Hello Hitesh ji,

I am glad that you gave your feedback on my above post. I really admire your investing skills. I can’t agree with you more on the fact that holding on to winners lead to market beating portfolio returns . Peter Lynch’s quote on tendency of fund managers to sell their winners and add to losing position as amounting to "pulling the flowers and watering the weeds” left a great impression upon me.

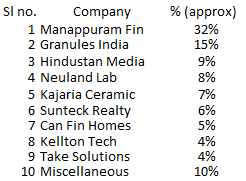

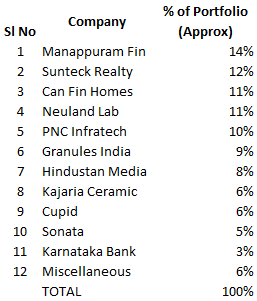

As desired, I am producing below my investment thesis for each of my top bets:

Manappuram Finance:

I bought it last year on sheer valuation aspect. I have observed that market always react in extreme, both in optimism and pessimism. Valuation accorded to Manappuram or for that matter Muthoot reflected extreme pessimism on their business model. At that time , Manappuram had AUM of over Rs.9,000 cr , was available at a MCAP of around 2,000 cr with a P/E of around 6 and Dividend yield of around 8%,. What more to ask for? Management gave a clear road map in the Concalls on their strategy of diversifying into non gold businesses (viz. Micro Finance, Mortgage and Vehicle Finance) & focus on short tenure loans.

I took a leap of faith in their vision and happy to note that so far they have walked the talk. I took further leverage, sold some of Gruh Finance and bought the stock upto 15% of my P.F. at an average price of around Rs.25. I wanted to buy more but had no cash and did not want to sell my other stock or raise more leverage.

I believe further re rerating would depend upon:

a) How efficiently and quickly can they scale up non gold businesses (presently around 11%)

b) How quickly can they reduce over dependence on south (presently around 65%)

c) Their ability to reduce dependence on bank finance.( presently around 72%)

Key things to monitor would be volatility of earnings if gold prices fall, and regulatory changes that may be made by RBI / GOI.

Granules India:

Granules was not my original idea. However, on getting the lead, I studied the stock in detail, developed the following investment thesis and bought the stock last year.

a) Solid track record. It had grown sales in excess of 25% and Profit over 35% in last decade.

b) Dominant share in Paracetamol, Ibuprofen & Metformin etc which are sort of of

evergreen products which would continue to sell in times to come

c) Management had clear Growth Strategy whether acquisition of Auctus,

rationalisation of its portfolio, or CRAMS JV with Omnichem etc

d) Real catalyst would be impact on margins due to higher proportion of sales of Formulation.

e) Being a B2B Company, chances of lapses under FDA Audit were expected to be lower.

f) Further successful entry into OTC Market in US can be a game changer.

However, it would need constant monitoring at my end since it has been a Capex led and export oriented growth and any delay in execution of plans may put the rerating thesis on hold. Key Risk being pricing pressure on existing products and negative surprise on FDA Audit.

HMVL:

I bought this recently .Vernacular newspapers are here to stay in India at least for immediate future.

a) Clear leader in Bihar and Jharkhand, gaining Market Share in U.P.

b) Profit CAGR of around 25% over past 3& 5 years.

c) Available at reasonable valuation of single digit PE with FCF yield of around 8-10%.

d) Significant scope of reducing the gap in term of yields with Dainik Jagran in U.P.,

e) State Election in U.P. being near term catalyst.

f) Possible EPS accretive acquisition (not in near term) or buyback/dividend

(may be hope) out of cash of around Rs.650 cr or so in the books which may lead to

re rating of the stock

g) Key monitorables include mode of deployment of cash, newsprint price.

Kajaria Ceramics:

I bought Kajaria around couple of years back. My Investment thesis is produced below:

a) Tiles Industry was growing in double digits due to urbanisation , increasing disposable income etc, lower per capita consumption in India compared to developed countries.

b) Kajaria being leader in the industry, enjoyed some short of moat or atleast brand recollect/ power. Dealers spoke highly about Kajaria. In fact, during renovation of my home (prior to my purchase of stock), I finally had to settle at Kajaria floor tiles for my room.

c) It was gaining share from unorganised segment.

d) Gradual Reduction in debt.

e) Govt ‘s mission of Housing for all by 2022 and Swachh Bharat added tailwind to the sector as a whole.

It has doubled in price since then, valuations are optically expensive, but then whenever the thought of selling it comes in my mind, I start thinking about the story of Asian Paints on the bourses and then hold back

Key Risks: Gas Prices , Time wise correction

Neuland Laboratories :

I wanted to buy a small cap pharma company .I liked the Management’s vision to focus on high margin niche APIs , greater focus on CMS and the probability of operating leverage that would resulting from increase in sales as explained by them in their Concalls. I think opportunity for this Company is huge, whether they are able to scale it up is to be monitored. Some may argue that sales were stagnant for last few years but in investment we have to look forward and see what can change. Key risk remains too much dependence on export (a usual case in Pharma with few exceptions like Alkem etc) and scalability. Management seems to be very candid from what I read in their concall transcripts.

Sunteck Realty

Sunteck is a contra bet for me. I bought it recently partly from the proceeds of Repco Homes. It is a Mumbai focused quality real estate Company with around 24 msf land bank. It basically caters to HNI Clients. Valuations reflect the extreme pessimism towards the sector, which is bound to improve , only question is of time. Current Market Cap of 1400 cr , with reasonable debt. Revenue has been volatile since it followed Project Completion Method of Accounting .

Ability to partner quality PE players ( including Kotak to which it provided an exit at around 22% IRR over a span of 4 Years) speak volumes about the management. Such partnership helps in buying land at cheap prices when ever opportunity presents itself. I was quite impressed with Mr. Kamal Khetan when I heard him in the concall. Mr. Ajay Piramal through trusts/ investment arms also hold around 5% stake in the Company.

BKC residential project may have diluted the ROE but I am looking ahead and feel they will be one of the big beneficiaries once the market improves.

Potential re rating is contingent upon quick monetisation of inventory at BKC and timely execution of Goregaon project.

Key Risks remain delay in recovery of real estate market and single market risk (Mumbai).

Canfin Homes:

Bought recently, Repco proceeds were partly used to buy Canfin. Fastest growing HFC at relatively inexpensive valuation . So, apart from sector tailwind, more of undervaluation play on relative basis.

Kellton Tech:

Wanted to buy a IOT/ Cloud based player due to sector tailwind . Studied 8 k miles, Kellton , Cambridge & Ramco. Could not understand the Cash Flow Statement of 8k miles, Ramco was overvalued, Cambridge used to trade either in Upper Circuit or lower circuit. Kellton was offering higher growth at reasonable valuation, so went for it . I know growth was risky as it was led by acquisitions. Disappointed more by Management’s easy going attitude on TV. I am currently reviewing the position.

(I do hold a minor tracking position in Cambridge.)

Take Solution:

Renewed Focus on Life Science Segment which is witnessing very good growth rates, huge opportunity size and was available at attractive valuation. Company has so far delivered. However, kellton experience is forcing me to review my position here also.