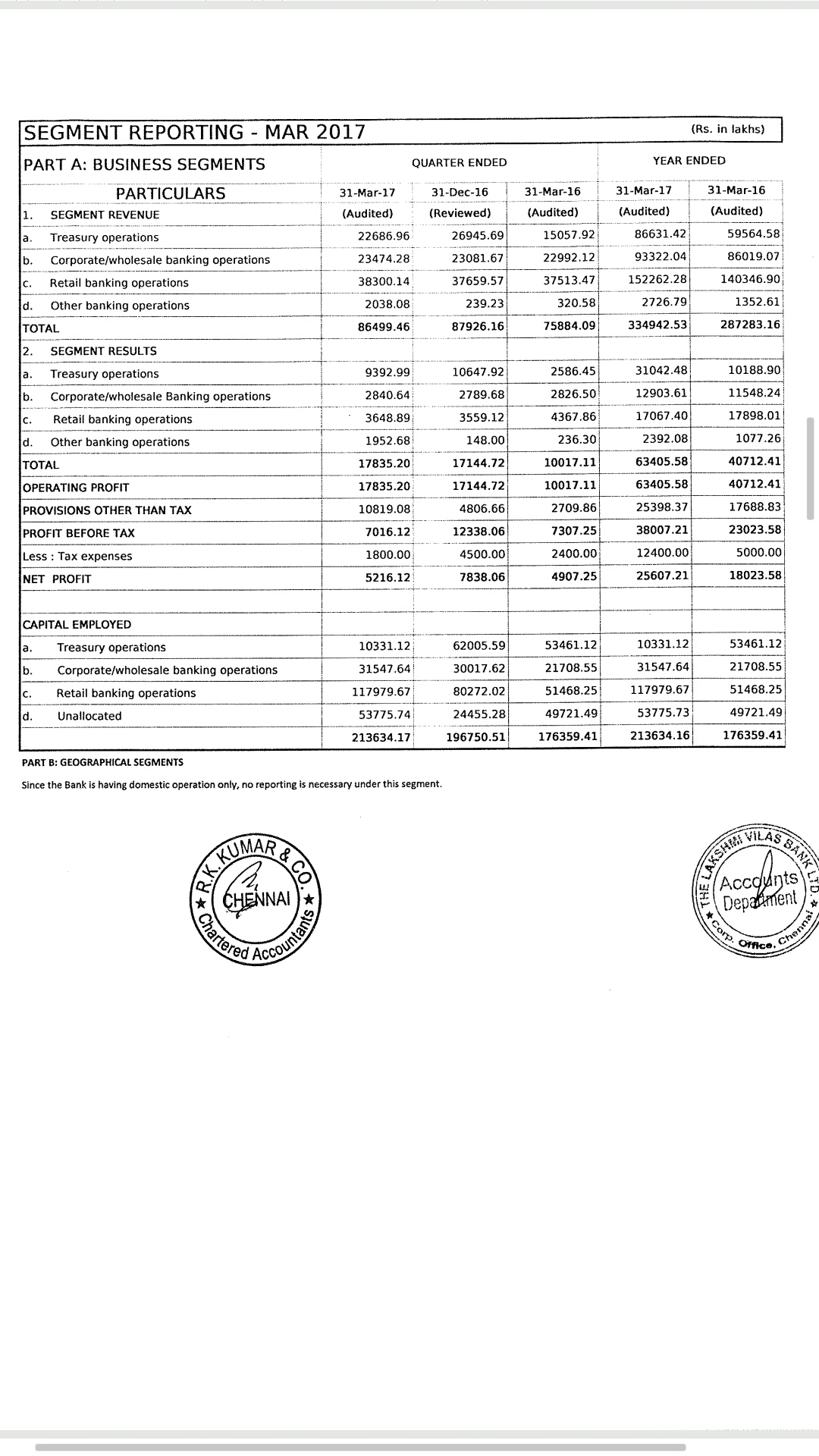

Market Cap: 3492 cr

CMP: 178.95

P/E: 13.38

Dividend Yield: 1.57%

P/B: 1.85

-

LVB is a 90 year old regional bank in Tamil Nadu with 500 branches with 271 in the state of Tamil Nadu. Nearly 50% of the business of the bank comes from the state of Tamil Nadu.

-

This year, the bank crossed Rs. 50000 cr business milestone(Deposits Rs. 30553 cr and Advances Rs. 23958 cr)

-

Total Deposit have grown by 20.14%(Rs. 30553 cr) y-o-y

-

CASA Deposits have grown by 32.24% (Rs. 5838 cr) y-oy. Current CASA figure is 19.11% and the management’s goal is to increase the number. And going by their last two years performance, one can see this growth.

-

Traditionally, their major source of income(Interest from Advances) was from Corporate loan book.

-

The new management, under the leadership of Parthasarathi Mukherjee, acknowledged their limitation of small bank, and now has the focus on increasing their retail/sme lending.

-

“We are moving away from large corporates, which is not our cup of tea…. We are a smaller bank. So, it is better to concentrate on smaller advances, where we have local knowledge and local understanding of the businesses. So, we believe that is where we have the DNA. And we are trying to leverage on that DNA,” - NS Venkatesh, Executive Director.

-

“Currently, 50.8 per cent and 49.2 per cent of the bank’s loan portfolio comprise loans to large corporate, and RAM(Retail, Agriculture and MSME) and commercial banking segments, respectively. This bank plans to change the loan mix between large corporate, and RAM and commercial banking to 25: 75.”

-

Advances have gone up by 20.89% to Rs. 23958 cr and the yields have slightly dropped by 92bps to 11.29%

-

FY’17 Revenue was Rs. 2846 cr(up by 10.84% y-o-y) and Net Profit was Rs. 256 cr(up by 42.08% y-o-y).

-

Last five years, the net profit growth was 12.73%, sales was 19.25% and roe was 10.46%

-

Dividend Payout has increased from last three years from 16.36% to 29.86%.

-

Total number of branches has increased from 292 to 500 since 2013.

-

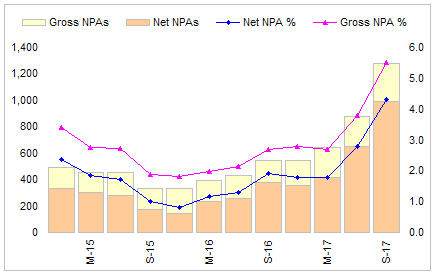

Gross NPA increased from 1.97% to 2.67% and Net NPA increased from 1.18% to 1.76%.

-

Capital Adequacy Ratio: Tier 1 capital @ 10.48% and Tier 2 Capital @ 10.38%.

For the first time since inception in 1926, the bank raised capital at 168 cr from institutional investor and may raise again.

Investment Rationale:

-

New Management: LVB appointed Parthsarthy Mukherjee, a chemistry graduate from Kolkatta Presidency College, who was an Axis bank veteran for the last 20 years. He has completely changed the top management by introducing new team members from prestigious banks like HDFC, Axis and Royal Bank of Scotland. NS Venkatesh joined from IDBI as Executive Director. RVS Sridhar, who was earlier at Axis is now the new Chief Risk Officer. Govind Ravindran has assumed the role of head consumer lending after serving HDFC for about 15 years in business development. Madhusudan Rao has joined as Chief Customer Service from SBI and Peeush Jain has joined as head of business partnership and transformation. S Venkatesh, formerly with RBL Bank, is heading the credit and wholesale banking at LVB. B Nedumaran, who was with Ma Foi HR consultancy, is looking after human resources.

-

Vision 2020: In 2016, Parthasarthy introduced vision 2020 where he set milestones. He stated that he wanted to increase the branch network from 460 to 500 in 2017 and 750 in 2020. He has achieved the 500 branch milestone. His target is 20-25% of annual growth for the next ten years.

-

“Mukherjee said by 2026, the overall business, including advances and deposits, should be up to nine times higher than the current Rs 45,000 crore. The profit should be 15-20 times higher than the usual run rate. The bank will also focus on pushing the share of low-cost current and savings account deposits up to 25% by 2020 from 14.5% now, and to over 35% by 2026. As part of the strategy, the bank will bring down the composition of corporate loans to 25% from 42% now and will focus on the higher earning retail and SME loans. The cost to income ratio, which is currently 57% would be brought down to 45%, at par with the industry level by FY20.” Source: HDFC Securities Research Report

-

Focus on Retail/MSME: This is a key area of focus for the banks where they are backing on their strength of concentrated branch network and deep relationship with the customer. They want to reduce their exposure to corporate loan and focus more on retail and msme loan. In 2016, they had 2.71 mn customers((14% metropolitan, 17% rural and 28% urban). Although, 50% of their branches are in TN, rest of the 50% is pan-india.

-

Consistent Dividend Payout: The bank has a decent dividend yield of 1.57% and in the last three years, their dividend payout has increased from 16.36% to 29.87%.

Risks:

-

Concentration: As mentioned above, having 50% of branches in TN exposes the bank to concentrated risks. This risk will be in all regional banks and the ability of the bank to expand in other state will be mitigate this

-

New Management: Although, individually the new management personnel may have performed in their previous role, can they work as a team and turnaround is yet to be seen. A lot will depend on Parthasarthy Mukhejees leadership. This situation is very similar to IndusInd CEO Ramesh Sobti who turnaround the bank and results are for everyone to see.

-

Competition: Since this is a small bank and a regional player, there is high chance that it loses market share to big banks. Although, markets have been very bullish about regional banks like Fedral bank, karnataka bank, etc. we have to see how these small banks are able to survive the current competition from the HDFC and Kotaks of the world

-

NPA: Although, the bank wants to focus on the retail and MSME loans, their previous corporate loan can drag the bank down. In 2016, their top sectors break-up of advances include infrastructure(7.16%), Textile(4.82%), Base Metals(4.56%), Food Processing(1.27%) and Chemicals(1.33%). With the new NPA resolution framework introduced by the government, the Bank will have to take tough decisions and provisions might go up. This might impact their future fundraising plans. The bank wants to raise 600 cr. of which 168 have already been raised.

Valuation:

The bank currently is trading at a trailing PE of 13.38 and a PB of 1.85. The ROE of the bank is 11.75% and with the measures taken by the management this number can go up. The stock price is fairly valued but compared to other regional banks like Federal bank or RBL bank appears cheap.

Disclosure: The author Invested @ 138 in November. The author is not a Sebi Registered advisor. Please do your own due diligence before investing.