurus Labs to help overcome a shortage.

Australian PrEP Supply to Ease Soon | Mirage News

3 Likes

The Therapeutic Goods Administration (TGA) has temporarily approved Laurus Labs, Emtricitabine and Tenofovir Disoproxil Fumarate 200 mg/300 mg Tablets until 31 January 2025.

6 Likes

1.What kind of moats can a CDMO business have over other CDMO businesses?

2.Diworsification at work. Agree or not?

Laurus good summary of last 6 years progress.

R&D Spend and Current pipeline. 17 Para IV of which 11 are FTFs

5 Likes

7dc7fcbb-ed78-4011-ae2a-91d6eae6891c.pdf (558.3 KB)

Highlights from the recent con call and my findings:

- Revenue New revenue streams Animal health and Crop Science in coming years 2-3. Formulation segment (good margins) is also expected to contribute.

- Margin expectations in the coming quarters Management gave a guidance for 20% EBITDA margin for the full year for the current FY. The first half had a margin of 14-15% so one should expect a margin of 23-25% in the next two quarters which can go on for the next few financial years.

- This anticipated improvement is attributed to a strong order book and scheduled deliveries, particularly within the CDMO segment.

- This year growth is driven by the CDMO segment

- CDMO division is expected to drive the majority of the growth in FY25, the management anticipates growth across all segments, including Generic API and FDF in the coming years Q4 call will give a much better picture

- Operating deleverage the company is going through a deleverage phase due to the cap ex in the growth initiatives along with the challenges in the generic API segment

- Operating deleverage ends the management mentioned that the deleverage may have ended and we can expect the leverage to come into play after one or two quarters

- Cap ex plan of 2000 cr: Majorly of which will be in the CDMO, around 200 cr in Formulation segment, api will receive the lowest share.

- Growth triggers: Continued CDMO Growth (already doing well and good quarters expected), New Revenue Streams from Animal Health and Crop Sciences (in 2-3 years), Generic API Growth Through Portfolio Expansion (Currently struggling and going through deleverage because of the expansion but deleverage has ended as per management and leverage can kick in after few quarters which can improve margins), Formulations Business Expansion (good margin business can move up in the value chain)

Next 2-3 years outlook is good as of now with good capital appreciation as per me.

Disclaimer: Invested. Not a recommendation.

11 Likes

2 Likes

Approval of investment worth 1.6 Billion Rupees

2 Likes

there has been a lot of promoter buying in the script in Dec 2024 . Probably good times ahead

Source : https://www.nseindia.com/companies-listing/corporate-filings-pit-annual

Disclosure : Invested and Biased

I don’t see any exchange notification for this. They should have notified it to the exchanges.

check in the link you will find all the info …

4 Likes

Couldn’t find anything here ? Can you point me exactly where this was released as a disclosure ? He couldn’t have done such a large transaction without a proper SAST disclosure.

Search by Company Name “Laurus Labs Limited” in the search box and select Laurus Labs from the dropdown .

It has data since 2020 which can be downloaded in excel and this is the first time since 2021 where there has been such big acquisitions by the promoters . However , 2021 was different as promoters sold way more to release their pledge

2 Likes

Does this pass compliance norms? I mean, since promoters have inside information, can they pledge their existing holdings to buy more shares and then sell their shares at a higher value to release the pledge?

Also, how do you know that the shares were pledged for exactly this purpose of buying more shares and not for something else?

4 Likes

Laurus Labs Limited Satyanarayana Chava Promoter And Designated Person Equity 15,70,000 - - - 09-Dec-2024 09-Dec-2024

9th December price is quite high, he is buying close to 580 to 590 levels.

3 Likes

@Vikky9995, I too think debt is a better option when the going is good, Shell out 6 to 7%, and rest is for you to internally grow. Therein equity is a costlier funding option - you have larger profits - of the interest payment saved; and pay higher tax thereon, but share the kitty among larger no of shareholders (or bigger).

but if the going is not good, and you don’t earn worth the liability (interest due) God forbid!

The members here are generally wise enough, so former situation is better. But if one is speculating; make sure the debt is low and is well covered.

1 Like

Good results from Laurus labs.

Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/40f6294a-0346-4a9a-9dc8-baf1790984ae.pdf

Investor Presentation:

6 Likes