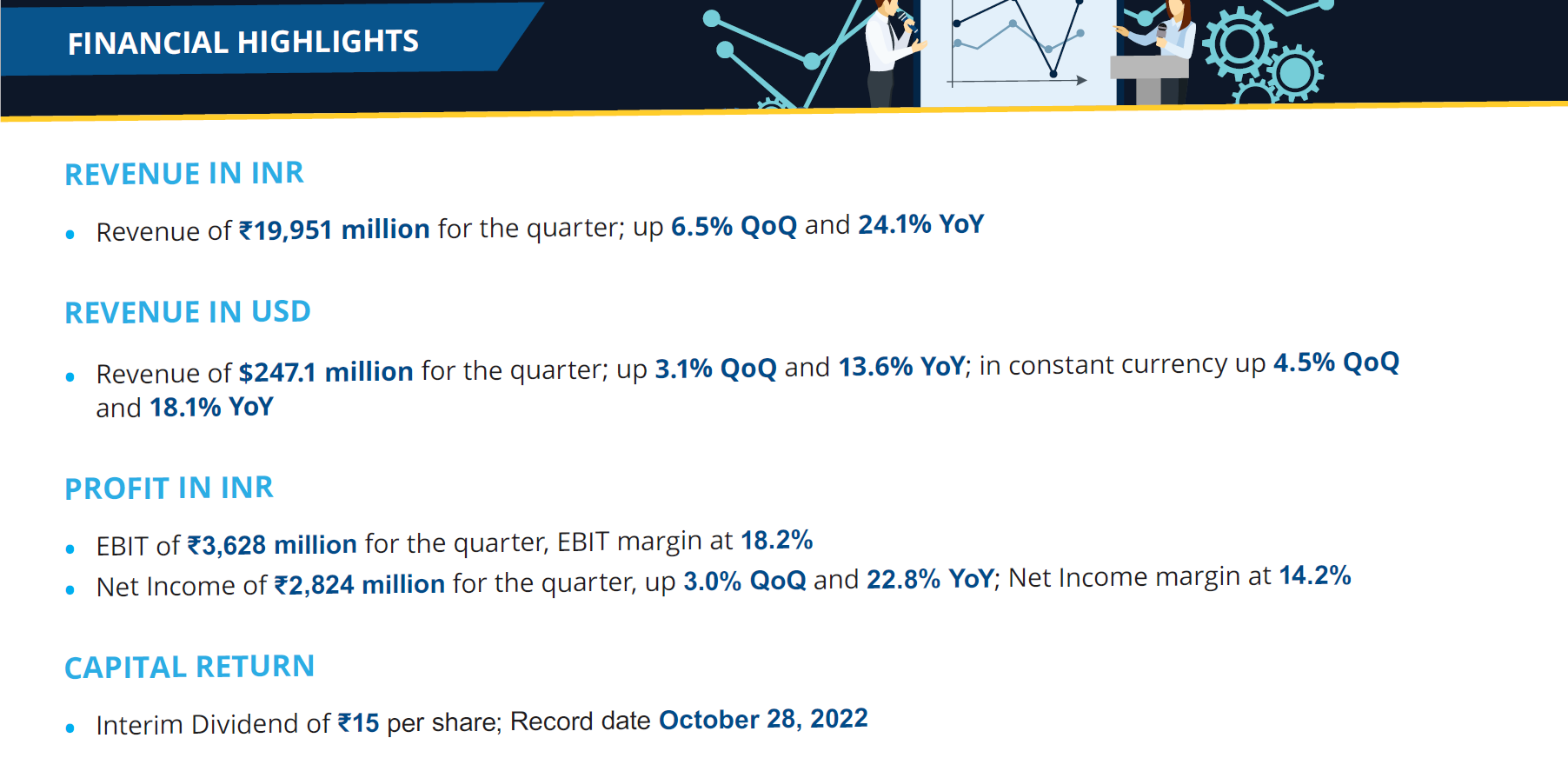

FY23 - Q2 - Result looks good.

4 Likes

2 Likes

Acquisition update

January 12, 2022: L&T Technology Services Limited (BSE: 540115, NSE: LTTS), a global leading pure-play engineering services company, today announced that it has agreed to acquire the Smart World & Communication (SWC) Business of L&T, enabling LTTS to combine synergies and take offerings in Next-Gen Communications, Sustainable Spaces and Cybersecurity to the global market.

1 Like

Concall Summary

2 Likes

If true, it doesn’t reflect well at all on the company. And this settlement could have 7-8% impact on FY23 PAT (per analysts).

Nothing alarming other than the impact on FY23 PAT. Ask anyone working in IT and they will tell you that all IT companies do the same trick. Most of the time people travel on B1/B2 for the purpose of Training, Knowledge transfer but they work from there after those “Trainings” :). If you look back, you will find many such news of Infy, TCS etc setting such visa abuses.

3 Likes

Company has confirmed that this amount has been accounted for in the previous quarters itself and wont have any adverse impact on Q4FY23 and FY23 results.

2 Likes

These 2 companies result confirm that ER&D space companies are able to buck trend compared to pure IT services companies

3 Likes

Company is doing 20% growth every quarter since last 7-8 quarters, will do 20%+ USD in FY24 as well, FY25 they will hit 1.5B. In tough macro conditions if they can deliver growth, wonder what can happen if the skies get clear someday ![]()

Reverse DCF bakes in 10-12% growth with terminal multiple of 15. This has all the characteristics of a compounder business which can grow 18-20% CAGR in next 5 years, but still available at 30-35 PE.

Disc: Invested

17 Likes

LTTS is a well diversified play. One can take a basket approach and include LTTS along with some high beta names in this sub segment of tech plays.

2 Likes

Its definitely a large deal for LTTS and shows that SWC capabilities have started bearing fruits in cybersecurity. However, the key thing to watch out will be how they are able to leverage these kind of big wins to take the offerings to their global clients. Legacy SWC always had government contracts in India and that was one of the main reasons for their low margins and higher DSO days.

There is a huge demand in smart cities and cybersecurity globally in developed countries. Amit Chaddha (LTTS CEO) recently wrote in an article how smart cities and software defined vehicles can be integrated. If leveraged well, such deals can be big revenue triggers for future pipeline.

Disc - Invested from lower levels.

3 Likes

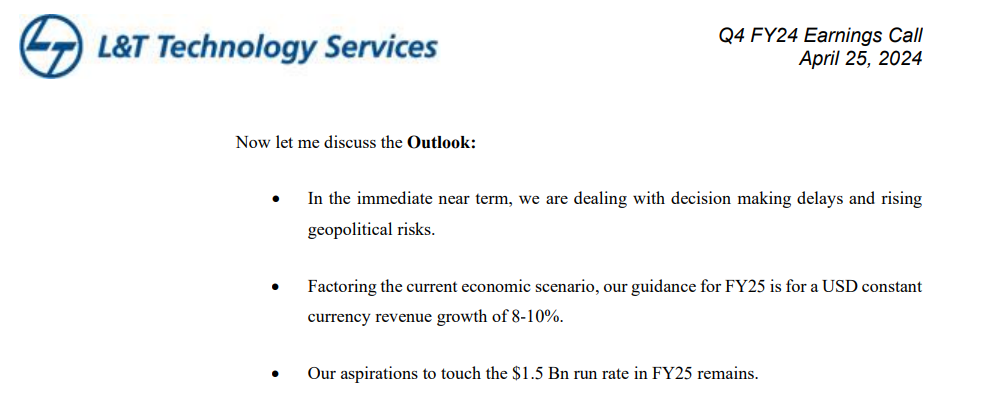

Based On above Outlook by Management , On one hand they are guiding for 8-10% CC growth for fy 25 on the other hand they have aspirations to touch 1.5 billion usd in reveue that a 50% increase from present sales. How are they going to achieve it if they are guiding for 8-10% CC growth.

2 Likes

Maybe through acquisitions

You have only highlighted certain part of concall. If you are following the company, they have always maintained that their 1.5 B USD aspiration has inorganic growth backed in as well. Recently they absorbed around 300 engineers from Forvia as part of a 45M Euro deal. Now they are not looking for any auto related acquisitions in Europe. The target is medtech in US now. Yes 1.5B USD is ambitious but not completely ruled out. Problem with LTTS off late is they are taking two steps forward and one step backward. They were doing well on margin and revenue front before they acquired SWC. They had to compromise on margin due to that. Now due to reorganizing in three verticals, they are again compromising on margin and you will see EBIT margin mostly going below 16% in first two quarters of FY25. So they have compromised on margins for growth in last two years which market has not taken kindly. In fact, in Q4FY24 they did growth 5.1 QoQ in CC which is really good but margin guidance did not go well with market and stock has been on downturn since then.

10 Likes

Summary of L&T Technology Services Q1 FY25 Earnings Call

Key Highlights:

- Revenue grew 6% YoY (Year over Year) but declined 3% QoQ (Quarter over Quarter) due to SWC seasonality.

- Large deal wins were strong, with two $30 million deals, two $15 million deals, and three deals with a total contract value (TCV) of $10 million.

- The company is investing in Sales and Technology under its “Go Deeper to Scale” strategy to prioritize growth.

- They expect their revenue and margins to improve from this quarter onwards.

Segment Performance:

- Mobility: Strongest growth in the last 6 quarters (6%+), driven by Auto, followed by Commercial Vehicles and Aero. Won 3 large deals in Mobility. Focus on EV, Hybridization, Vehicle Engineering, and Software Defined Vehicles (SDV).

- Sustainability: Slight YoY growth due to strong performance in Plant Engineering, offset by a decline in Industrial Products. The decline is temporary due to supply chain issues and large deal delays. They are investing in asset management solutions and see this as the next growth engine.

- Hi-Tech: Good growth in Semiconductors, with strong demand for AI chip design. Medical sub-segment is seeing spending on Sustenance engineering, QARA, Value analysis and Value engineering, Digital manufacturing solutions for operational excellence. They are seeing multiple large deals in play across Telecom, Semcon, ISV, and MedTech.

Outlook:

- The company is comfortable with its guidance of 8-10% revenue growth.

- They see growth in all three quarters ahead and expect H2 to be better than H1.

- Their aspiration of $1.5 billion in revenue by FY25 remains unchanged.

- They will host an Investor and Analyst Day on August 27th in Bangalore.

Other Points:

- The company filed 47 patents in Q1 and has a cumulative total of 1,343.

- They are ranked as a Leader in the Everest Connected Product Services assessment.

- EBIT margin for the quarter was 15.6%, in line with the aspiration of 16% for FY25.

- The company expects the EBIT margin trajectory in H2 to be better than H1.

- They are actively recruiting freshers and laterals, but automation is reducing the straight-line impact of headcount on revenue.

- Wage hikes for the year are expected to be finalized in the next week or so and will be effective from October.

Key Points:

- L&T Technology Services (LTTS) is targeting an 8%-10% organic revenue growth for FY25.

- The company is also aiming to achieve a $1.5 billion revenue run rate by the end of FY25, which may include inorganic growth through mergers and acquisitions (M&A).

- LTTS has a strong pipeline of deals, with a significant portion being proactive deals initiated by the company.

- The company is focusing on M&A in three key areas: Automotive in Europe, ISV & Hyperscalers in North America, and Medical in North America.

- LTTS expects its revenue to grow every quarter for the rest of FY25, with a stronger H2 compared to H1.

- The company is confident in its growth prospects despite potential macro headwinds.

Other Call Highlights:

- LTTS is seeing increased customer interest in cost reduction, cash conservation, and faster time-to-market solutions.

- The company is investing in Artificial Intelligence (AI) and is incorporating it into many of its bids.

- LTTS plans to be more transparent by issuing press releases on new wins and partnerships.

- The recent large deals won by LTTS are ramping up at different paces depending on the specific customer situation.

Inorganic Growth:

- LTTS confirms that M&A is part of their strategy to achieve the $1.5 billion revenue target.

- The company is looking for targets in the range of $50 million to $150 million with the right margins and valuations.

Overall, the call portrayed a positive outlook for LTTS with strong growth prospects and a clear M&A strategy. L&T Technology Services is focused on growth and is making investments to achieve its goals. They are confident that their revenue and margins will improve in the coming quarters.

Follow me on X for many other company updates: x.com

7 Likes

Altair and L&T Technology Services have joined forces to establish a digital twin center of excellence, aiming to deliver advanced digital twin capabilities to joint customers across mobility, hi-tech, and sustainability segments. This strategic partnership is set to revolutionize the digital twin technology landscape.