Think before posting whether it adds value or not. Irrelevant, one liners, speculative & price comments are of no value & must be avoided.

6 Likes

Most technologies in IT industry follow a life span of incubation, early adoption, slag, late adoption and then becomes a keyword. This happened with Java, .NET, IBM products, integration technologies and SOA. AI/ML won’t be any different I remember 6 years ago cloud was a new buzzword now it’s a common term these trends can be viewed in stackoverflow statistics

Irony is stackoveflow itself is going through disruption due to ChatGPT

Now coming to the annual report of ksolves, what I do see is they have posted good actually great numbers but do they have a differentiation? I doubt as most of these tech solutions can be provided by any systems integrator like TCS or Wipro which have better execution history and breadth and depth of customers, yes they do provide cutting edge tech solutions as in date which is shown in their reports

But these technologies also will fade away giving room to other competing better technologies in which case either the employees have to upgrade themselves or there has to be a churn which is very common across service companies in IT industry, being in IT for more than 20 years, service companies have a very competitive markets and especially system integrators which does not have huge differentiation in terms of reusable assets, products air frameworks, the project is usually won by a company which is able to onboard employees very quickly which companies with good reserve can do pretty well like Infosys or TCS

While I do see ksolves May grow Inorganically in a short term but unless they have a differentiation in terms of vision they may lag in a medium or long term

Disclaimer: uninvested but observing

5 Likes

Any updates on this? The company has give -6% returns in the past 12 months and -25% YTD.

Their numbers still look good apart from a slight fall in OPM. Am I missing something here or is it just a profit booking phase?

It still looks like a multibagger to me, would be great if anyone who has been tracking this for a long time can share their views.

2 Likes

I’ve been tracking it for quite some time. The fall in share price can be attributed mostly to the fall in margins , with the management guiding for further drop till 35% OPM.

Everything other than that seems fine.

Disclosure: Invested

1 Like

See my comments from July 2023

They’ve diversified into other areas as well, so it’s not just Salesforce now.

One domain I find particularly interesting is AI/ML. They’ve managed to train LLMs with internal data of clients and have deployed them for their use. This is no mean feat.

This is an area with good revenue potential I’d say.

But one thing I am cautious of is that the metrics/ratios seem too good to be true. Apart from the last 2 quarters maybe, everything’s picture perfect which makes me feel weird.

Disc: Exited a few months ago, but still tracking.

2 Likes

What metrics/ratios seem too good to be true?

If you are talking about RoE, I think that’s because they don’t retain a lot of their earnings and pay them back as dividends, so the equity value remains low only.

1 Like

Almost all of 'em.

ROE, ROCE, OPM, sales growth , profit growth. Sales and profit growth are still good, even after taking a hit.

It’s the perfect picture that’s making me suspicious.

OPM is high, but is decreasing now as the company is growing. Sales and profit growth have also normalized from 60-70% YoY to 30-40% now.

It is fair to be suspicious about the numbers reported, but the fact that they are actually paying out so much dividend, reduces the concerns since if they were faking the numbers, they wouldn’t be paying so much dividends.

3 Likes

Paying dividends doesn’t mean the ratios are pristine. They could be in profit, but not as much as reported to be.

I’m not saying they’re fraudulent, but it’s good to remain cautious; and I’m not against making money in these, I exited Ksolves after making a good chunk myself, but it’s always wise to be alert.

If they live up to their promises then well and good ![]()

2 Likes

I have made good money in this stock but I sold it 2 quarters back. Primary reason was the scuttlebutt I did wherein I reached out to one of my ex manager who was hired by this company.

1)The company work culture is toxic and one is expected to work like a dog.

2)There are no seniors or no lateral with good experience able to work there for long. Only the ones who stayed for too long are remaining.

3) Tech wise they may have some ground but they are playing with buzz words.

4) To create great wealth for investors, this company has to scale their operations which is not possible with the current leadership.

Basically, this company has some good growth years from a small base, from hereon it will be a tough uphill task.

8 Likes

I have been following this stock for quite some time. Is there a way to verify that they are not scam! I am totally not able to digest the fact that the OPM and Growth is so high and they are not scaling like crazy, instead of taking out dividends what are they not reinvesting in the business?

I think it is super expensive on PB but on Mcap/Sales of 6 with this high margins I see this cheap also.

Already corrected and looking to take positions but still not made my head!

1 Like

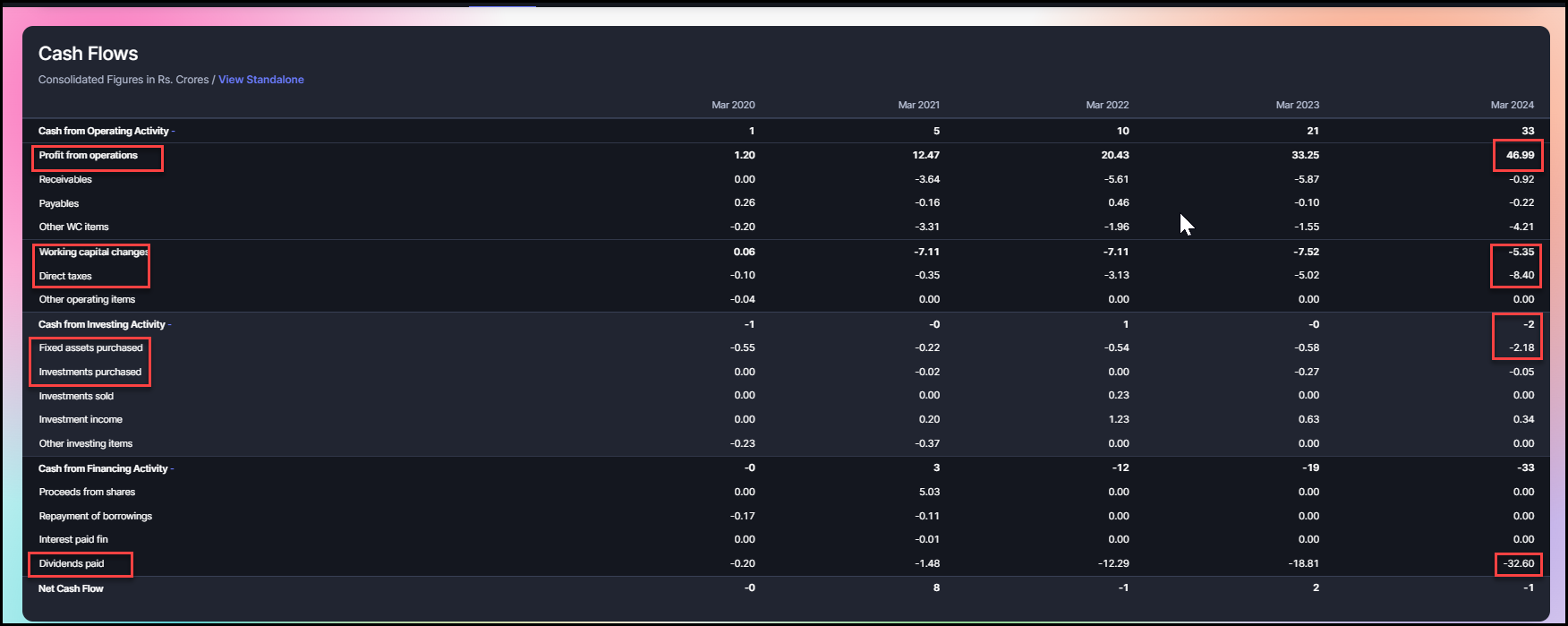

The easiest and, for me, the most trusted way to interpret this as not a fluke or scam is to simply look at cashflows. Most of what they generate or show as profit is given out to shareholders in the form of dividends. There are no borrowings to trick giving cash by taking loans. Hence, the cash going out is definitely the profit the company generates. And cash is the most tangible proof to me that the business is not a fluke.

Giving out dividends is also why its ROE and Price to Book are so high. Both these items depend on a company’s net worth (equity capital + reserves). Giving out most of what they earn as dividends makes their net worth low (as dividends are deducted from the reserves on the liability side and cash on the assets side), always keeping the ROE and PB high irrespective of their Market Cap.

IT businesses are cash machines. It is common for such companies to give out dividends as they don’t have major capital expenditures like traditional industrial businesses. They either give dividends or buy other IT comps (M&As). In this case, since this company is so small, doing M&A comes with a lot of risk, which is why they give out dividends.

I hold this company in my portfolio and try to interpret its value by looking at the PEG ratio. Here, the earning multiple is 20-21, and the company is aiming to grow at a 30% CARG basis, with 0 debt, in a business where the ROE is so high. To me, this company is a screaming buy at this level. I have and will keep adding more once I have some more cash.

If it is so good why it is falling? EBITDA margins are contracting from 42-43% to the current 36-38% levels as management is spending on marketing initiatives to bring more business/revenues. Their guidance, if you want to believe, is to maintain a 35% EBITDA minimum at all costs. Once this transition of margins phase is over, see the last 3 quarters (1-2 more to go), revenue growth (30% CAGR growth) may start guiding the valuations again instead of the Margins now (given if margins remain stable at 35-37% range).

Disc: Invested & biased & only my thesis!!

7 Likes

Alright this is my view,

I tracked this company for 6 months before I invested few months back.

I simply couldnt figure out how they are doing things and generating profit even during downturn, by simply selling salesforce, and the likes.

Let me tell you what i figured after watching all 4-5 concalls and reading their presentations.

there are 2 key people in the company. One is promoter who handles sales and other is the engineer type executor, he handles process.

What they do is they pay lesser than everyone else and have no fancy expenses like big IT, also cheaper, and lesser qualified workers comparatively as they don’t have to do any innovation or anything. Look at them as a callcenter (just a perspective on cheaper employee/culture/infra), than an IT org. and you will understand what I mean.

These are very grounded people,

My only concern is high dividends and 3 cr. each salary promoter extract on his name and his wife name, who supposedly does something in leadership position in HR if i remember right.

Btw, now they are opening office in US, to avoid tariff problem, they have been trying to develop US business since last 3 quaters, maybe they are simply lucky that as soon as they developed US market, this issue arose and they will shall have an advantage now.

Their expense is increasing too as they are now going for expansion.

2 Likes

Sorry but I have strong disagreements with some of your points and felt like I should jot it down.

If this is true I’d stay out of this. I’ve worked with startups like this, the overall atmosphere is of resentment. The talented ones jump ship at the first opportunity, and the mediocre ones stay because they don’t have a choice. It’s impossible to grow beyond a point without raw talent at the ground level, no matter what the top management says.

The so called fancy expenses are for attracting talent. Nobody wants to work with shabby infrastructure and facilities, more so when there are better opportunities out there.

Exactly, this is your classic local IT company. The boss keeps everything for himself and pays the employees poorly. They’re not going bust with this attitude, but they won’t grow either.

In the last few concalls they said they’re trying to focus more on AI projects. If that’s the case then this is the opposite of what they should be doing.

IMHO they’re a poor business, and they’ve extracted every bit from this modest setup. Unless they change their attitude (unlikely , as they say, the cheetah never loses its spots) they’re not going anywhere.

Disc:Made a good chunk of money because I invested early, exited when I felt the runway was mostly over.

2 Likes

RKD,SumeetS & Metal Head

I have been following this company and have seen the comments about work culture. I have 20+ years of Leadership experience and have worked in a mid size setup (within a large company) also. Based on that thought of sharing my views-

-

Employee Ratings- For a very small company, growing at good pace with ambitious promoter is a tough place to work. As there will be no fixed rules to work, you have to work extensively if a dead line is close by, promoter interference will be quiet high and will be much more sharper as compared to a professional CEO. Also work culture will be largely driven by ability of promoter and Co promoter (Who manages HR also). So employee satisfaction rating are bound to be erratic. Still at ambition box rating of 2.9 and at glass door 3.2, things look not that bad.

(PS- When L&T boss talks about work hours, consider your experience of slogging, working like dog can be a common phrase applied for any company) -

If you see advent of AI and LLM there is huge scope for Mid size company who can do small budget but very effective implementation of AI in business process. I guess all big IT companies will be hesitant to take small AI projects which I see will come in leaps and Bounds. They will be a steppingstone to get entry in a company and drive long term relationship. Sales force or front end revenue generation projects are great lead as they are easiest to sell and very effective in delivering ROI on IT project.

-

Look at the way they are giving ESOPs. If not all get credit to promoter than it means that employees are pushed for long term and all know ESOPs are best value creator for the employee if company grows. So to me thats a positive sign (Also see the ESOP discount in grant letter put up by company…they are not at large discounts). This I see as a negative point also as vesting period is an year, so all ESOP in hands of employees who exit will sell and that small quantity it seems is putting pressure on stock price

-

Management focus on stock price management by giving frequent split, bonus etc is huge negative. Other side to make ESOP attractive, you need to have an eye on it (Also to drive engagement and push employees for higher growth)

PS- Invested

3 Likes

Totally agree with this, I had voiced something similar some time ago

It seems people notice the comments on valuepickr a lot ![]()

Share up 6% today (A jump seen after lot of time)

Thanks RKD for your comments. AI/ML is new to me but last week I have done a two full day workshop. It was eye opener and suggest you all guys to orient yourself with AI/ML. Coming back to your response training company data on AI/ML is something not a great capability, but most in demand and good job can open doors for many more such initiative. So yes, good times for this company.

Dis- Invested, not a subject matter expert in IT, AI/ML

1 Like

correct - training is not a niche and infact, all IT companies are doing it and is part of most service offerings - metrics seem too good if its only because of AI

In IT margins are always good. They come down due to high salaries, lavish travel and infra, which it seems Ksolves is managing well and is often talked about in investor calls

1 Like