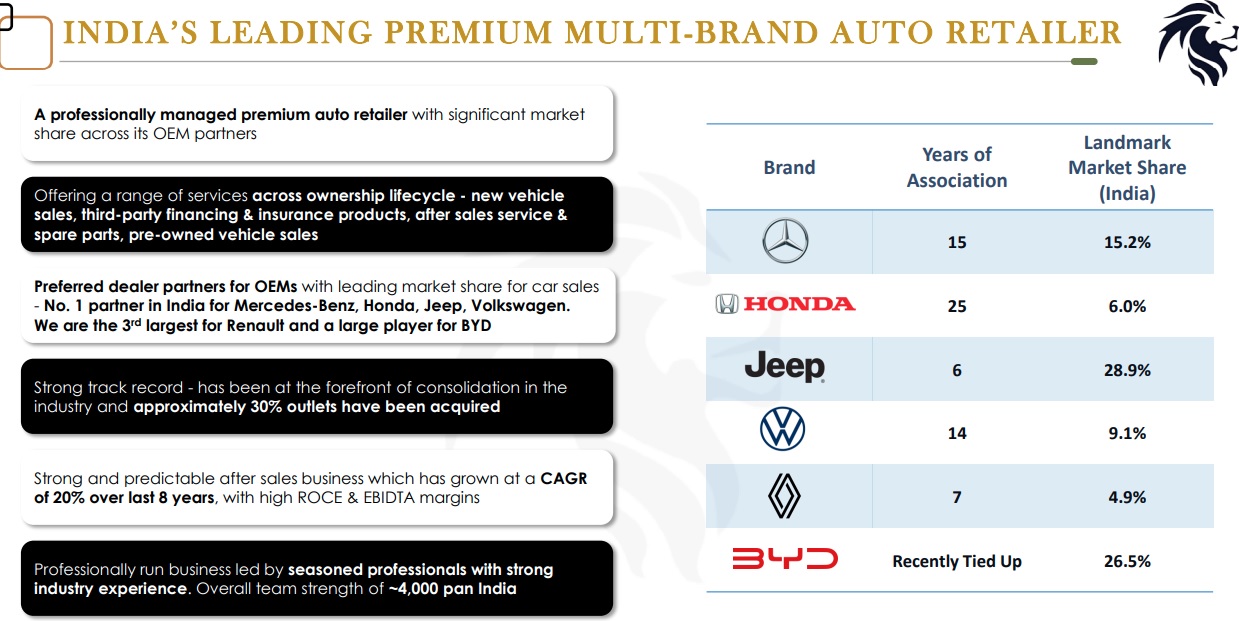

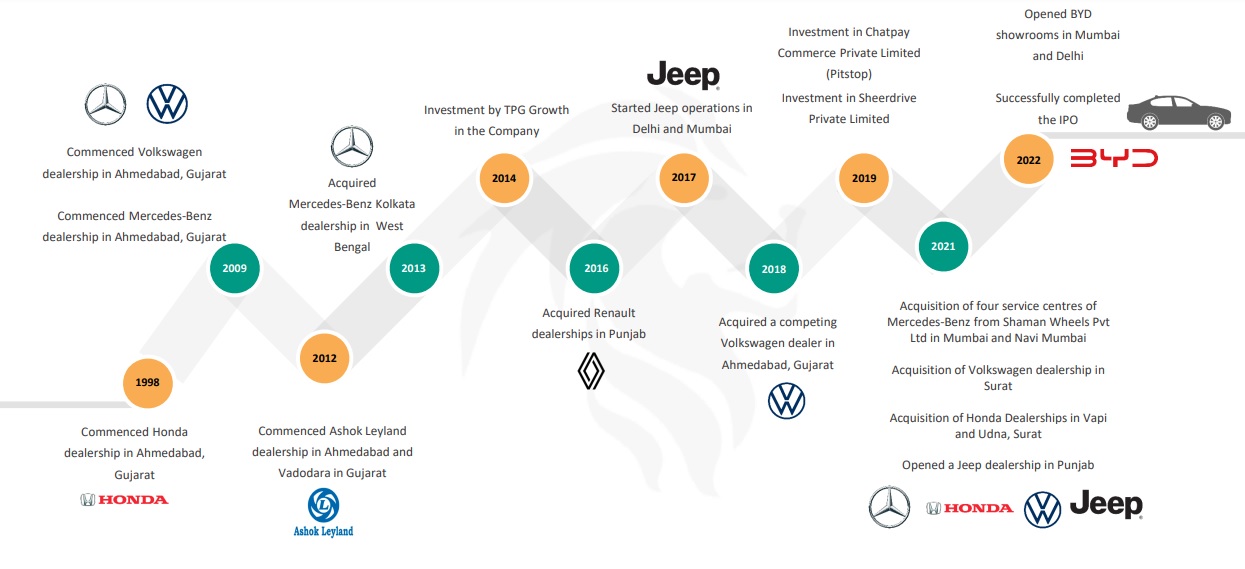

Leading and only listed car & CV seller in India - deals in luxury car segment (Merc, Jeep, VW, Honda, BYD & Ashok Leyland(CV)) - Company exiting Renault cars as renault has future plans to launch cars in affordable low price segment. Landmark want to focus on premium & Luxury segment.

Overall market- India has become 3rd largest car market in the world and growing at good CAGR owing to increasing purchasing capacity. Shift towards high end cars is clearly visible as sales of SUV segment is growing rapidly. People are looking beyond Maruti Suzuki & Tata cars.

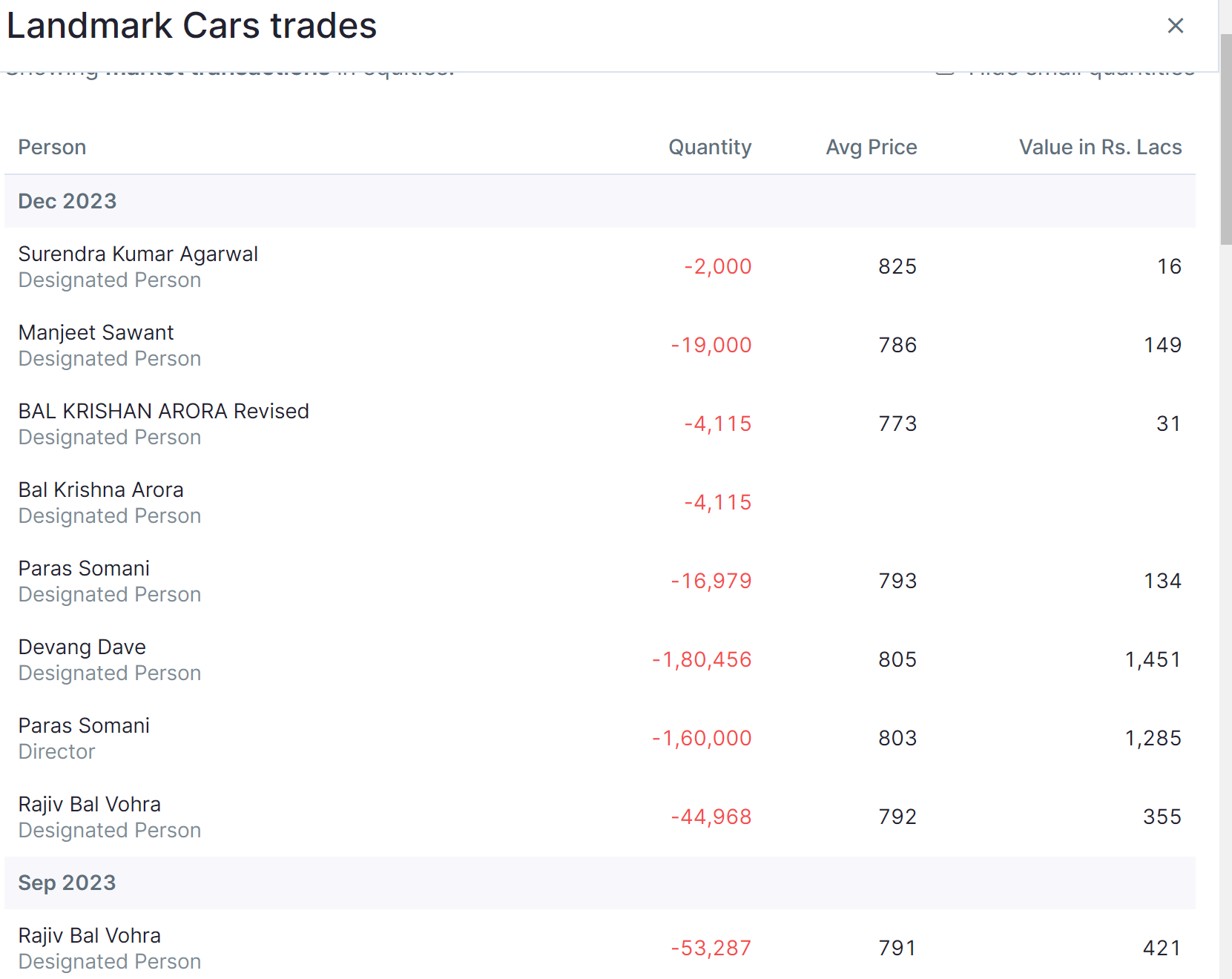

Share of BYD is abnormal as it is new entrant in Inida (Landmark owns showrooms in Delhi & Mumbai areas for BYD).

Business Sub-segments:

-

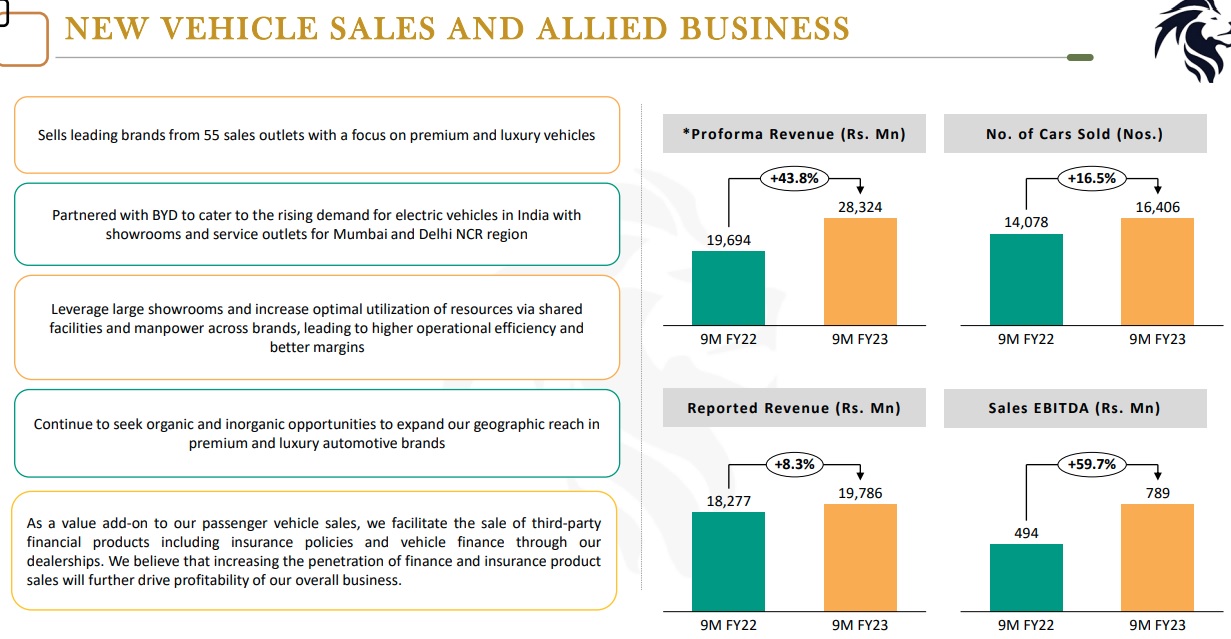

New Car Sales: Low margin / medium-high growth business

-

Service : Growing at 20% + CAGR, Kind of annuity business as premium vehicles mostly gets serviced at authorized centers only (as per concall 50% + footfall even after 5 years of selling), ALso holds exclusive license for few premium accessories like permaguard & motorone car care brands

-

Allied business - Insurance & financial products, Second hand car sales - Low margin & low revenue business

Thesis:

- Entire bet is on growing band & disposable income of Indian higher middle & higher class.

- Shift of people from economic to premium/luxury cars

- Higher use of electronics in cars will make sure, cars are serviced/repaired at authorized centers only

- High sales numbers will widen the annuity service segment revenue for next few years (at least 5)

Anti-Thesis:

- Discretionary spending product - recession/low growth will hit hard on business

- Attached Brands don’t perform as good as rival brands (Hyundai is gaining market share but Honda is losing share.

- High working Capital requirement as they buy from company & then sell to customers except Merc (model changed in 2022- now company directly bill in name of customer & dealer gets his share of commission, helpful in improving WC of dealer)

Disc: tracking position