Yes, definitely no point considering ourself as part holders of the business unless the controlling management treats us that way. Regarding management integrity generally it is black or white. I try to stick only with the most transparent ones. Sometimes this could be unproven management or us ignoring certain flags which lands us in trouble. I have to say the red flags were obvious in this stock when I read this thread which I chose to ignore that landed me in trouble this time.

True. Sometimes we become victims of affective forecasting. We refuse to see the writing on the wall and hope that the business chiefs will mend their ways. But, it seldom happens.

I think an approach worth considering is to eliminate subjectivity in management assessment. Our examination of management is influenced by our biases. A charming, dynamic business leader may be misinterpreted as a good businessman. Big difference between the two.

Let me connect the dots:

Sidhant Gupta (Along with associates: Sidhant Gupta HUF, Pasupati Dairies, Sonika Gupta) use to hold 10-12% stake in Kwality. HSBC used to have 3% stake at the end of Jun-17. As HSBC wanted to sell stake, they were not able to arrange a buyer for the block they owned and hence started selling in the market.

The stock crashed on 4th & 5th of Sep. Sidhant Gupta (may be forced by the management) pledged its shares and with the money started buying the stock (being sold by HSBC) from the market. Come Dec-17 SH pattern, HSBC didn’t held any stake

Question is why Sidhant Gupta and not the management bought the stock? Management has no limit to buy as most of his holding is pledged to provide working capital for the company.

Fast forward to March: Sidhant Gupta (alongwith Associates) has most of his holdings pledged with different brokers. For whatever reasons, F6 sold 1cr shares of Sidhant Gupta without his knowledge (as per the company filing). Since most of the shares are pledged this calls for a MTM margin. As Sidhant Gupta has no money left (or no shares to pledge) brokers/financiers are expected to sell his stake to recover the MTM. In last few days whatever bulk deal we have seen is most likely because of the MTM margins (but who knows there are more cockroaches in the kitchen) and SG has been forced to sell the shares to cover up the margin.

This is purely a hypothetical theory. However, if we closely look at the insider filings from BSE, details coincides with the hypothetical theory i have shared.

File Attached Kwality - SG Pledging.xlsx (52.0 KB)

Coming to the Business

It is the largest private dairy in India with capacity of ~4.3LLPD. Company has been transforming itself from B2B to B2C business. It procures 3.4llpd of milk directly. Operational numbers do look good. However, devil lies in the Balance Sheet. Company has 1620crs of debt with effective interest rate of 12.5%. This bring interest cost to 203crs. Including the floating working capital loan, interest cost for the year comes to ~220crs which is a big dent on OCF. Company still generates OCF of ~200crs (FY17) as per the filing. This can go down this year, as last year Interest cost was around 183crs.

Questions that one needs to ask:

- Is the company worth 3,000crs (1400cr market cap+1600cr debt)? I believe asset is worth more than this but not all stories can be bought looking at the asset value.

- if yes, are you comfortable to hold it given the management quality isnt good?

- What if the company cant improve the balance sheet over next couple of quarters, as management indicated they are finalising the capital restructuring?

- If by any chance management decides to retire the debt by Equity dilution, it would dilute the equity significantly. If the equity is offered (assuming they retire 500crs of debt) between Rs 55-70, dilution would be anywhere between 30-40%.

6 Likes

In the previous con call mgmt said that the max dilution would be 15%. Even at 120 odd price they didn’t feel the valuation was correct hemce were delaying the fund raise. With price now at 50-60, cant see them going for this now unless they decide to dilute more as you say above.

I don’t want to guess at what price they would dilute. If they don’t. then its going to affect them badly coz they have to bring down the interest cost significantly. Now that’s for the management to decide.

I would watch how the event unfolds.

agreed @kunal_patel its between the devil and the deep sea for Kwality. If they delay the funds raise, the balance sheet remains under pressure and market will be unrewarding. If they raise the funds and clear some of their high cost debts, they end up diluting more than expected.

From a business standpoint, I think the key monitor able is how the B2C business is able to grow. In the past (FY17) it grew in excess of 30-32%, then it slowed down in Q1-Q2 FY18 due to GST and demon issues, then has started to pick up again from Q3 (23% YoY). If this continues and they are able to maintain a growth of avg 20% for the next few years, then the transformation of the business including the balance sheet, cash flows and P&L will happen.

Disc: I am invested in Kwality so have a positive bias.

the major risk for Kwality more than the management quality is the debt.

In my opinion if the insiders want to sell shares, they would sell in small quantities minimizing sharp falls like seen in recent times. The sharp falls seems like a result of pledges unwindng.

Coming to the debt. the company interest cost in the December quarter increased 10% qoq indicating at 10% increase in debt. Further increase in debt can lead to share price drops. there is some seasonality in cash flows, So a weak FY18 OCF could also be leading to increase in debt.

for the three years from FY15-FY17 Kwality cash flows was in line with its net profits. this was the major concern for Kwality before that its cash flows were always negative

Overall Kwality looks like a high risk high return play.

The promoters’ stake has fallen by ~ 9.2% between Jan and March 18 (as per BSE filings). It raises some serious concerns.

Regards

Sj

1 Like

Im quite certain this is a result of the lender dumping promoter-mortgaged shares in the open market.

Yes, that seems like the most logical reason. Also, given the fall in April, it is reasonable to believe that their current stake should be lower.

Disc: Recently exited

Regards

SJ

HI everyone, please share your thoughts on the stock now as it has taken serious price drop.

Additionally share your perspective of a fresh investment at current prices caped at INR10000

Will it be worthy high risk high return bet

From Q3 FY18 concall there are few points that were not answered by management/ discrepancies in management answers.

- Even if debt is constant for last 2 years, why interest cost is increasing.

- This year again operating cash flows as per annual result is only 56 crore. In Q3 concall management told that OCF till H1 was 160 crore. As per annual result, there is increase of 320 crore in trade receivables. However management is saying that this is initial phase of value product launch and in initial phase you have to provide lot of credit to distributors.

- In Q3 concall management was telling that their credit rating has improved and they expected 1% decline in interest rate on outstanding loans. As per brickworks rating in june -18, credit rating on outstanding loan has been actually downgraded.

I am not clear is there any difference between company’s credit rating and credit rating on outstanding loans.

- In concall management is saying their debtors day are reducing, but their trade receivable increase this year from 1500 crores to 1800 crores.

My one more concern is

already promoter holding has come down to 51%, almost all of which is pledged.

What will happen if selling of pledged shares continue. Will promoter loose operational control of company ???

Members views are invited.

Disc: Invested at avg. price of 30-32

The business seems to be moving in the right direction based on the numbers and the conference call transcripts.

However, to me one of the keys is to get a handle on whether the 1800 Cr receivables is good or whether they will need to provision for it.

The selling of pledged shares will continue unless the management gets a large investor on board or KKR takes control via a board revamp. The valuations are mouth watering for someone like an FMCG major to take over this company. There’s ample opportunity to buy since pledged shares are being sold.

Disclosure: invested

Anyone knows why there was a drop in ~85% during Nov-Dec 2011? Was it a case of stock manipulation?

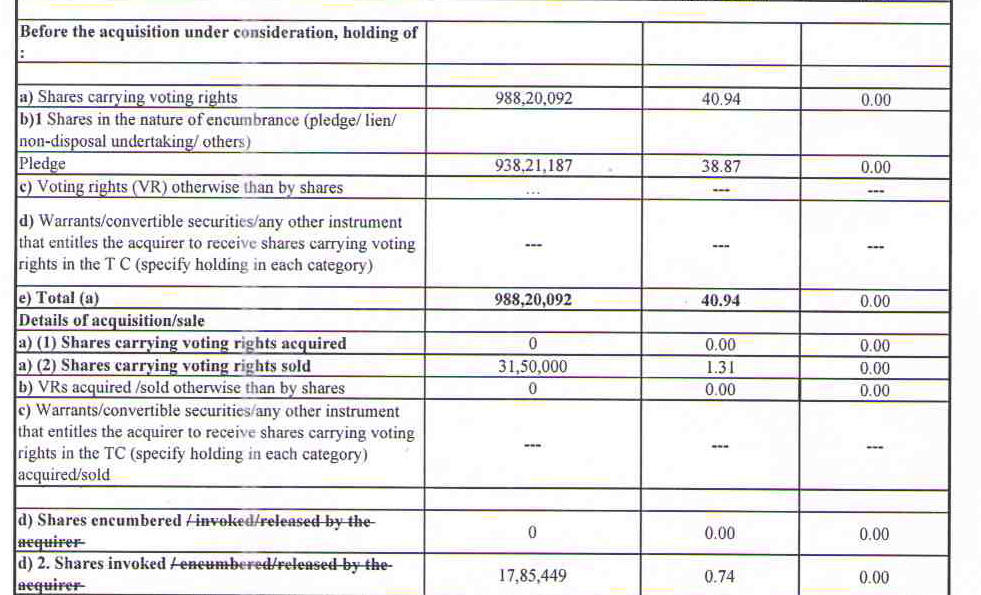

as per latest announcement promoter Sanjay Dhingra also sold 1.31% share holding (31,50,000 shares).

now 38.13% shareholding out of 38.92% shareholding is pledged.

Why dhingra would sell little un pledged share holding that he has. Is he leaving the sinking ship ??

If leaving then why so late, when value of shares is not much ??

does any body have any thoughts??

1 Like

What one can make out of it12198881.pdf (102.3 KB)

That they are making out everything!

2 Likes

The company has declared bankrupcty now!

What exactly happens now?

KKR will get its money after selling the assets and the remaining gets distributed to equity investors’ demat (or linked bank) accounts?

Is there any good resource from where I can learn?

Disclosure:

I’m quite new to Value Investing.

Just merely compared P/E with competitors like Britannia, Nestle and assumed it is a value opportunity and entered at ~55.

You dont get anything in NCLT companies as equity is reduced to 10 percent only.