Is Diagnostic sector bottoming out? Some signs visible in chart but still weak, given it was a fancied sector last year, euphoria is out and valuations are more saner now. With some more consolidation we should get next leg of journey post Q4 nos.

Coming back to Krsnaa , Here is a recent presentation,

Inferences based on past numbers, idea is to get unit economics for longer term and see how it would look like in future( validation of mgmt guidance), pl note numbers are approximation and annualized for FY22

-

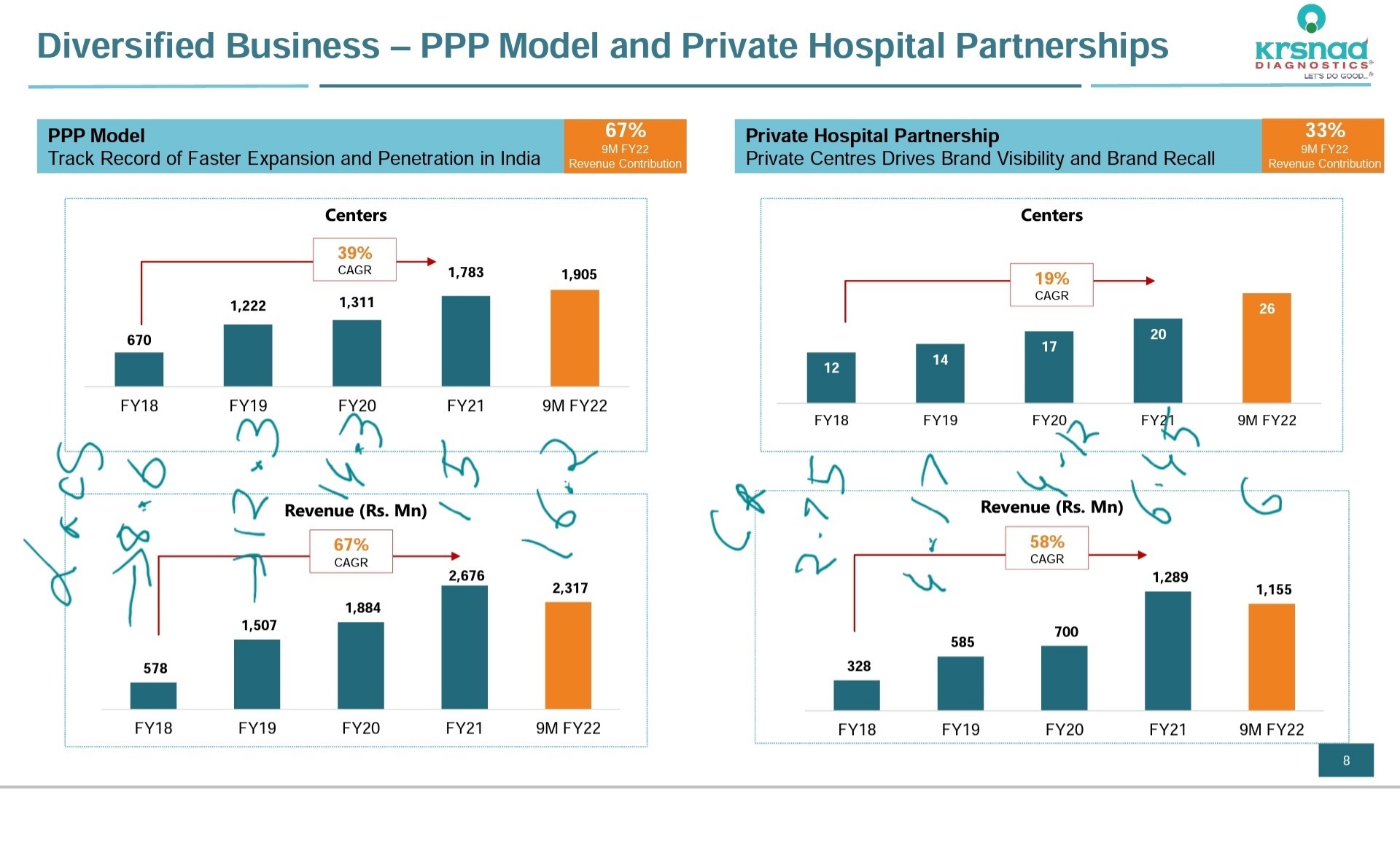

How has revenue growth and realization fared over last few years for both channels - PPP & Private hospitals, Trend is encouraging and seem to have doubled over last 5 years

-

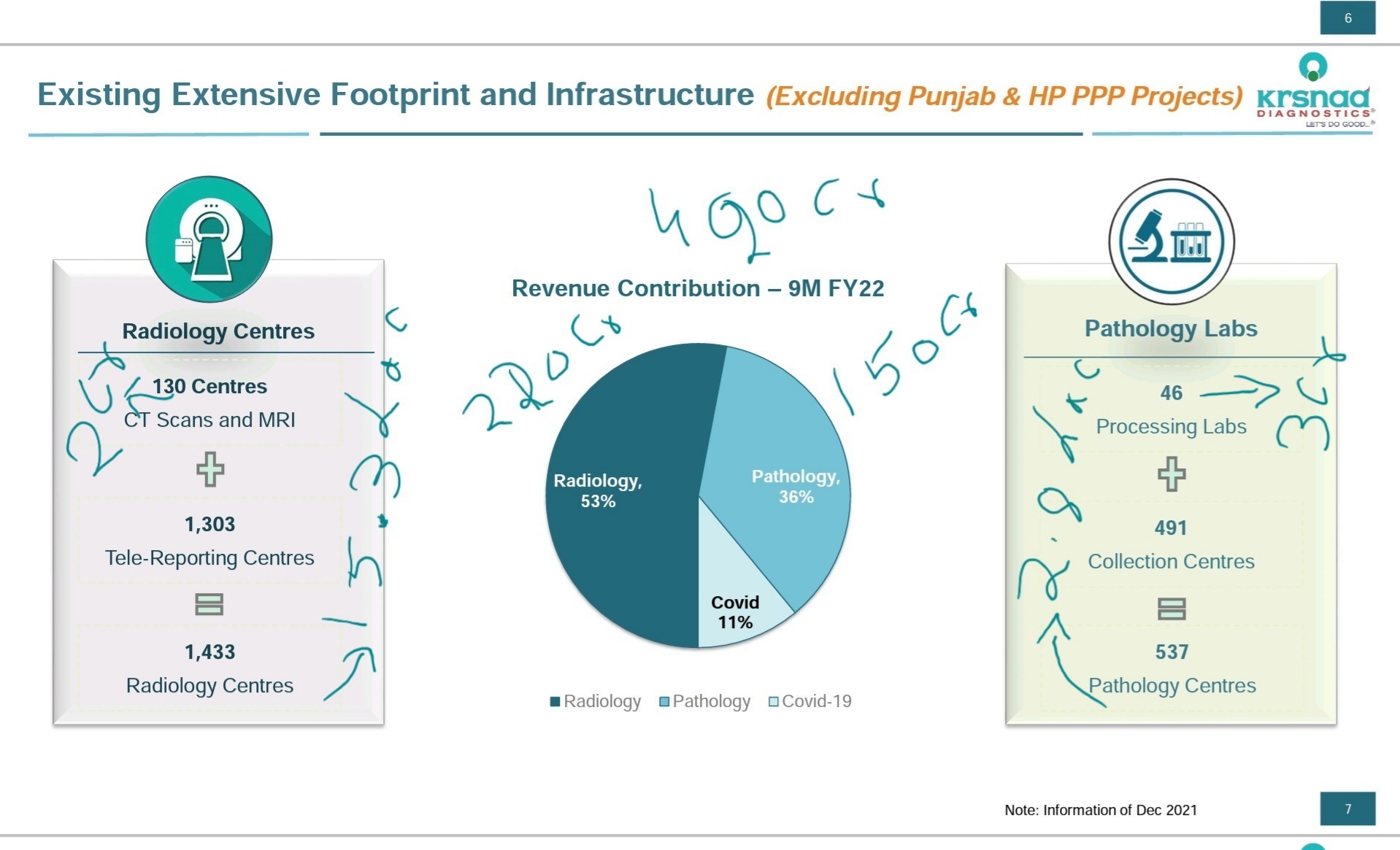

Let’s look at Radiology vs Pathology for FY 22( again annualized and approx, excluding covid nos) - Radiology center at 2Cr( 130 centers and 220 cr revenue) and Pathology center at 3Cr realization - (46 centers and 150 cr revenue)---- Annual non covid revenue at 420 cr approx

-

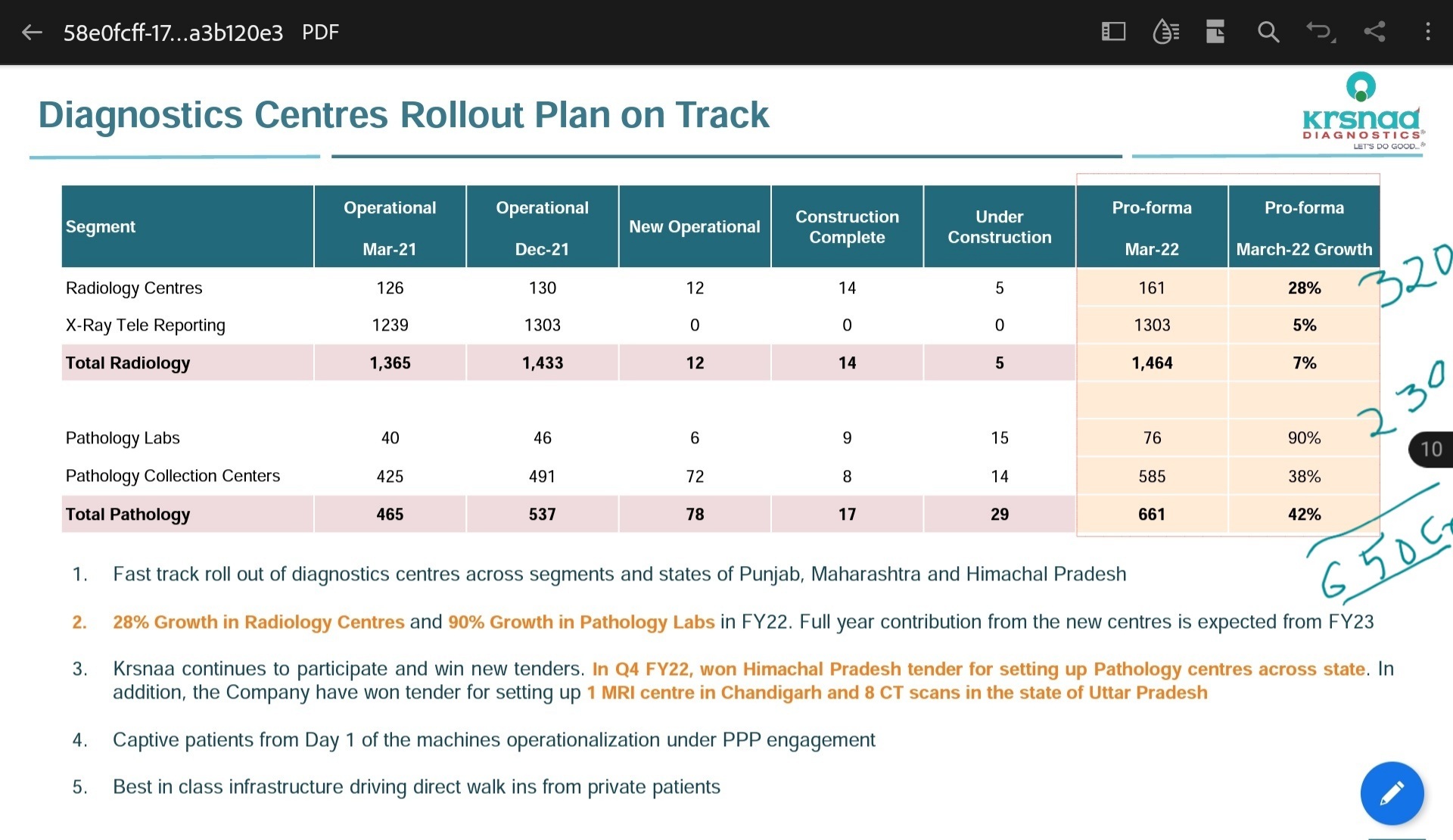

If above were to be applied to recent expansion in FY22, what can FY 23 look like, at current runrate a 650 Cr+ is doable( older center maturing and B2C channel can add upside)

-

Margins - last 2 Qtrs company has delivered 30% EBDITA and interest burden going away, Net profit margin is around 14% in Q3

Optimist case - 650Cr-680Cr revenue, 30% EBDITA = 210 cr+, 14% NP = 90 Cr,

Base case- 650 Cr revenue, 28% EBDITA = 180 cr+, 12% NP = 80 cr

Given industry is a high teen growth, high longevity, 20X EBDITA is a optmist case valuations at 4000 Cr+ mkt cap, at 15X EBDITA in base case 2700cr+ mkt cap. Current mkg cap is around 1650 cr. B2C players are at much higher valuations of 30X-35X+ EBDITA at similar margin profiles.

Krsnaa has called out 2X revenue and 3X profits in 3years, to be seen how they deliver in next 2-3 Qtrs.

Invested with minor allocation, plan to build up per execution in coming Qtrs.

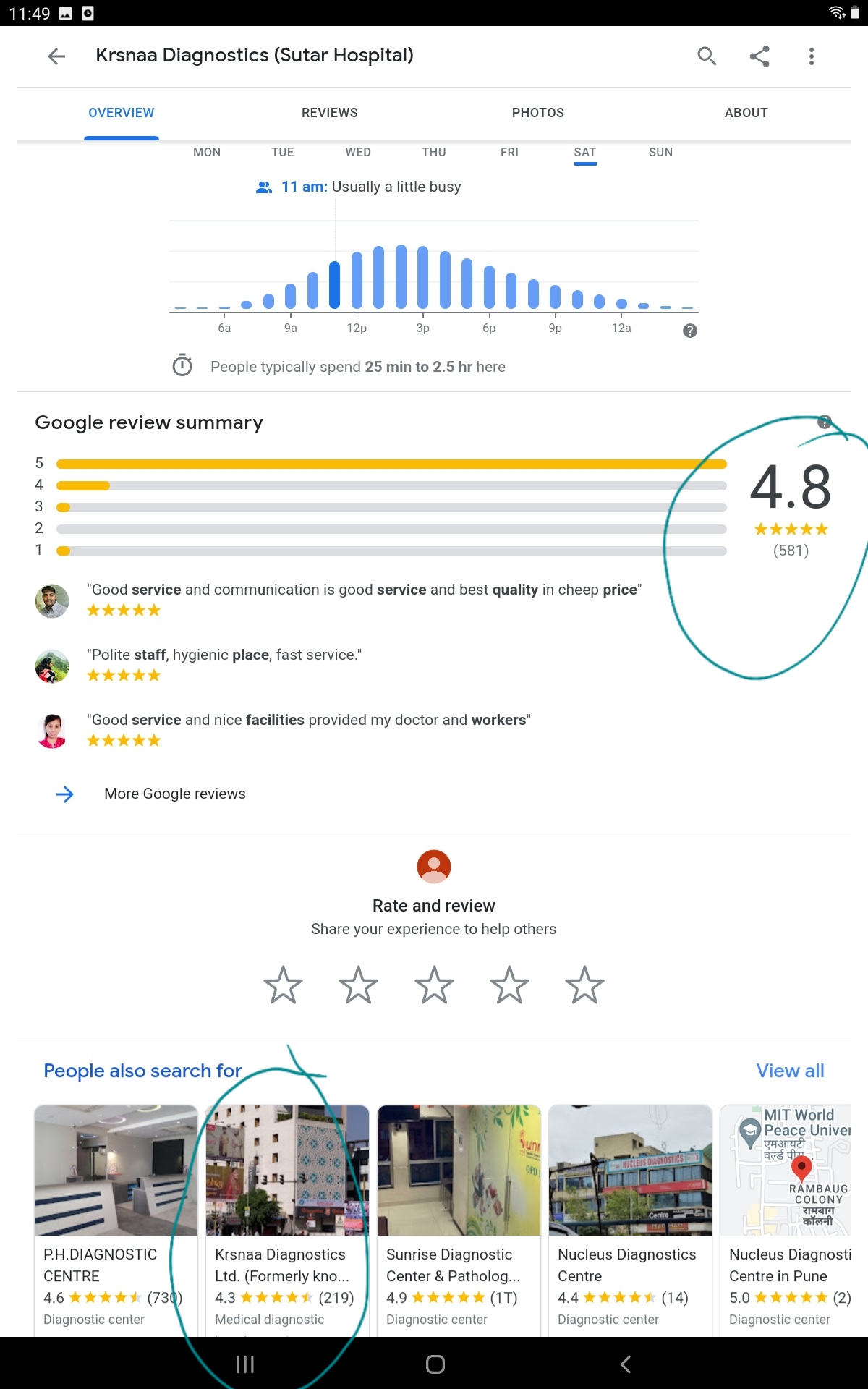

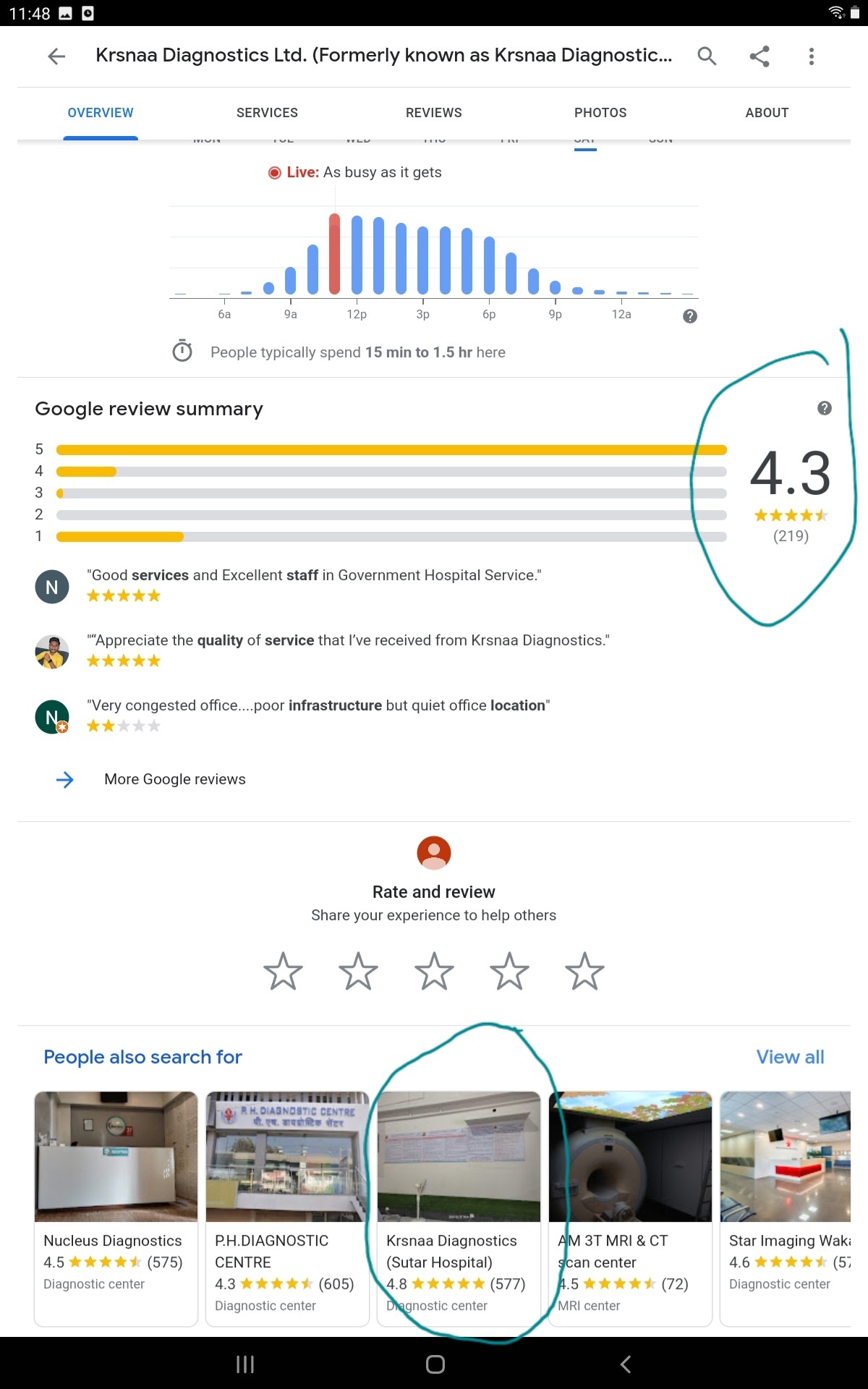

Edit - Adding some scuttlebutt online - Pune Krsnaa reviews - ssmple size is good, they are rated inline/better with private peers - on quick glance one can see Radilogy reviews as well( which are complex and still has good reviews - price, facility, service quality, )

Patient reviews on Radiology are quite encouraging and reflects B2C elements playing out as well - word of mouth spreads faster

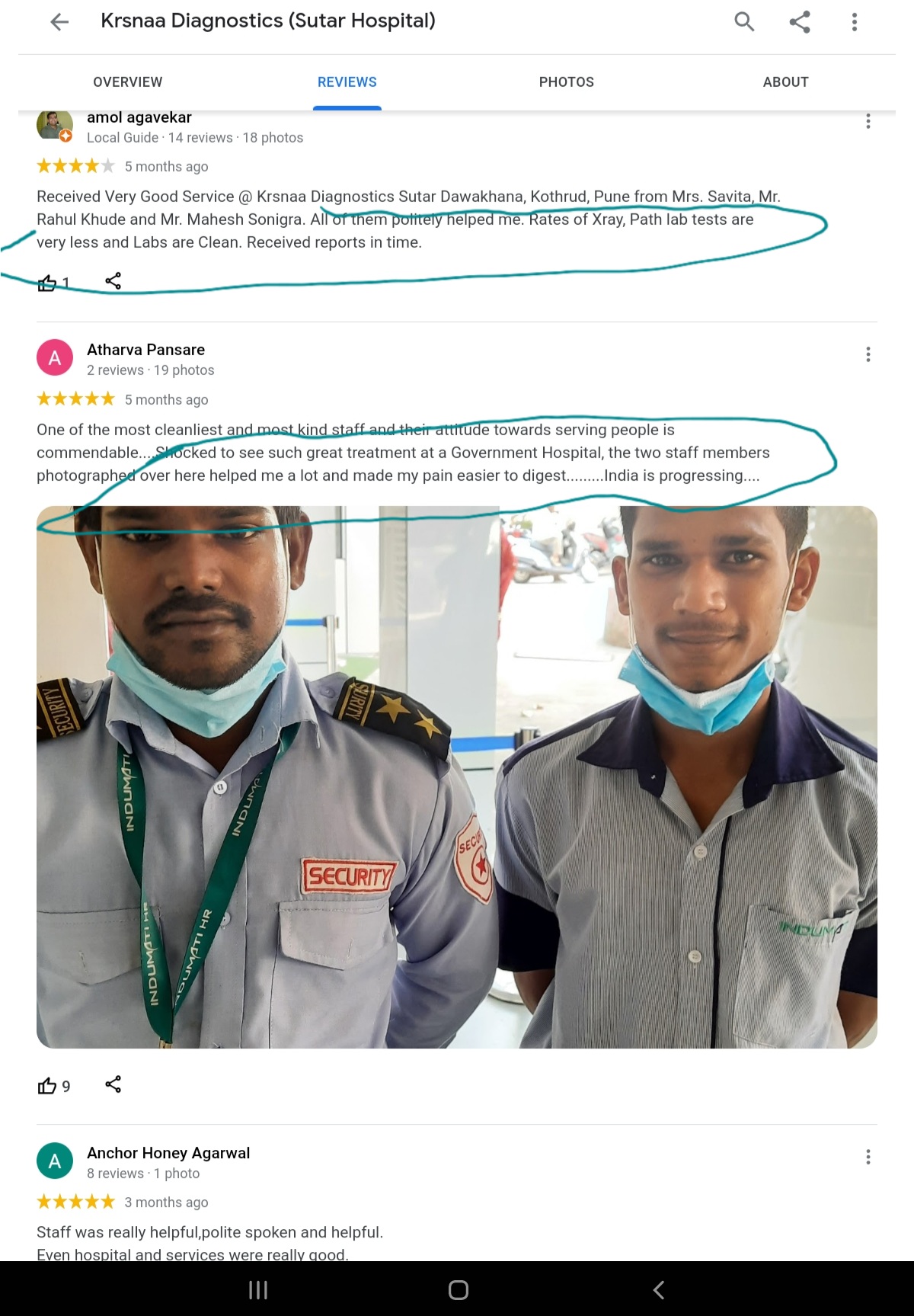

Politicians pointing issues in PPP model is understandable, esp those in opposition, NGO has agendas as well, most of them wants us to believe nothing is good/improving about India, I have been to a govt hospital recently and was impressed with efforts on , security, cleanliness, almost nil pricing and lab facilities ( not Krsnaa but other local), point is do visit to see the change, may not be at par with private( e.g AC, staff, infra maint like wall paint, lift quality, etc ) but dramatic improvement from what it used to be like going to govt hospitals a decade back. One can visit and see for themselves as most of large and mid size cities have ppp model run setups now.