LACTOSE INDIA (CMP Rs 46.6, Mkt Cap Rs 39 cr)

Lactose India (founded in 1991) is one of the leading producer of lactose in India with 40% market share. Clients include large pharma companies like Abott, Astra Zeneca, Wyeth, Bayer, Cadila, etc. Company has recently started focusing on Finished Pharma Formulations and API. What has been the potential game changer for the company is its agreement with Kerry (since Sep 2011) and its putting up of Lactulose plant of 2400MT/Annum.

Investment Highlights

1) Significant Capacity expansion undertaken since FY11. Benefits of the same expected over next couple of years.

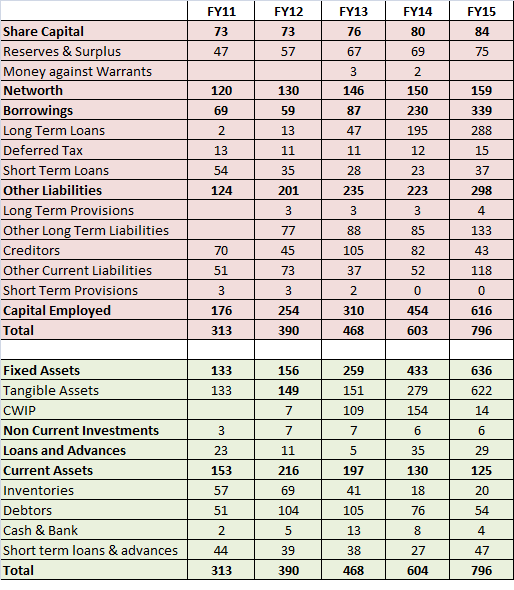

2) Kerry agreement in FY 12 has likely changed course for the company with significant capex undertaken post that. Fixed assets have grown from Rs 15cr in FY12 to Rs 63cr in FY15.

Understanding Kerry Transaction

Kerry Transaction

Kerry Advance explained as Note 33 in AR FY12

During the year, based on certain commercial negotiations, the Company has received from Kerry Ingredients Private Limited a sum of 7,67,72,000 for expansion of production capacity and others measures for strengthening of business and 3,36,81,113 as an advance against goods to be supplied by the Company. The final terms & conditions of these transactions are still under negotiation. Till then the said amounts have been reflected as “other long term liabilities” and “advance from customers” respectively in the financial statements.

My comment – Rs 11.04 cr received from Kerry. Rs 7.67cr shown as other long term liabilities and Rs 3.36cr as advance against goods supplied. Asset side as Cash.

Kerry Transaction as explained in Note 33 in AR FY 13

a) During the F.Y 2011-12, the Company had received from Kerry Ingredients India Private Limited (Kerry) a sum of Rs. 767.72 lacs for expansion of production capacity and others measures for strengthening of business and the same had been reflected as Liabilities in the financial statements for the year ended 31st March 2012 in absence of any agreement with Kerry.

b) During the current year, the Company has executed a Manufacturing Agreement with Kerry on 11th January, 2013 and as per the terms of the agreement the said sum Rs. 767.72 has been received as follows:

i. Rs. 190 Lacs has been received for the purchase of Company’s customers for such products. The said sum will be accounted for as Income in the year when the Company’s customers will be transferred to Kerry.

ii. Rs. 577.72 Lacs has been received as Advance Manufacturing Consideration by the Company on having agreed to upgrade its plant and produce up to 10000 metric tons 200 Mesh Lactose per year exclusively for Kerry. This Consideration shall be apportioned over a period of 10 years from the commencement date which is the date on which the Company commences the production of the upgraded manufacturing facility as agreed in the Manufacturing Agreement.

Accordingly, the said sum of Rs. 767.72 Lacs has been reflected as current / long term liability as the case may in the in the Financial Statements for the year ended 31st March 2013.

My comment – Rs 5.77cr used for capex and could be reflected in P&L once plant commissions.

AR FY 14 Details of Kerry Transaction

Note 30

Note: The Company had during the earlier years received an amount of Rs. 1,90,00,000 from Kerry Ingredients Private Limited (KIIPL) for transfer of Company’s customers as per the manufacturing agreement executed on 11th January, 2013. During the Current year in terms of Manufacturing Agreement, the Comapny has transferred its entire customers to KIIPL and accordingly the amount received has been recognized as income under exceptional item.

My comment –

Rs 1.9cr have been recognized in income after transferring customers.

Rs 5.77cr and Rs 3.36cr yet to show in P&L. Rs 5.77cr used for capex and Rs 3.36cr against future supply of goods.

AR FY15 (Kerry and Sanofi)

Note 37 :

a) During the FY 2013-14, the Company had commenced production of its upgraded manufacturing facility to manufacture up to 10000 metric tons 200 Mesh Lactose per year exclusively for Kerry Ingredients India Private Limited (KIIPL) and accordingly as per the manufacturing agreement with KIIPL , has recognised during the year income of 57,77,200 (P.Y. 33,70,033/-) on proportionate basis out of total Advance Manufacturing Consideration amounting to 5,77,72,000 and the balance of 57,77,200/ - (P.Y. 57,77,200/- is disclosed under the head “Other Current liability” and 4,28,47,561/-(P.Y. ` 4,86,24,767/-) is disclosed under the head “Other Long term liability”.

b) During the year, Company has received an advance amounting to 2,60,00,000/- from Sanofi India Limited for procurement of machinery, equipment and carrying out civil work for structural modification of manufacturing facility exclusively meant for Sanofi India Limited through an agreement dated 10th April, 2014 and addendum thereto dated 1st January, 2015.As per said agreement, advance payment is to be adjusted by way of monthly deductions by Sanofi India Limited equivalent to 20% of the Conversion and Packaging charges billed to Sanofi India Limited by Lactose (India) Limited from F.Y 2015-2016.Accordingly, out of advance of 2,60,00,000/-, 36,00,000/- is disclosed under the head “Other Current liability” and 2,24,00,000/- is disclosed under the head “Other Long term liability” on estimated basis.

My Comment –

Lactose India has ramped up production of Lactose from 3500MT to 11000MT (exclusively meant for Kerry). This assures demand clarity. According to management, Kerry wants to further enhance lactose sourcing but Lactose India wants to stabilize current capacity before adding more.

Sanofi agreement is on similar lines to Kerry. Thus, Lactose India is becoming more of contract manufacturer for MNCs with asset light model.

3) Promoter has issued warrants at Rs 12.5/share in FY14 and at Rs 27.5/share recently in August 2015. Promoter stake has increased from 28%(since Kerry transaction) to 38% and will potentially increase to 46% (post conversion of recent warrants)

- Capacity expansion has been largely funded through debt (Long term + Short term). Debt has increased from Rs 5cr in FY12 to Rs 32cr in FY15. The reason for highlighting this point is when bank funds capacity of company with market cap of Rs 12-15cr to the tune of Rs 25cr, there has to be very good clarity on demand.

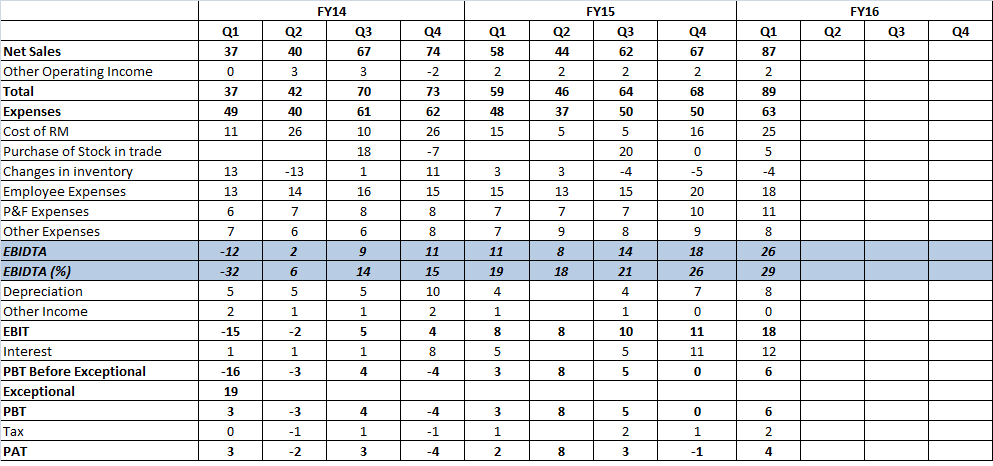

5) Company’s margins have shown very good improvement (steadily) over past few quarters from 15% in Q4 FY14 to 29% in Q1 FY16.

6) Company has put up 2400MT/annum Lactulose plant which should add to numbers in FY17. This can add to Sales to the tune of Rs 55-60cr. (Capex for Lactulose has be Rs 30cr).

Financial Tables

Balance Sheet (Rs mn)

- Sharp increase in FA from Rs 15cr in FY12 to Rs 63cr (benefit likely to come over FY17 & FY18.

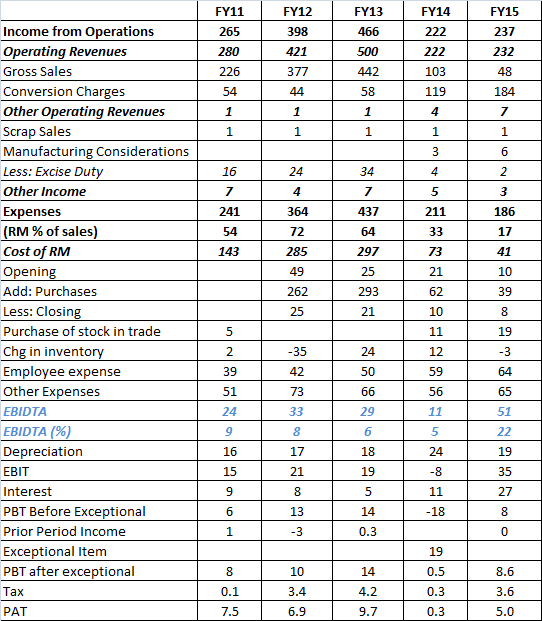

Profit & Loss

P&L Quarterly

EBIDTA margins have smartly improved from 15% in Q4 FY14 to 29% in Q1 FY16. Largely due to asset light model and contract work undertaken by the company.

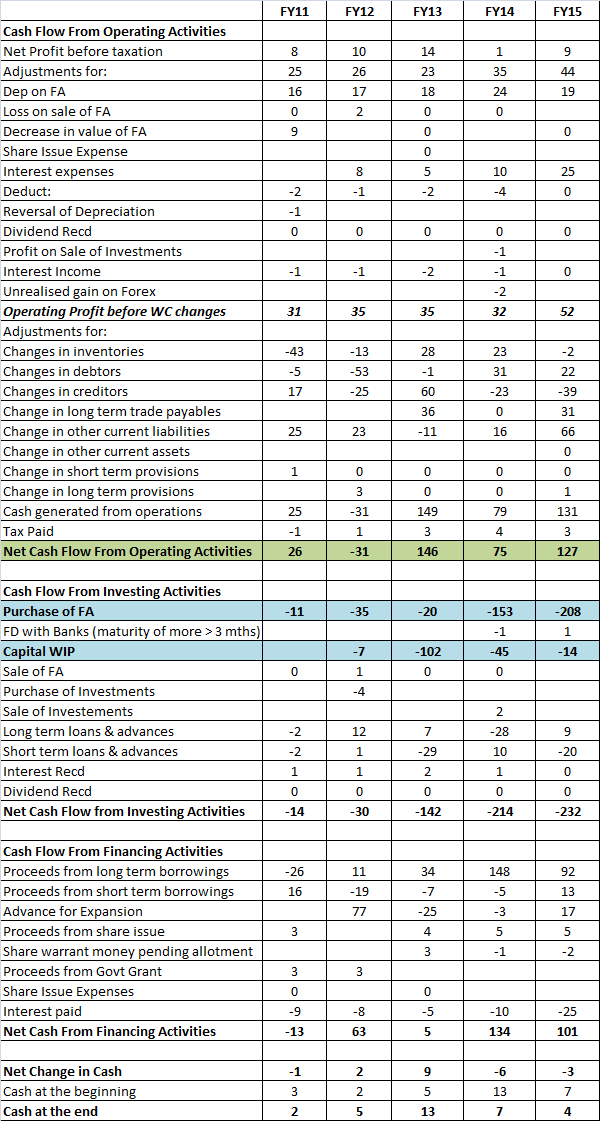

Cash Flows

Lactose has enjoyed good operating cash flows over last 3 years.

Company has undertaken massive capex and has spent close to Rs 55cr on fixed assets over last 3 years.

Investment Summary in Brief

With very big capex and demand largely tied up, financial performance can sharply improve over next couple of years.

Due to asset light model EBIDTA margins have sharply improved. Existing business can do sales of Rs 45-50cr and Lactulose can add another Rs 55-60cr. Based on 20-25% EBIDTA , Lactose India can do EBIDTA of Rs 20-25cr in FY17/FY18 (depending on ramping up of capacity). ROE and ROCE will be quite high over coming years.

Company’s Website - www.lactoseindialimited.com (contains useful information)

Disclosure - Invested.