Interesting.

Could you share the source.

Also, any specific reason for borosil growing faster than La opala other than the low base?

Interesting.

Could you share the source.

Also, any specific reason for borosil growing faster than La opala other than the low base?

La opala has lost agression on ground to borosil/cello.

My reckoning is : their capacity is full and hence not adding more dealers/distributors. Post capacity expansion of 12000 MTPA, should focus.

However lots of distribution changes on ground. Dealers are losing confidence.

Need to focus on marketing as well as aligning the distribution

Anyone with alternate views?

Plenty of cheap chinese import in glassware and opalware is probably hitting the company. Most shops I visited have huge stocks of Chinese and other smaller local players. Laopala finds very little shelf space.

Company needs to focus on their marketing.

Update :

They consider Maharashtra as a weak market and all the distributor churn has been in the Maharashtra market. Rest markets are fine.

Post Capacity coming on stream, they will focus on marketing and sales (the capacity addition will put pressure on them to deliver)

Yes you may be right.

I am new to valuepickr and surprised to see how nicely the analysis is being done. Genesis has been established solely to invest in La Opala. The expenses in P/L, B/S, Investments etc of Genesis is pathetic.

But… La Opala as a company is not just a market leader but also a market creator. I love the business and growth prospect once the capacity expansion is operational properly and hopefully some agressive marketing and advertising is done.

On a side note…My mother keeps gifting its crockery sets to everyone.

AGM22

Opalware

Crystalware

Borosilicate

Misc

Disc - No investments

I have a retail shop in Pune and Cello has been very aggressive in its sales and marketing campaign, they provide better dealer margins and are also priced lower than la opala and have better and unique designs, it is difficult to maintain many designs as it increases shelf space and inventory, so we are now mostly selling cello dinner sets, very good demand I would say. Competition is heating as cello is planning capacity expansion and also a new plant for borosilicate glass division in direct competition to La Opala.

I would disagree with you as we retail opalware dinner sets borosil is equally god, to be honest there is some minor difference between opalware of la opala, borosil and cello, cello is a bit better because it is much resistance to breakage and we primarily push cello to customers.

Chinese imports are mostly sold through the black market via under invoicing, Indian players who are organised will grab market share.

Hi All,

Please find below analysis done on La Opala. Do let me know if I have missed on anything in this analysis

| Date of report: | 21-04-2024 | Competitor PE | 43.9 | Sector | Glassware |

|---|---|---|---|---|---|

| CMP: | 322 | Current PE | 26.8 | No of Years | 37 |

| Market Cap: | 3569 Cr | Highest PE | 71 | Key Products | Opalware Crockery |

| ROCE / ROE | 22.1% / 16% | Lowest PE | 8.4 | Key Competitor | Borosil, Cello, Unorganised Sector |

Background: A company in Tableware sector specializing in opalware crockery with 50% market share of organized sector and with upside potential of 2.1 times within 3 years. Today the company is cheaply valued as of current price and will be able to generate 2.1 times return in 3 years.

Business Model and Analysis

Overview:

Co produces opal glass tableware from entry level to premium catering to all type of customers. Co also produces items of Borosilicate to cater to “Cook Serve Store” Range

Industry Growth:

Industry for opalware is expected to grow around 6% CAGR till 2030. Growth in industry is primarily due to higher disposable income, increasing middle class base, increasing events and social parties and influence from social media to make home look more “aesthetic”

Capacity Utilisation:

The company has 2 plants one in Uttarakhand and one in Jharkhand. Plants are working at capacity.

Opportunities:

In opalware company operates at 3 price point under different brand to cater to entry level consumer to premium consumer. Co continuously innovates new designs to make its product in trend with market and create brand image. Co has a large market to penetrate as many consumers use unbranded tableware. Further imposing of anti-dumping duties by Indian govt over China and UAE market has made market penetration easier. Inflation for 24/25 is projected to be lower than 23/24 which will provide high disposable income in hands of consumer. The company has increased its number of distributors by 67% in last 3 years to avoid stock out situations. Co exports products in 30 countries which comprises of 10% of its Revenue. Exploring foreign markets will help in increasing topline and bottom line.

Risk:

The company has biggest threat from unorganised sector which operates at lower price point than the company. Entry level consumers are not concerned over brand and looks at price point while buying product. Creating a brand takes a long lead time and historical sales data proves that sales are flattish over 2-3 years period before they take a leap of 30%-40%. Raw Materials like soda ash, borax, sodium silico fluoride, quartz powder although sourced locally are heavily susceptible to price fluctuations.

Future Expansion:

Company is venturing into borosilicate market and plant will commence operation from FY25/26. This business will give direct competition to Borosils’ lunchbox and microwave ware segment. The management is predicting to generate its current OPM level ie 38% in this segment which is doubtful as Borosil generate around 8% in this segment. Due to its widespread distributor segment, co will gain advantage in entering this market

Competion:

Further it is heavily vulnerable to competition from unorganised sector operating at low price points

Management:

The company is home run company run by its promoter, his son and daughter in law. Management is strong and has given sufficient information in it’s Annual returns. Further the management has not entered into any related party transaction. Promoters hold 65.64% share in company and has not pledged any share. Concerning points are that management takes around 12% of net profit as salary. Further there are no investor presentation or concalls available during the year by management.

Institutional Investor:

Institutinal investor are holding a steady 20% share in the company with HDFC (~6%) and DSP(~6%) being the constant shareholder*.*

Historical Data and Financials

Profit N Loss Account:

Balance Sheet:

Cash Flow:

Valuation:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Average |

|---|---|---|---|---|---|---|

| Price | 322 | 467 | 298 | 467 | 1.95 | |

| PE Ratio | 26.8 | 42.8 | 24.8 | 71 | 8.4 | 36.02 |

| EPS | 12.01 | 12.01 | 11.08 | 12.01 | 0.1 | 6.35 |

| Price/Book | 4.3 | 7.1 | 4 | 23.8 | 0.4 | 6.15 |

| EV/EBITDA | 18.8 | 27.1 | 17.4 | 44.4 | 0.5 | 22.27 |

| ROCE | 22% | 17% | 10% | 43% | 10% | 17.59% |

Company has demonstrated a strong P&L growth by venturing into new markets and by creating branks to cater to different customer segments. Further company has maintained a constant OPM of 38%. Company has maintained a lean Balance sheet by taking very less debt and funding its expansion activity by cash generated from operations. Excess Cash is either invested in good investments which help cover for other expenses, interest and depreciation costs. Company also repays back money to its shareholder in the form of dividend.

Future Growth:

| Amt (INR Cr) | 20/21 | 21/22 | 22/23 | 23/24 | 24/25E | 25/26 E | 26/27 E |

|---|---|---|---|---|---|---|---|

| Sales | 211 | 323 | 452 | 391 | 431 | 594 | 772 |

| GP | 69 | 122 | 172 | 151 | 164 | 190 | 246 |

| PBT | 64 | 117 | 165 | 160 | 157 | 182 | 237 |

| Net Profit | 50 | 87 | 123 | 133 | 115 | 133 | 173 |

| EPS | 4 | 8 | 11 | 12 | 10 | 12 | 16 |

| PE | 50 | 44 | 31 | 27 | 36 | 36 | 44 |

| Price | 222 | 347 | 340 | 322 | 370 | 429 | 682 |

Sales Growth :

Gross Profit:

Gross Profit rate is at 38% which company has maintained historically. For lunch and micro ware business, gross profit is considered at 8% same as Borosil.

PBT:

Company converts 96% of its gross margin into net profit due to low interest and depreciation cost and high interest income received from its investments.

Net Profit:

Tax rate is assumed to be at 27% same as Tax paid in last year

PE Calculation:

Disc- Invested

Had looked at the company last year, please correct me if things have changed since then till now.

Good business but the promoters are not willing to invest in the business nor paying out cash to the shareholders. Company is sitting on more than Rs.400 crores of cash which is invested in Bond funds. Lost money in Franklin Credit Fund fiasco. Rs.136 crores is invested in equity of Genesis Exports Ltd which is the holding company of the promoters which in turn holds 46 % in La Opala. This cross holding benefits only the promoters to the detriment of minority shareholders. You have pointed out about the high promoter salary and no information sharing with shareholders due to absence of investor concalls or presentations. There is scope for increasing dividends substantially since capex requirements are negligible. Capacity was raised in FY22, but sales growth has not happened since then. Overall, promoter interest to take company to greater heights seems missing.

With a slight change in management approach, the stock will get rerated as business has a lot of potential, but the promoters are not doing justice to it.

(Disc.: No positions)

Hey,

Following points have changed-

Following points remain constant-

I would like to ask, company has shown good sales growth. Why do you feel that management is not interested to take company to great heights? ![]()

I feel so because of the same points I mentioned. Retail businesses require heavy investments in distribution channel, brand building and marketing. The company can easily afford to do a lot more than what they have been traditionally doing. If things have changed in the last few months like you say that would be a good thing. Lack of adequate investor communication doesn’t help my case. Maybe I will revisit my thesis after this year’s Annual Report is published.

This is where we sorely need some scuttle butt volunteer . Company communication is limited …

Malolan

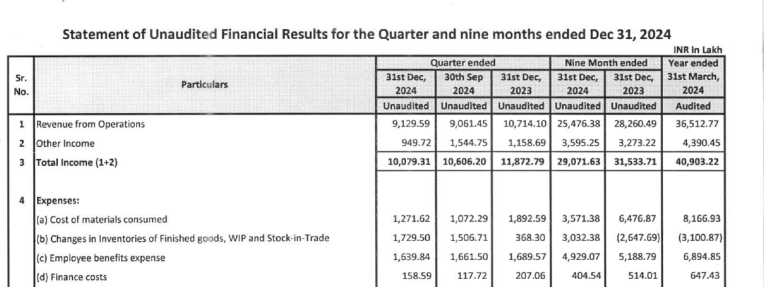

What do you guys think about the Q3 results?

For me i was quite disappointed but to be fair current price took plunge to reflect the same so net net valuation seems fair.

Does anyone has insight maybe as management does not do any concalls.

My 2 cents are this poor quarter was maybe due to shifting of their facility, liquidating higher cost inventory and maybe take 1-2 quarters to see operation stabilise

Seems your interpretation is correct…

Yes and also i saw that insider bought some shares too but insignificant some 65k odd

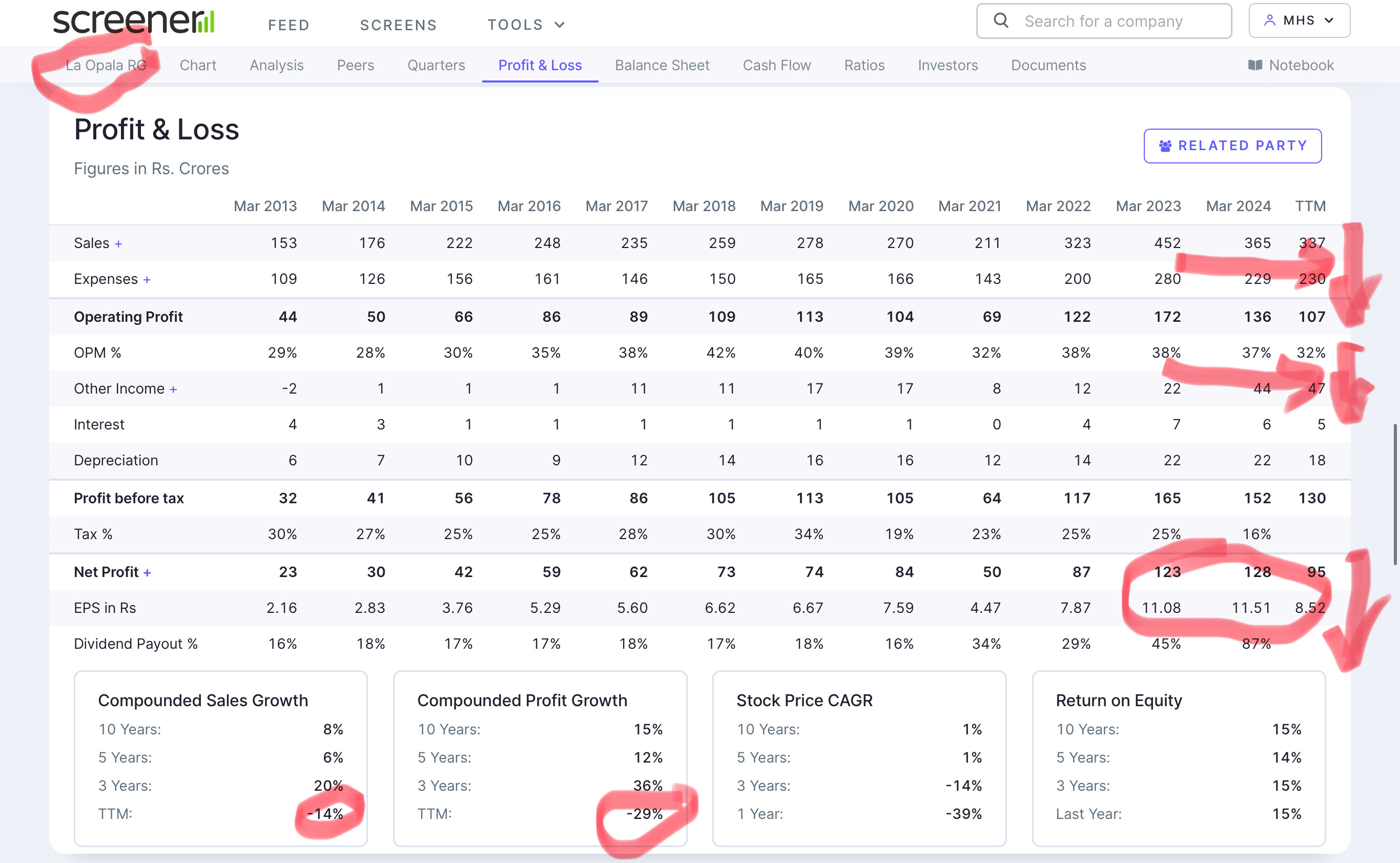

Last 3 years Sales CAGR is 20% and 3 years profit CAGR is 36% but stock price is -14% CAGR for last 3 years. What explains the continual decline of this stock?

Starting valuation,higher competitive intensity in sector & results might be plateaued for next 1-2 quarters before showing growth(in my opinion).

Disc: biased and recently bought some exposure