Sharing some notes we collated on KSB. Plz share any industry feedback or insights

Valuations - ~20x trailing and 16-17x 1 yr fwd. Paharpur group – indian promoters – bought from open mkt 1 lakh shares in the last week of March 21 around 800 Rs

About KSB

- KSB India is a subsidiary of the German group KSB Aktiengesellschaft, which is a supplier of pumps, valves and related services, with headquarters in Frankenthal (Pfalz), Germany. The parent has more than 16,000 employees, with annual consolidated sales EUR2.4bn

- KSB is engaged in the manufacture of customised pumps, with applications in thermal/nuclear power plants, refineries and offshore oil rigs, sugar and paper industries, irrigation, water supply, waste water management, etc.

- The business is structured into two broad segments, namely Projects (Thermal power plants, Nuclear power plants, O&G) and Standard Products (Agriculture, Waste Water, Construction & Domestic) contributing ~50% each to the top line

Management Change - First time since inception in India. an Indian Rajeev Jain was given charge of KSB India in 2015-16. Rajeev Jain was President, South Asia KSB (Indonesia & Singapore). KSB is now customising solutions for Indian market more aggressively and see the gain in market share below under Rajeev Jain’s stewardship

Opportunity

- Market leadership (#3) in India. KSB sees good growth opportunities in the Indian market (~Rs120bn) and targets to attain the #1 position in Pumps over the mid-to-long term (vs #3 position currently and #6 in CY17)

- With capacity built up ahead of competition and pre-qualification in place, we expect opportunities in

- FGD (flue gas de-sulphurisation) and the Atma Nirbhar vision are perceived as the largest opportunity. Atmanirbhar Bharat - KSB is one such key operator in pumps as 95% of its pumps are manufactured locally, with only 5% (special parts) sourced from out

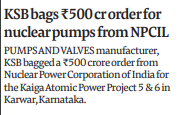

- nuclear - NPCIL announced 12 reactors (each 700MW), a Rs3bn opportunity each by 2031

- O&G (Oil & Gas) - Stabilising crude oil prices would lead to capex by oil producers.

- Agriculture, “smart” cities and wastewater management also throw up healthy prospects

- Exports - parent is using KSB India for sourcing of products too. exports have doubled in the last few years

Sales

- Domestic Sales -83%, rest exports. After-market and services (19% of its revenue

- top-7 customers, which bring 20-25% to the business, are NPCIL, HME Mittal Energy, ISGEC, L&T Hydrocarbons, IOC, Thermax and BHEL

Margins - Earlier suppressed owing to Chinese competition. After preference to Indian manufacturers, however, margins are now comfortable.

Initiatives

- Valves

- KSB has traditionally focussed on pumps, but has now grown itsValve portfolio (much larger market than pumps), led by development of a Valve facility at Coimbatore and acquisition of MIL

Controls from United Breweries in the past.

- additional factory shed in Sinnar

- storage facility at Tarapur (contractual obligation for

storage and testing for NPCIL),

- shaft grinding machine & Mech seal testing set up for execution of NPCIL orders, FGD lining room

extension (due to uptick in FGD ordering),

- Group solar (JV with service provider company),

- 3D printing machine (to facilitate design, development & rectification of product),

- mechanical seal localisation

- IVC ball valve project.

Risks

- Impact of commodity headwinds on margins to be curtailed by selective price

actions, cost initiatives and localisation

- Deferred Capex

Ashish Kila

Perfect Research

Disclaimer

We are not SEBI registered advisors

The above note is not an investment advice but an educational post to discuss a business model

Plz consult your financial advisor before taking any decision

Thank you for the thread on this name. I was trying to get a visibility on potential revenue growth for this company for the next 2-3 years. If see the following article (link - KSB net rises 25.91%; co reports surge in demand for pumps, valves - The Financial Express) the company mentions that they will do annual capex of Rs80-100cr in CY22 similar to CY21 (though in CY21 from their cash flow capex comes to only Rs38cr). If I build ~Rs90cr capex in then the gross block which was estimated at Rs760cr in CY21 (taking Rs723cr gross block of CY20 and adding Rs38cr capex from cash flow of CY21) rises to Rs851/941cr in CY22/23 (some of the capex can be maintenance/non-revenue generating as well). Last 5 year average asset turn on gross block has been 1.8x and in CY21 it was estimated at 2x. Taking 2x gives revenues of ~Rs1600/1800cr in CY22/23 implying growth of 9%/11% y/y.

KSB globally has almost monopoly in cryogenic valves ,pumps and systems used for handling LPG and LNG plants India percentage of gas as fuel is increasing.I have experience of using and procuring them.

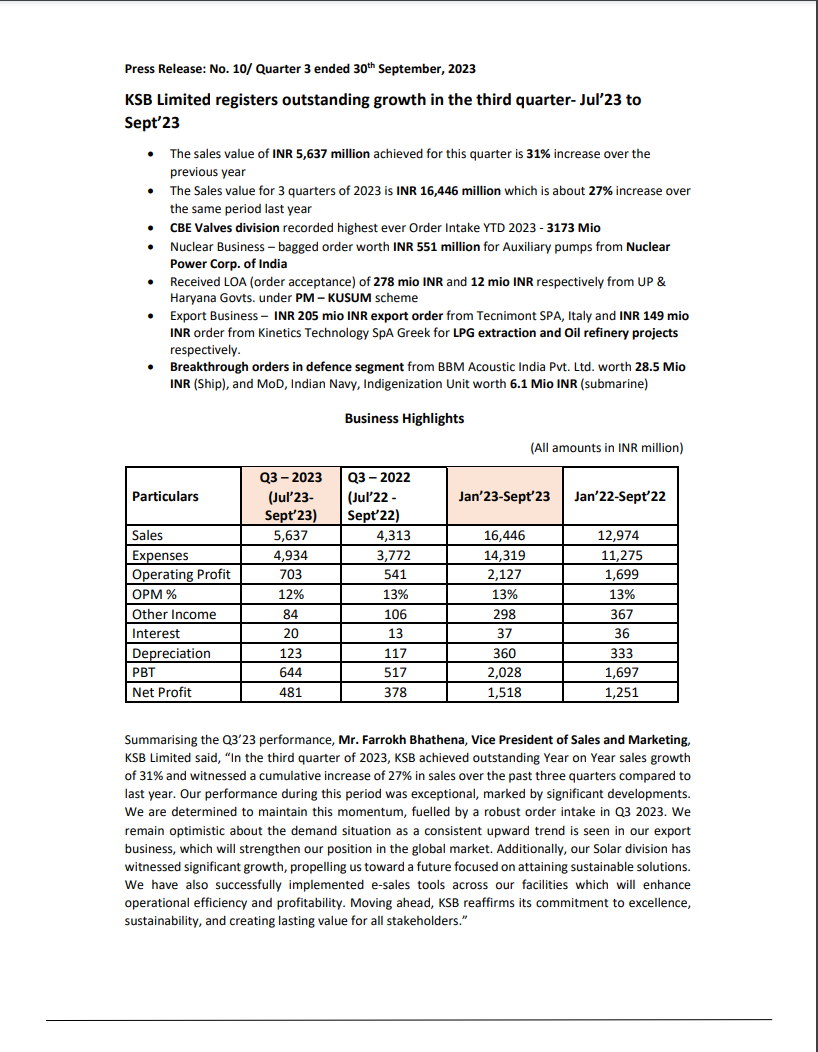

KSB Limited, a company, has reported impressive financial performance in the third quarter of 2023 (July to September). Here are the key highlights:

Sales Growth: KSB achieved significant sales growth, with a sales value of INR 5,637 million for the quarter, representing a remarkable 31% increase compared to the same period in the previous year. This indicates a strong demand for their products and services.

Cumulative Sales Increase: Over the first three quarters of 2023, KSB reported a total sales value of INR 16,446 million. This represents a substantial 27% increase over the same period in the previous year, underscoring their sustained growth.

Divisional Achievements: Several divisions within the company made notable achievements. The CBE Valves division recorded its highest-ever Order Intake Year-to-Date (YTD) in 2023, amounting to 3,173 million INR. The Nuclear Business secured an order worth INR 551 million for Auxiliary pumps from the Nuclear Power Corp. of India.

Government Orders: KSB received Letters of Acceptance (order acceptances) of 278 million INR and 12 million INR from the governments of Uttar Pradesh (UP) and Haryana, respectively, under the PM-KUSUM scheme. These orders are significant for the company.

Export Business: The Export Business also performed well, securing an export order of INR 205 million from Tecnimont SPA in Italy and an INR 149 million order from Kinetics Technology SpA in Greece. These orders are related to LPG extraction and oil refinery projects.

Defense Sector Orders: KSB received breakthrough orders in the defense segment. BBM Acoustic India Pvt. Ltd. placed an order worth 28.5 million INR (ship), and the Ministry of Defense (MoD), Indian Navy, Indigenization Unit, issued an order worth 6.1 million INR (submarine). These orders strengthen KSB’s presence in the defense sector.

Financial Summary: Here is a summary of the financial performance for Q3 2023 compared to the same period in the previous year:

Sales: INR 5,637 million (2023) vs. INR 4,313 million (2022)

Operating Profit: INR 703 million (2023) vs. INR 541 million (2022)

Net Profit: INR 481 million (2023) vs. INR 378 million (2022)

Operating Profit Margin (OPM): 12% (2023) vs. 13% (2022)

Company Perspective: Mr. Farrokh Bhathena, Vice President of Sales and Marketing at KSB Limited, expressed their optimism regarding the demand situation. They highlighted the upward trend in their export business, which is strengthening their position in the global market. KSB also mentioned their focus on sustainability and efficiency improvements, with the successful implementation of e-sales tools across their facilities to enhance operational efficiency and profitability.

Hi Ashish, the company has grown reasonably well since the time you posted about the co. ( June’21 )…Are you still holding this as the p/e is expensive now at 64…