L.T. Elevators Limited

Sector: Industrial Manufacturing (Elevators)

Exchange: BSE SME

Basic Details

• Market Cap: ₹ 416 crores [As on 28.12.2025]

• Issue Price: ₹ 78 [16.09.2025]

• Current Price: ₹217 [28.12.2025]

• Listing Date: 19.09.2025

Promoters holding is almost 63%.

Invicta Continuum Fund [AIF] is holding around 6% of shares.

Financial Highlights

The company works through two entities. Parent LT is in lift and elevators, whereas 100% subsidiary Park Smart Solutions limited is in Mechanical car parking system. The consolidated result includes subsidiary financials w.e.f. Q4, 2024-25.

Financials- standalone

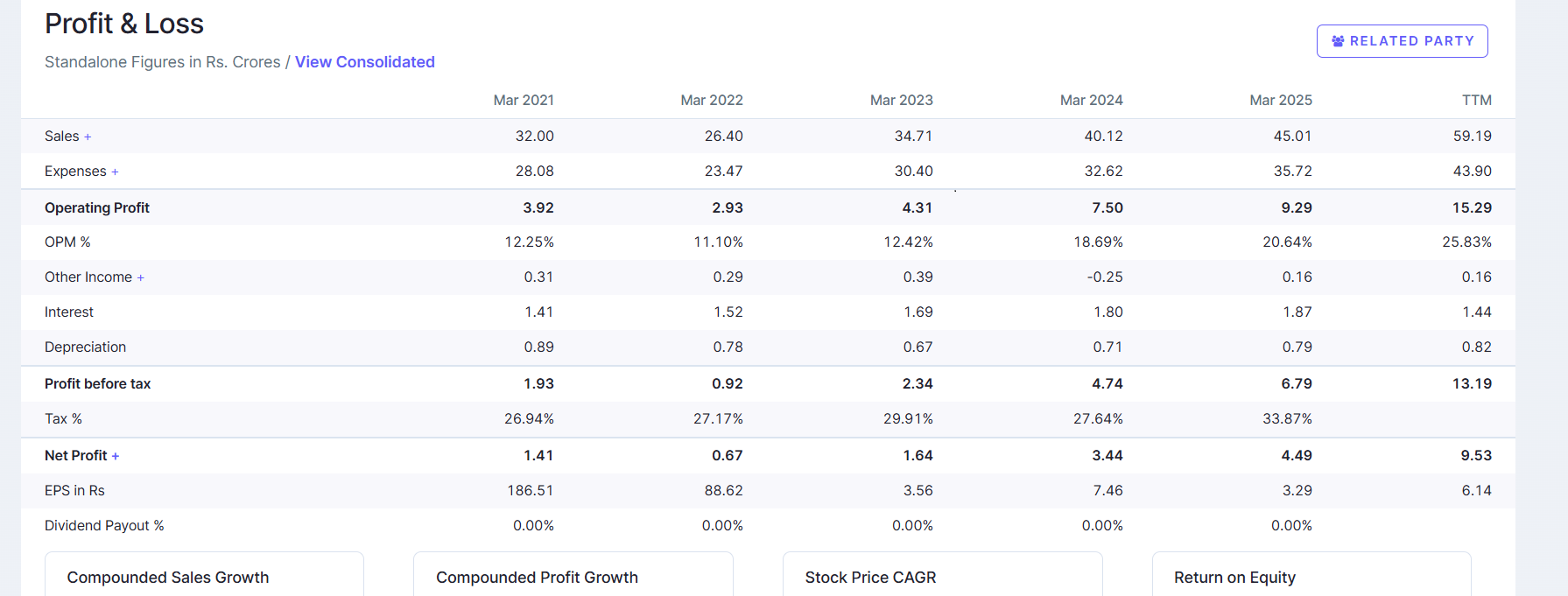

The company’s topline (standalone) is growing at a steady pace, almost @20%. Margin is going up due to better capacity utilization, and due to increasing share of service revenue. The parent company had 62% capacity utilization in FY 2025, which may go up to almost 80% in current financial year.

Standalone numbers of Park solutions was 10.3 Cr revenue & 82 Lakhs PAT in H1’FY25. In H1 2025-26, they have done almost 16 crores topline with 3 crores PBT. The subsidiary was working on 71% capacity in FY 2025, with almost 50% growth they shall be working on 100% capacity in FY 2026. The company has informed that the subsidiary has brought industrial land nearby, it appears that they have expansion plan for the subsidiary.

The contribution of subsidiary is likely to grow in the company. The consolidated order book of the company stood at 22 Crs as of Aug 2025, with the parent company accounting for 11.4 Crs and the subsidiary contributing 10.7 Crs.

Current Year estimate:

From these information, I estimate (pure guesswork) for FY 2025-26 a consolidated topline of almost 105 crores [70 crores for parent and 35 crores for subsidiary] with PAT of almost 16 crores if present margin can be sustained in H2- 2025-26.

Business Overview

L.T. Elevator is by far one of the elevator manufacturers across the nation. With well-established assembly lines, the company has an integrated production line with the help of hi-tech German technology. They are India’s only indigenous elevator company with latest modern German machinery and hi-tech infrastructure. They claim to optimize and customize operations for maximum efficiency, immense product quality, improved customer experience, reduced risks and lower capital expenditure. They have an in-house design team of 25+ engineers for mechanical, electrical, embedded systems and robotics. L.T. Elevator manufactures following products at its manufacturing plant: Modern Escalators, High-Speed Apartment Lifts, Bungalow Lifts. Hospital lifts, Goods lift. Specialty Elevators. Mechanical Car Parking System is being manufactured by their 100% subsidiary.

They have 20 branch offices in India with a trained maintenance team of around 250 persons. They claim to provide in-person maintenance support within 60 minutes for breakdowns. They have over 8,000 installations under service contract including elevators, escalators and car parking.

Elevators (Parent): Installed 800 units p.a.; utilization: 62% utilisation in FY25 vs 49% in FY24. b) Parking Systems (Subsidiary): Installed 1600 units p.a.; with a 71% utilisation in FY25.

The company is concentrated in east India. They have a mix of clients consisting of public sector clients (including Railways), private corporates, real estate developers, and standalone projects, largely on a made-to-order basis.

Management Quality

Nothing is known much about the management. However, in my view a person who can create a business of almost 400 crores market cap from scratch has some management acumen.

The promoter is a long term investor in some decent listed companies like Chennai Ferrous, Gita Renewables, Roto Pumps. Roto Pump holding is significant.

Investment Thesis

- It is the only pure play elevator company in listed space.

- Elevator business has decent maintenance and spare business. The company claims 8000 installations, which is likely to grow in course of time.

- The company has expansions plans, and looks like that the company’s products are well accepted in the market.

- Home elevator space is growing at a decent pace. The company has recently reported successful delivery of 3 state-of-the-art single phase home elevators at a prestigious duplex project in Kolkata, marking our strong entry into the ~₹2000 Cr niche B2C home elevator market that is ripe for disruption with innovative, elegant, and aesthetic solutions.

- The company expects India’s elevator and parking markets growing at 15-20% CAGR through 2030. Parking market growth can be higher. Sharing the press release of the company.

LT press release 11.11.2025 UPLOAD.pdf (111.4 KB)

Concerns:

- Investing is micro-cap companies are risky, one can lose 100% of the capital.

- There are some red flags in the balance sheet like some disputes with tax departments, non payment of some money to governments, MSMEs etc.

- Promoter directors salary appears to be on higher side.

- Inventory/receivables appears on higher side. Cash flow from operating activity is negative.

Valuation

The company has equity base of 19 crores, and at present market price [Rs. 217], the company is valued at almost 416 crores. Based on current year’s earning estimates, it is trading at 26 times earning. Not cheap.

Growth Catalysts

-The elevator market is growing at 15-20% CAGR as per the management view.

-Parking subsidiary shall be working at almost 100% capacity in the current financials. They have already taken land for the subsidiary and I guess that they will start another unit next year.

-Though it may not be possible to them to compete against Otis/Kone, in home elevator market they can do well which is growing at a decent pace.

-Presently their spares and service business is around 7% which is likely to grow going forward in future.

Red Flags to Watch

There are some red flags in the balance sheet like some disputes with tax departments, non payment of some money to governments, MSMEs etc. Promoter directors salary appears to be on higher side.

Disclosures:

Invested. No relationship with promoter/company.

Disclaimer

SME stocks carry higher risks due to their smaller size, limited operating history, and relaxed regulatory requirements. This analysis is for educational purposes only and should not be considered as investment advice. Always conduct your own research or consult with sebi registered financial advisors before making investment decisions.