L&T Finance Holdings, once wanted to become a bank. It was so focused on that one goal that made it de-focused on the niche NBFC space. It was Jack of all master of none and same was evident from its ROE, growth and other metrics. When RBI made it clear that L&T may never get a chance to become a bank, it was the first to act and swiftest of them. Instead of disappointment and gloom, started focus and bloom. Focus on ROE, growth and specific areas of business -

- Rural Finance

- Housing

- Wholesale

(They even have a growing AMC business which they once wanted to sell but are holding it and it is doing quite well)

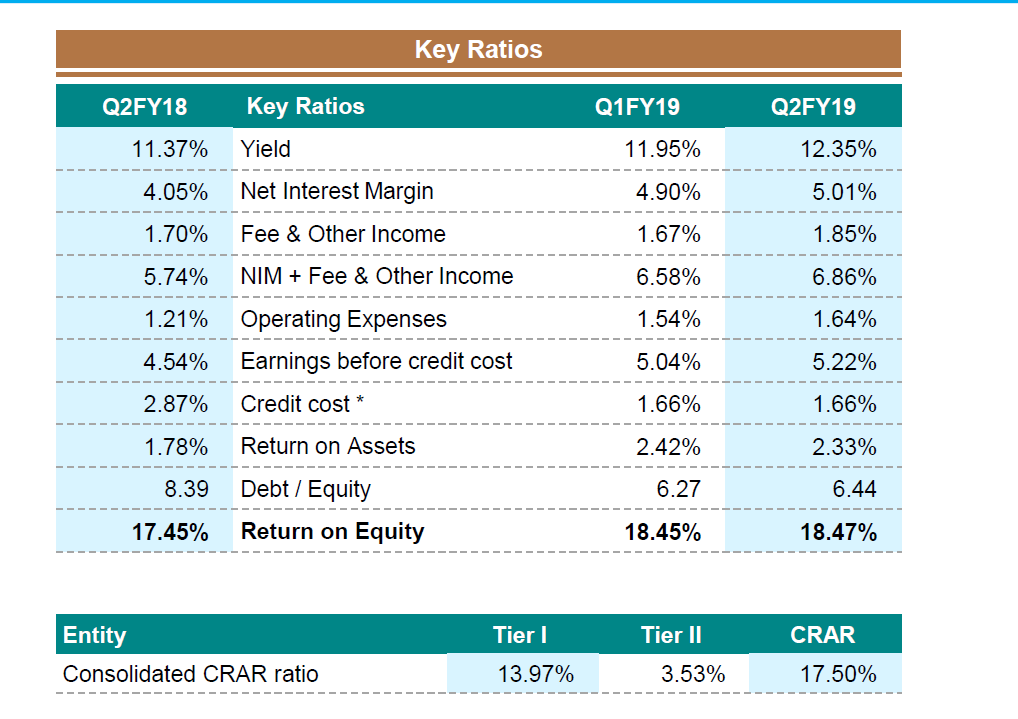

A target to achieve 19 ROE by 2020. All this happened around couple of years back. ROE is already doubled since then to around 17 plus. They will surpass 19 and be close to 20 or 20 plus by 2020. NPAs have reduced ever since. Growth in focused business is industry leading. Target is to further reduce contribution of Wholesale in the overall mix and increase retail parts.

Frankly, I track quite a few blue chip and mid caps from good business houses…I have never seen such a dynamic and aggressive management and specially the ones who walk the talk and are so focused on first writing their goals and second achieving them.

History may not be with them but I feel that future may be. In this era of NBFC and shift from PSU to Private, this one stock is not worth ignoring. If in 2 years they can do so much change to themselves, I am sure they can achieve any targets they set for themselves and they must be tracked by serious investors.

At around 2 time P/B, if management keeps walking the talk for next 2-4 years, this may turn out to be a dark horse in NBFC space.

I welcome all seniors and co investors for their comments

Stock Analysis: The share is trading at P/B of less than 2.5, ROE is 17 plus, P/E do not matter to me when I analyze a financial company (I may be wrong). 64% is promoter shareholding. Significant individual public Investor is Harsh Mariwala Family. Growth for last 1 year has been 30% plus QoQ in Profits. Loan book is growing 30% plus as well. NPA is very healthy and improving with good risk management.

- Wholsesale: This business includes Corporate loans. This is mostly legacy but not defocused. Management target is to reduce it in the overall mix but still focus on this business

- Housing: Relatively new entrant. Loan growth is more from developer loans than retail at the moment. But same is even for some darlings like PNB Housing. They have edge on understanding the developer by virtue of their parent who have either been their contractors in some form or other or supplier. Decades of experience of parent in EPC space provides an edge and risk management in terms of to whom they give money and how much.

- Rural Finance: Highest growth area for the company since last couple of years. Better than some microfinance darlings when it comes to risk management/NPAs and growth combination.

- AMC business: Although not prime focus at the moment. Initially wanted to sell it but did not get good valuation. It was a boon in disguise I feel as AMC is growing and with time this part of business will fetch better valuations when sold, if sold.

Risks:

- It is not a bank, it is NBFC: NBFC by its inherent nature is a very very risky business.

- Interest rate fluctuations, Bond Yields etc will impact cost of funds. But same is for every NBFC. It is how well they manage the risk and this year they have been doing well in challenging times of bond yields for NBFCs

- Aggression can be a friend and foe. The management is very aggressive. I hope they are intelligent over long term otherwise it may result in back fire in terms of NPAs.

- Housing growth is more developer loans. Risk of NPA in future

- Wholesale book is still 50% plus. Risk of NPAs in future

- Rural Finance/Micro Finance is a very risky business. Government policies is a major risk.

- Any new buyouts (as earlier few years back they were targeting Insurance space) valuations,

- Not being a bank is in itself a big risk for long term shareholders and so is a feeling of need to be a bank if it crops up to any NBFC management. Same, is true for any NBFC. Look what happened to Capital First’s long term shareholders in its quest to become a bank.

- Need of capital by parent L&T? Not sure about this one.

Investment Rationale: All provided above, plus the risks above are opportunities to get it at 2 times P/B. If we believe in the Management ethics, integrity, intelligence and aggression, then these risks are opportunities. At least last 1.5 years they have walked the talk. Whenever they speak, they speak of shareholder value. Never heard a management so directly speaking of increasing shareholder value. (It could be pressure from L&T parent who want to increase their overall mix of profits from services business. So, it could be a gesture by management to please L&T as the highest shareholder). Whatever be the case, as long as they talk good and walk the talk with integrity and intelligence, we have a winner.

Disclosure: Invested. This is not recommendation. A healthy discussion on fundamentals only