Can some one help me understand what could be the logic of the company in keeping 250+crores money in mutual funds under current investment?

Probably they don’t have any other better use of cash.

Maybe they have already done all the capital expenditures.

Personal guess.

Regards.

Vikas

I believe the promoters are typical conservative old fashioned family which believes in keeping cash for the “rainy day”. So they neither give large dividends, nor aggressively acquire companies/spend more on R&D, branding, sales promotion, reducing prices etc. Nothing wrong in being conservative, but it can be counter productive when you allow competition to come in and take market share away from you.

This is just my reading from outside. I could be completely wrong…

Disclosure : Watching as I am invested in La Opala’s competition

1 Like

I would argue that they might be destroying shareholder value if they are indeed thinking like that. If these cash equivalents translate into business expansion plans that is a different ball game but putting that money in stock market is completely baffling.

1 Like

Is Saurabh Mukerjea’s little champs portfolio invested in La Opala. How do you see its standing in front of competitors Asahi glass and Borosil in future.

Will it be able to get the growth back and demand the market position it used to in last decade, specially in opalware.

Are they trying something by following, which is as per their filling few months back

“To carry on the business of providing information technology,data processing,support service for software and hardware,support service for storage,disaster recovery and enterprise resource planning.”

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3a9f1f50-1059-4242-8aba-d02e5ec34988.pdf

Can someone share information, if he has gathered or can arrange to get it?

Not sure about this. Since they don’t conduct any concalls, one has to attend AGM or send email to CS to get some reply. Hope it is not “Diworsification” as it seems totally unrelated to their current business. Cash on books can make people take funny decisions…

I am aware about concall & media interaction by management, even writing to CS helps little as most of the questions are replied “can’t violate listing regulations”

Management is over cautious and don’t wish to explore more, seems they are satisfied with current TO / margins, which makes sense considering limited market of opalware. Although they have added a furnace which is expected to start production in current FY. Even their competitors have similar view about opalware. The point which bothers is they haven’t shown any indication of doing anything else.

Can’t disagree with your views on diworsification as even if they wish to try in mentioned competencies, the filed chosen by them is very low level and overcrowded with very minimal margin. I feel that this could be thought process of younger generation but personally I feel that the field chosen will not help.

Opalware has given them a good margin and anti-chinese protests may help them as well (mainly import duties etc).

Folks,

Just completed my annual report based research. I’m noting down some of the things that make this company interesting as well as some questions for our discussion

Things that make La Opala interesting

- Thinking- Yes, I was glad and refreshed hearing that they don’t see themselves as a tableware company but a company that provides experiences. This is a big point as consumer preferences change and if your thinking is rigid you will be left behind

- Product Laddering - Transition the customer to Opalware and then provide a product ladder with tiered pricing.

- Brand recall - Did a small research by asking my friends and family, and La Opala popped up nearly every time I asked them what brand they used. Gives me comfort!

- Tailwinds - China situation and extension of anti-dumping till 2022

- Competitive edge - They say that inventory is treated by distributors as Cash Equivalents. I believe this is huge advantage particularly in an industry where trade network and supply chain is the ADVANTAGE next to brand

- Investing in R&D facility though I’m not sure what is the thing they want to innovate.

BIG QUESTIONS

- Why the move to IT services as a new business?

- Exports & Crystalware sales have been sluggish. What’s their move here?

- How is the import-export split and what markets are they exploring for exports growth since opalware can be limited in india beyond a point

- Company increased capacity in 2017-18 but topline growth is not visible between FY18-20.

- 44% of their networth is in the form of cash and cash equivalents that sits neatly in Mutual funds. Now Mutual funds are sahi only for individuals and not shareholders so why so safe play here?

Would love to discuss this more and since some of you track competition can I as you to post some competitive summaries here if you can?

6 Likes

La Opala RG Ltd AR 2020 Notes

- The Company’s extensive distribution network is spread across India, comprising more than 200 distributors and 12,000 retailers. The Company focused on demand coming out of semi-urban India, addressing more than 600 towns with a population of 1,00,000+. Company also enjoys an international presence, exporting products to over 30 countries.

- Company intends to expand its manufacturing capacity by setting up a greenfield plant at Sitargunj. Due to Covid deferred the expansion plan at its Sitargunj unit by around six months, providing it breathing space till consumer demand revived. New plant capex will happen in FY22 now.

- From two furnaces comprising five manufacturing lines in our showpiece Sitargunj facility, we will have increased our capacity to three furnaces across eight manufacturing lines with the new capex.

- Rs. 270.01 Crore in revenues in 2019-20, a 2.91% decrease over the previous financial year. Rs. 84.27 Cr in profit after tax in 2019-20, a 13.82% increase over the previous financial year.

- Exports for FY20 at Rs. 35.60 cr compared to Rs. 39.37 cr in FY19. Exports at 13% of sales in FY20.

- Ended the year under review with Rs. 258.80 Crore cash on our books as on 31st March, 2020. Off this amount Rs. 54 cr is invested in Franklin India Short term Income Plan.

- The brand of the Company remained protected during the year under review. At La Opala, we believe that this was one of our most important achievements: at a time when markets and consumer sentiment were weak, it would have been easy to reduce our sticker prices with the objective to sell a large quantity. The management resisted this temptation to seek a short-term benefit at the expense of a long-term asset. The Company retained the price integrity of its products and protected its brand salience during the year under review. The result is that when consumer sentiment revives, we expect that the appeal of our products will have been retained.

- At La Opala, we continue to be optimistic of our longterm prospects because our product is mature, globally benchmarked for quality and priced lower than pure melamine and bone china. Your Company offers consumers products across price points, making them habit-forming.

- Company will focus on shrinking its receivables cycle during the current financial year.

- Covid19 Impact

- Lost almost 10 days of offtake and since this was the last week of the year, usually the most productive week through the year, the revenue ‘loss’ was estimated at around Rs. 15 Crore.

- One of the Company’s furnaces was under refurbishment in the last quarter of the year under review; this refurbishment was extended and the furnace remained deliberately inoperative through the first quarter of the current financial year, moderating manufacturing and inventory holding costs. The furnace will be brought back on stream as soon as the demand outlook revives.

- The lockdown has also impacted the hospitality and restaurant businesses which may make the investments of these institutions on premium crockery take a down-turn.

Regards

Harshit Goel

12 Likes

Went through the AR FY20. Some observations

- Company’s indebtedness grew from Rs 89 lakh to Rs 4.89 crore. This could be a concern as it will hit bottomline

- On performance- Do not be fooled by the PAT increase vs. PY. The sole reason for growth in PAT is lower corporate tax rate

- Lacklustre topline growth for the past 3 years. You cannot compare the sales of FY17 and prior to FY18 and beyond because of an accounting reason - the way discounts are treated in P&L. But FY18-20 is disappointment

Now if I combine the above 3 points with the obvious impact of COVID, I feel that the sales and profitability are headed straight down Antarctica for the next 2 quarters atleast. With the tax rate now equalized it will expose them further.

Online shopping during COVID19 and beyond

My main fear with this company is that it is so heavily depended on consumer preferences. If you look at e-commerce, Amazon is selling its own tableware in private label not to mention the dozen other competitors so then how does La Opala gain an advantage for first time buyers who may not know the brand. Any thoughts?

Their B2B segment (hotels, restaurants) is basically gone for this year as people may prefer to eat indoors.

Finally the price is tightly controlled owing to heavy institutional + promoter stake. If one of the institutions dump that might lead to a free fall in price.

My opinion - Wait and watch. I’m bearish on the stock and waiting for price fall following my valuation model.

Cheers

Uzi

6 Likes

WESTBRIDGE CROSSOVER FUND LLC has sold off 23 Lac shares on 11 Aug. They were invested since long but seems they made an exit with loss.

PLUTUS WEALTH MANAGEMENT LLP is the buyer in this deal.

You can find their input/rationale for picking LaOpala below, starting at 1:13:52

2 Likes

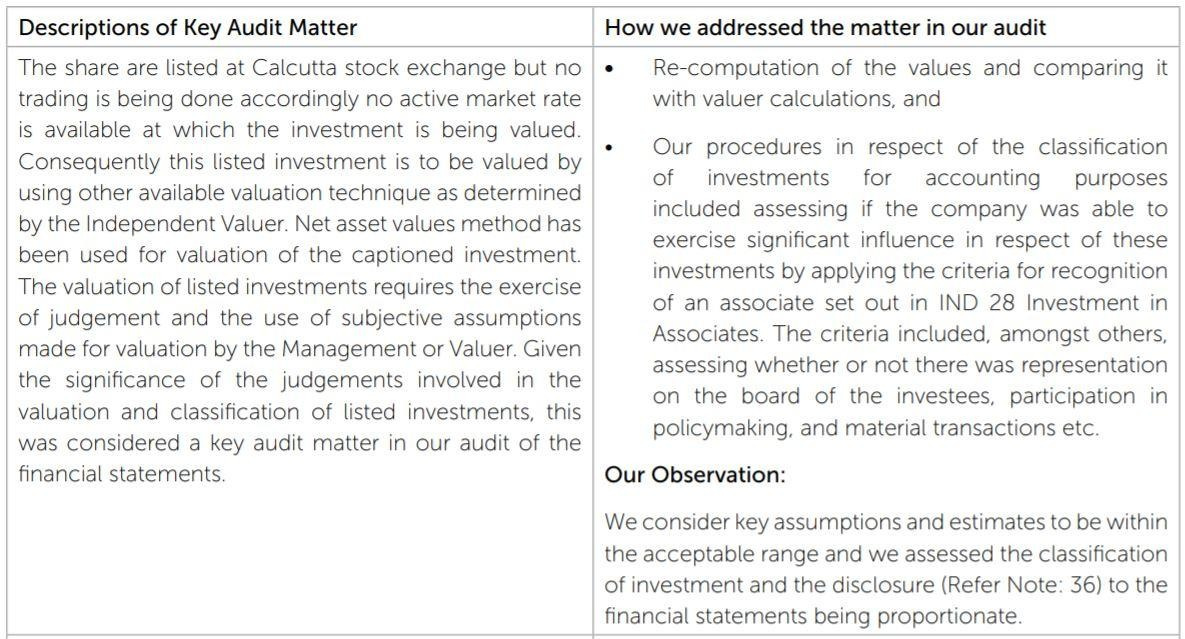

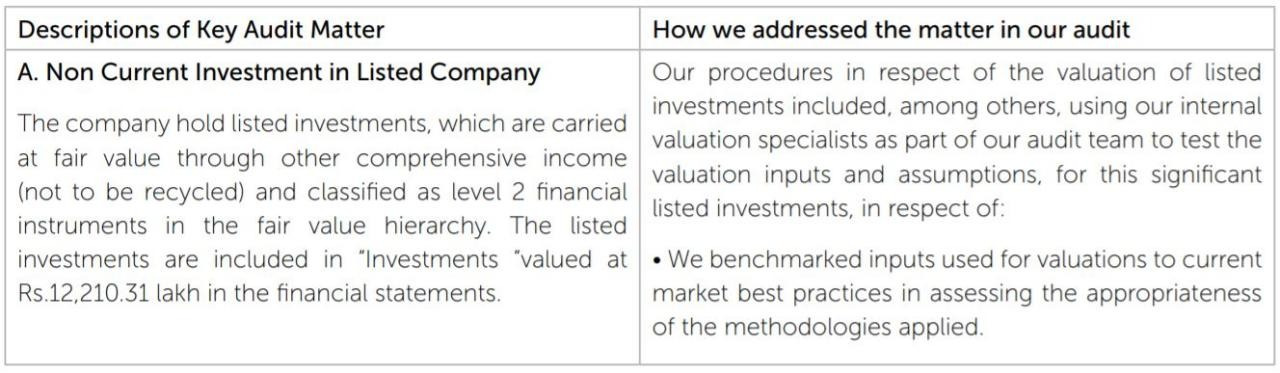

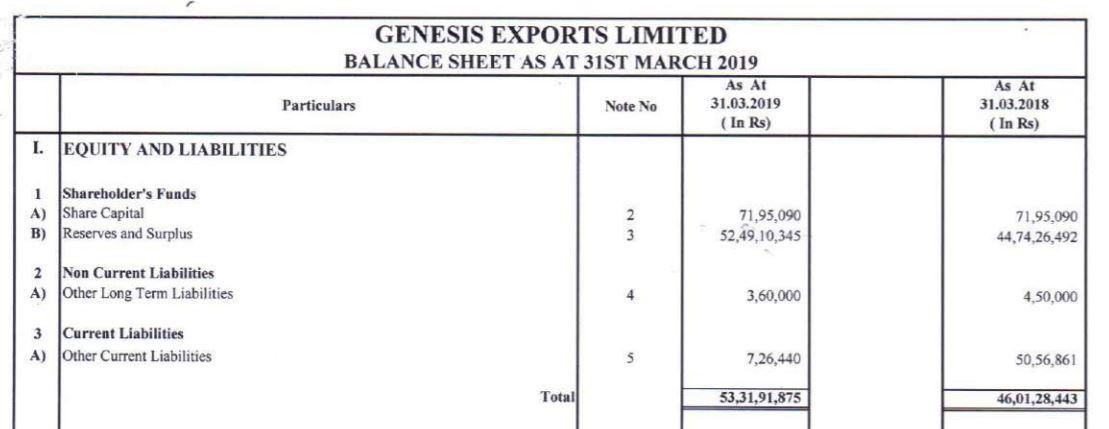

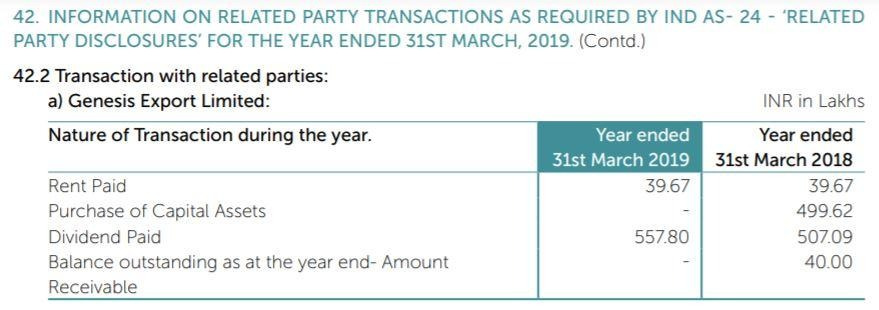

While analyzing La Opala, came across some interesting points. La Opala has a promoter group entity as Genesics Export Ltd. which is a NBFC and listed on Calcutta Exchange, holding around 45% in La Opala.

La Opala also has about 10% holding in Genesics Ltd. They have Non-Current Investments of significant amt. in Genesics Ltd.

While total net worth of Genesics is only 53 cr.

Genesics also involved into Related Party Transactions with La Opala.

What I guess is that promoters have used a way to use shareholders money in name of Non Current Investments to increase promoter shareholding in La Opala and not using their own funds to increase shareholding. Company is able to find a loophole to show shareholding of promoters inflated as they increased their stake in La Opala through Genesics by using funds of shareholders in name of non current investment and did not use their own funds to increase stake. Instead of paving way of increasing shareholding of promoter through a separate entity they could have had personal increase in shareholding.

Views Invited …

6 Likes

Good Article on La Opala. Must read…

3 Likes

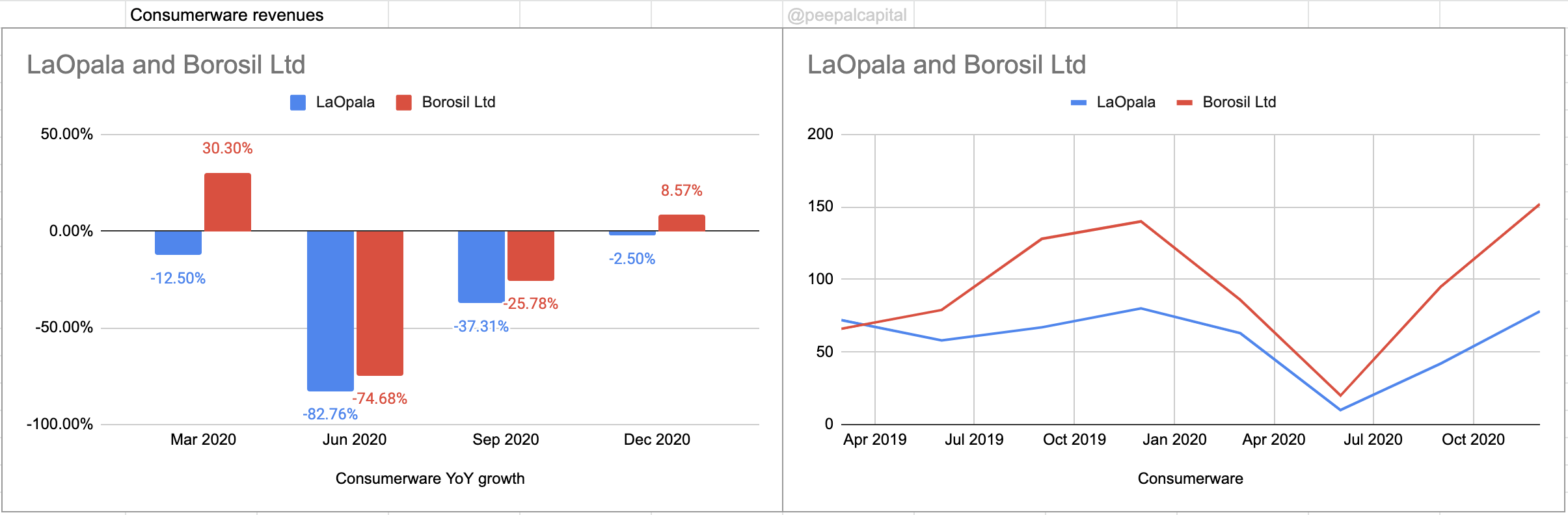

Has anyone analysed how big a threat could Borosil be, reading their annual report, looks ominous in terms of the turnover. Does someone have insights on their margins and ROCE from this category -

Borosil Limited (“Larah”) (Formerly known as Hopewell Tableware Limited)

The Company participates in the fast growing 500 crores opalware market through its brand Larah.* *The modern homemaker is looking for elegantly designed and fashionable products that can be used frequently (daily use) without fear of* *damage. Larah offers a light, strong and chip resistant product range that caters to this consumer need. Additionally, the products are boneash free, making them vegetarian friendly. Made up of toughened glass for extra strength, it’s extremely light weight and with a whiteness that* *doesn’t fade. Larah’s television commercial highlighting the break-resistant property of the product was well received.* *During FY19, Larah achieved a turnover of 146.9 crores, a growth of 43.9% over its sales of 102.1 crores (including excise duty) in FY18* *(Growth in revenue before excise duty was 46.9%).The company invested about 64 crores in capital expenditure towards adding capacity

as well as upgrading the production lines to produce ‘best-in-class’ opalware in a range of shapes and sizes. With this the company has the

capacity to service demand of up to ` 200 crores.

2 Likes

Apart from this segment Borosil have ventured into kitchen appliances. This particular section is going to huge gainly due to ‘Aatmanirbhar bharat’ . Their online sales are growing rapidly. They are into packaging pharma as well which is gaining high tailwinds due to growth in pharma. In my view Borosil is a much much better bet than La opala. Management is too conservative. This year’s annual report highlights how big the opportunity is for Borosil.

Disc : Invested in Borosil at 148 recently. Will hold for long.

2 Likes

Borosil entered the market in 2018, and based on my discussion with industry guys, the quality of La opala is Class apart. Difficult to compete with La opala on Quality parameter according to them.

There are premium section also yes but LaOpala having better quality… Also borosil having diversified business

1 Like