Located in Punjab, Kuantum Papers (known as ABC paper till 2012 until the name was changed) is an agro based paper manufacturer in India and manufactures primarily maplitho, creamwove, copier and specialty paper with a GSM range of 40-200 GSM. It has an operating capacity of 160,000 MTPA.

Client list includes Camlin Kokuyo, Mcgrawhill, S Chand, Navneet Publications among others. Caters primarily to academic segment.

The company’s major area of operations lie within 1,000 kms of the plant (in Punjab) in Northern and Eastern India. 32% revenues from Delhi, 10% Haryana, 7% from J&K, 7% from UP, 7% Punjab. Manufacturing is done based on pre-orders from its 100+ dealer network leading to low working capital days at 37 days.

In 2019, the company had undertaken a backward integration and modernization project involving a capex of 440 cr. The project was focused on cost optimization in generating captive power and in a chemical recovery boiler where the waste material from the pulping process was to be retreated to produce caustic soda which is an input in the pulping process).

Subsequently as the pandemic took hold and use of paper especially related to academia fell off a cliff. Revenues fell 60-70% in H1FY21. Due to the capex plan undertaken in 2019 and the pandemic taking hold, the company faced financial difficulties and entered into a resolution plan with its lenders under “Resolution Plan under RBI’s Framework Covid-19 related Stress” which helped it gain a moratorium on debt payments till Aug 2022 and regularization of some outstanding loans which would otherwise have been classified as default.

Coming to present day, Kuantum paper has recovered smartly from the Covid lows with revenues (Rs 1310 cr in FY23) up 60% from pre-covid levels. Company is operating at close to 100% capacity utilization with plans to increase capacity by 25% in coming fiscal. Increase in FY23 revenues can be attributed to increased volumes (+20% from pre covid levels) and the rest can be attributed to better realizations.

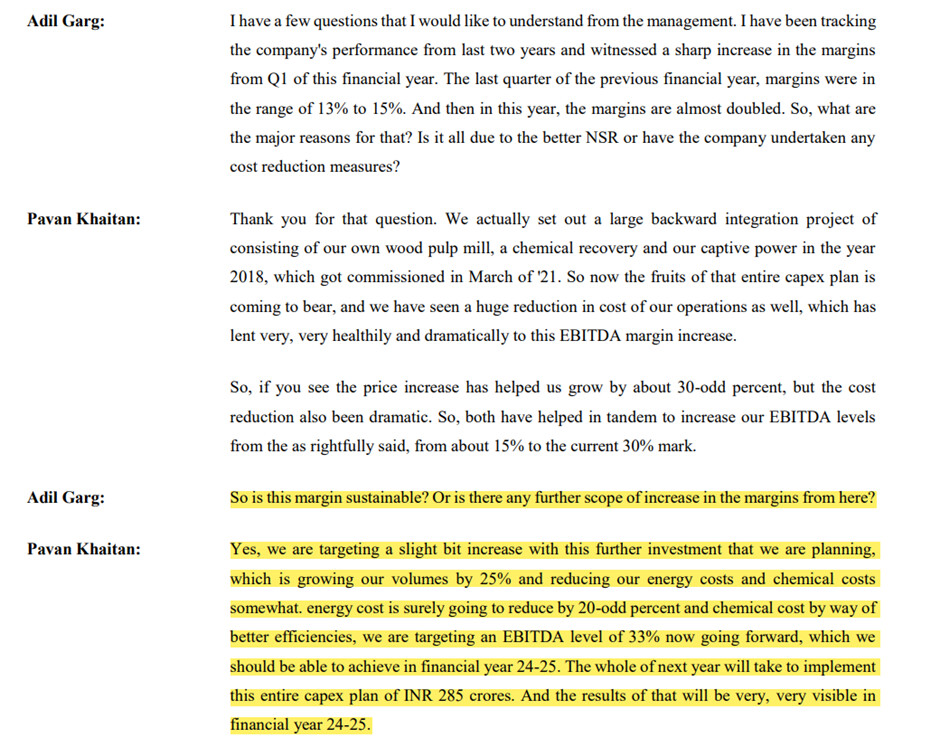

FY23 OPM came in at 29% of revenues for FY23 but has historically varied between 12-21%. Margin increase has been on the back of increased realization. Management seems to be confident of achieving 33% margins (paste screenshot) in FY25 due to certain investments worth Rs 285 cr being made in capacity expansion, a new tissue paper manufacturing plant and captive power generation.

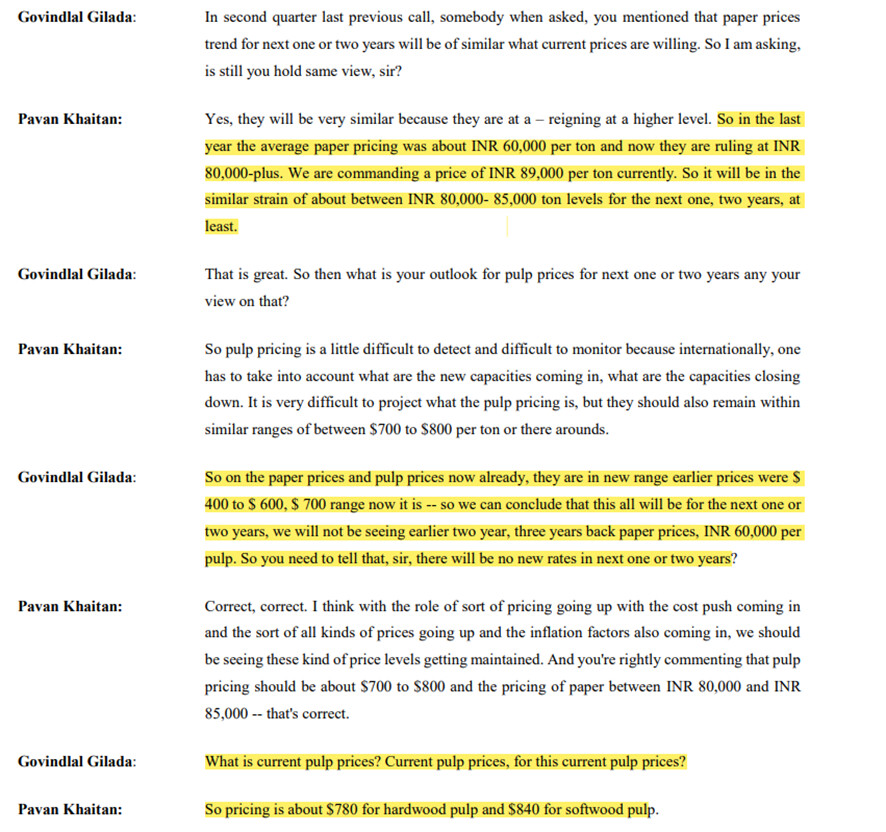

I have my doubts on this guidance as I would expect paper prices to behave in tandem with pulp prices. Wood pulp prices from China had reached a peak of $1200 per ton and have corrected to $800 levels towards end 2022 but the price of paper has not declined in line with pulp prices this time as per management.

Management is confident of achieving the targeted margins even if realizations fall off

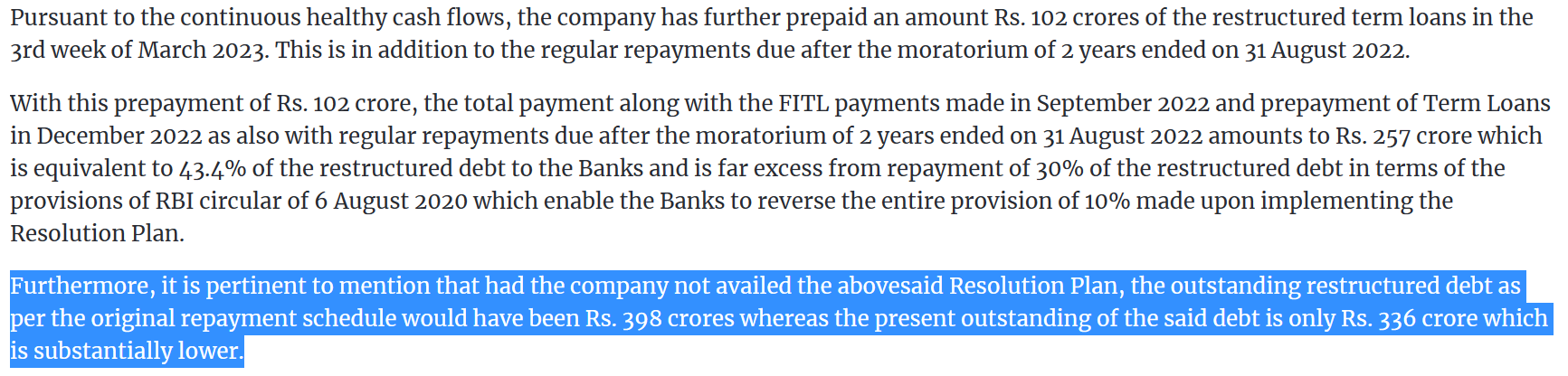

Company has aggressively paid down loans in view of the uptick in financial performance and as on Mar 2023 has debt which is Rs 60 cr lower than what it would have been had the company stuck to the original repayment schedule as agreed with the lenders.

Key Positives

- Strong turnaround post COVID

- Margins have doubled compared to historical average and management is confident of taking it even higher.

- Company is paying down debt aggressively. Any reduction in debt should ultimately show up in book value.

- 100% capacity utilization for the last 4 quarters with plans to ramp up capacity by 25% by FY24.

- Company planning to enter manufacture of food grade wrapping paper which is expected to get a fillip post the ban of single-use plastic

Key Risks

- Cyclical industry with prices fluctuating in line with pulp prices. Although pulp prices have come off by one third in the last one year, they are still 30% above pre-covid levels.

- Price has already run up in line with financial performace and is traidng at 1.4 P/B and 7.5 P/E (after adjusting earnings for exceptional Rs 64 cr non cash item in FY23) which is in line with market leaders like JK Paper, Andhra Paper and at a premium to TNPL

Disclosure: Not invested. Evaluating