Krishana Phoschem Limited - Detailed Analysis

1. Business Overview

Krishana Phoschem Limited (KPL) is a part of the Ostwal Group of Industries and is engaged in the manufacturing of fertilizers and industrial chemicals. The company operates a fully integrated business model, focusing on:

- Fertilizers:

- Single Super Phosphate (SSP) – 0.12 MMTPA

- NPK/DAP Complex Fertilizers – 0.33 MMTPA

- Industrial Chemicals:

- Phosphoric Acid – 0.099 MMTPA

- Sulfuric Acid – 0.264 MMTPA

- Beneficiated Rock Phosphate (BRP) – 0.20 MMTPA

KPL has a strong distribution network of ~2,500 wholesalers and ~30,000 retailers across 9 states. It has been aggressively expanding its production capacity, with significant investments in plant modernization and the relocation of its DAP/NPK facility from Spain.

2. Opportunity Present Here

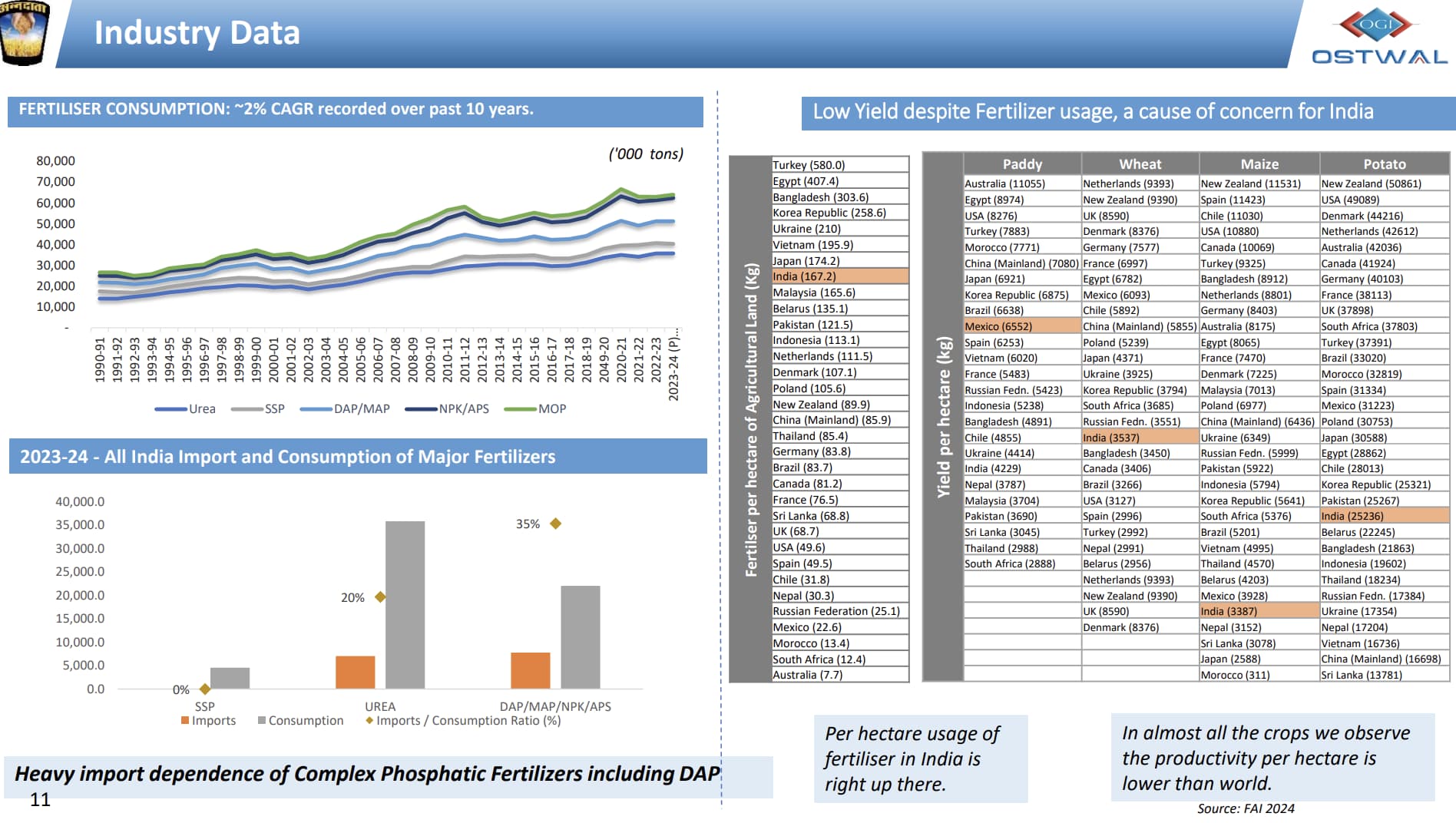

The Indian fertilizer industry is growing at a CAGR of 6-6.5%, expected to reach USD 62-70 billion by 2030. KPL operates in the phosphatic fertilizer segment, which constitutes about 20-25% of this market (~₹8-11 billion TAM).

- Strong demand for phosphatic fertilizers driven by government subsidies and increasing agricultural productivity.

- Backward integration in raw materials (rock phosphate, sulfuric acid) ensures a cost advantage.

- NPK segment growth – The company has recently achieved 79% utilization of its DAP/NPK plant, showing strong demand traction.

- Government policies like the Nutrient-Based Subsidy (NBS) scheme support phosphatic fertilizers, providing stability in pricing and margins.

3. Positives

-

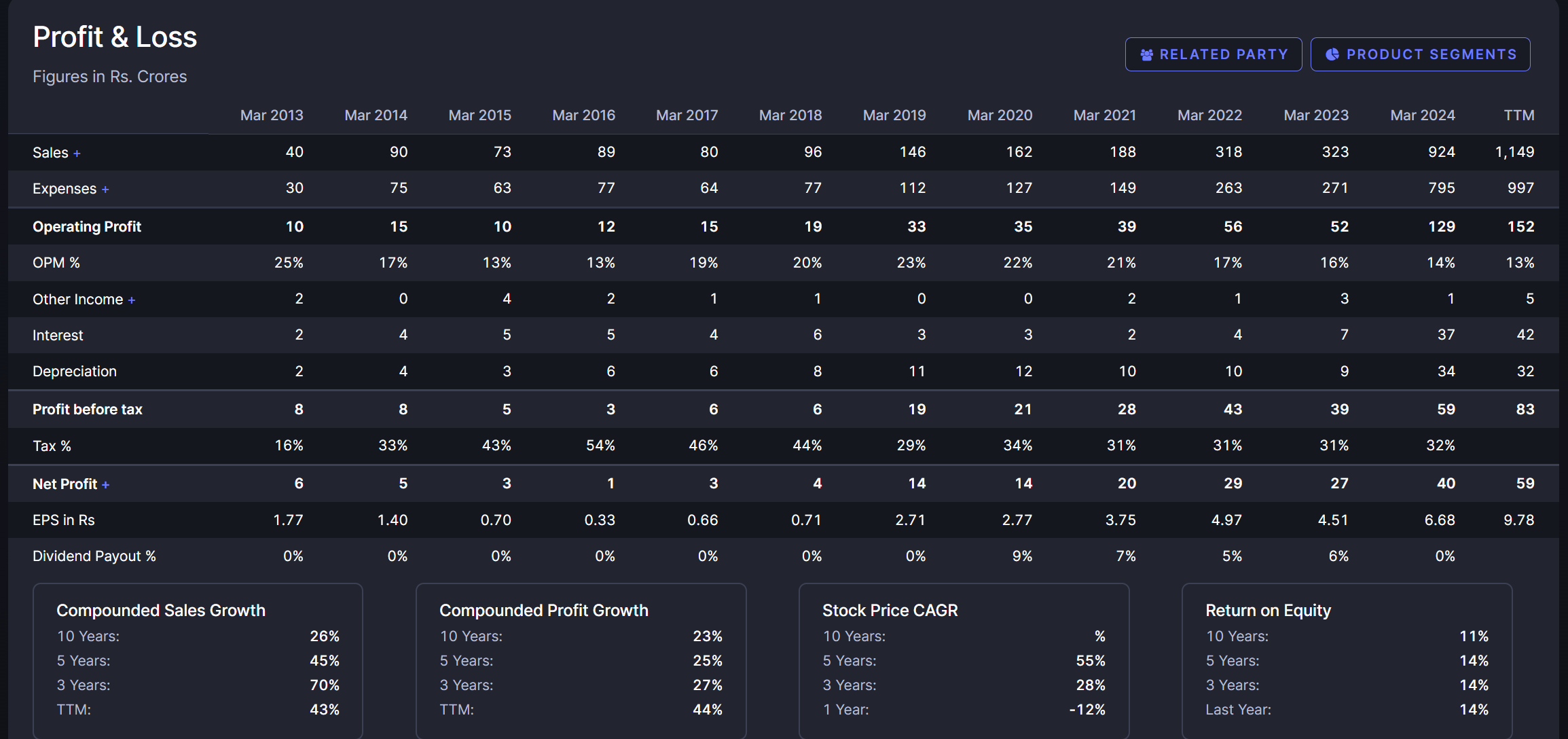

Strong Revenue Growth:

- Sales have grown 28x in 11 years (₹40 Cr in 2013 → ₹1,149 Cr in TTM FY24).

- Q3 FY25 revenue was ₹304 Cr, up 32.1% YoY.

-

Profitability Improvement:

- EBITDA in Q3 FY25 was ₹44.3 Cr, up 88.5% YoY.

- PAT grew 454% YoY to ₹20.5 Cr in Q3 FY25.

-

Capacity Expansion is Bearing Fruit:

- SSP utilization at 100%, NPK at 79%.

- Sulfuric acid capacity expanded from 99,000 MTPA to 165,000 MTPA.

-

Subsidy Receivables Declining:

- Down to ₹93.5 Cr (Q3 FY25) from ₹110.5 Cr (Q2 FY25), showing improved cash flow management.

-

DCF & ROE Comparison:

- KPL’s ROE = 14.4%, ROCE = 15%, much higher than competitors like Paradeep Phosphates (3% ROE).

- Despite negative FCF, its intrinsic value could improve as capex stabilizes.

-

Lower Competition from China:

- China’s export restrictions on fertilizers benefit Indian manufacturers like KPL, providing domestic pricing power.

-

Strong Long-Term Supply Contracts:

- Secured raw material supply (rock phosphate from Egypt, Jordan, and domestic sources).

4. Negatives & Red Flags

-

Declining Margins Despite Growth:

- Operating Profit Margin (OPM) fell from 25% (2013) to 13% (TTM FY24).

- Increasing expenses (raw material, logistics, and energy costs) are a key challenge.

-

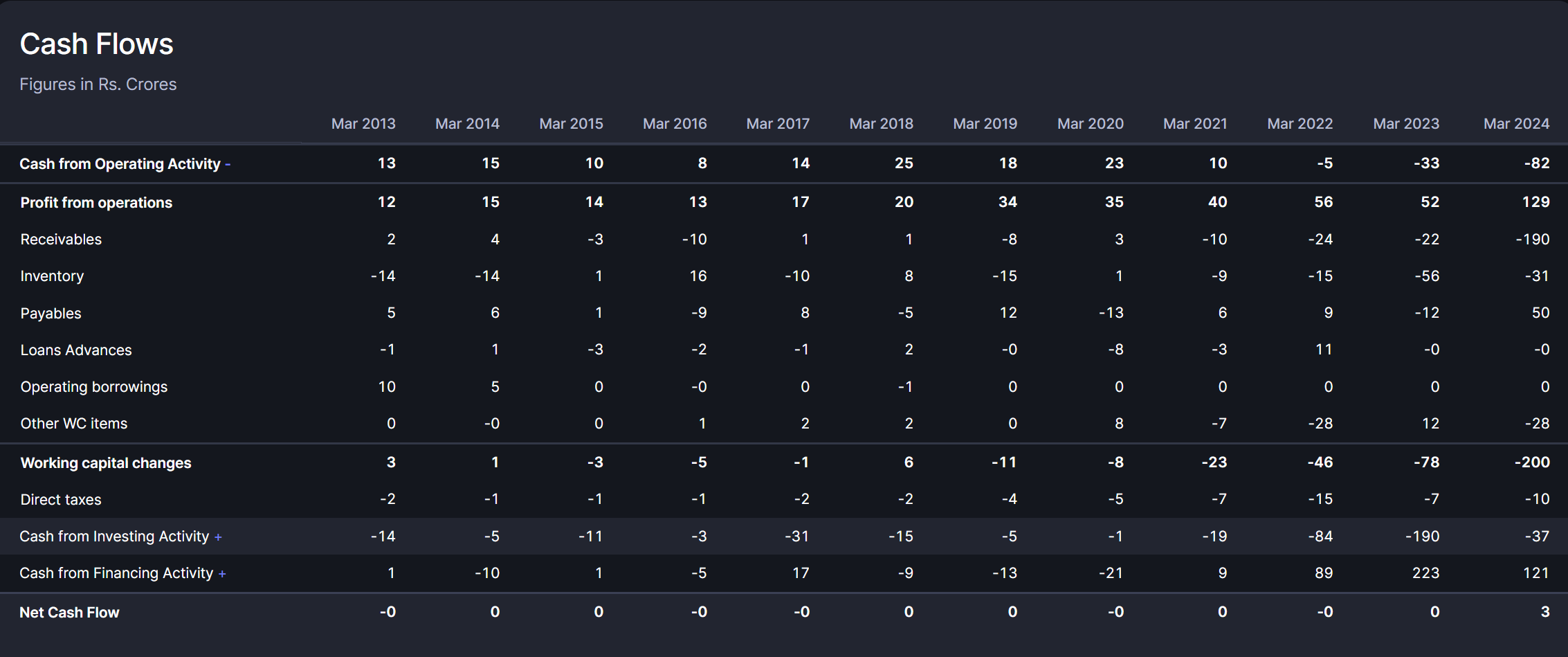

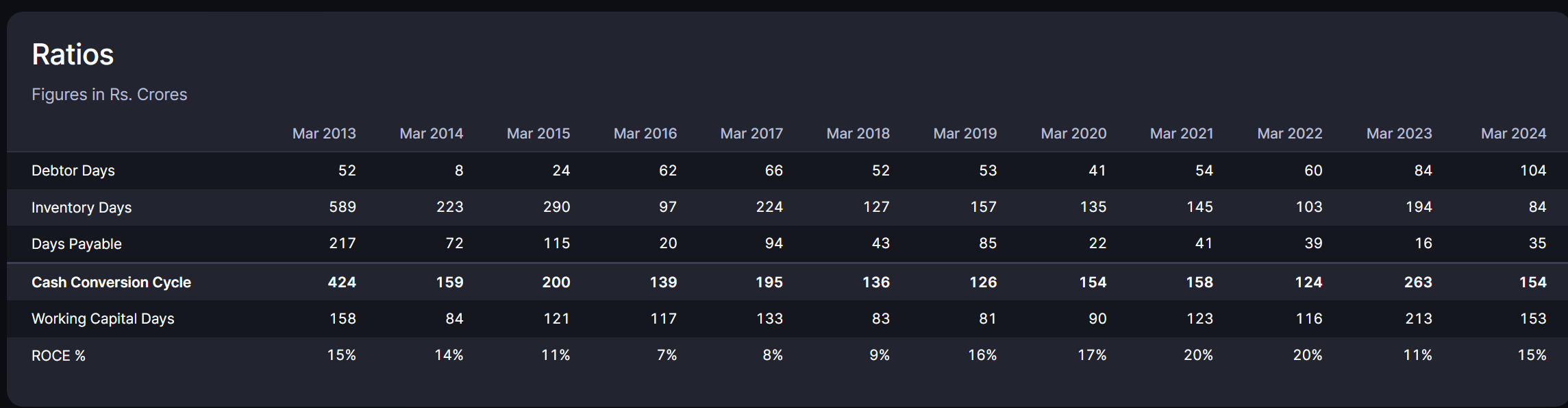

High Working Capital Requirement:

- Receivables surged to ₹190 Cr in FY24, causing a major cash flow crunch.

- Inventory also remains high at ₹31 Cr, impacting liquidity.

-

Negative Free Cash Flow (FCF) = ₹-119.8 Cr in FY24:

- Heavy capex and subsidy delays are hurting FCF.

- The company needs better working capital management to sustain expansion.

-

High Debt Levels & Interest Costs:

- Interest expenses jumped from ₹2 Cr (2013) to ₹42 Cr (TTM FY24).

- Increasing debt servicing cost may impact profitability if cash flows remain weak.

-

DCF Valuation Suggests Overvaluation:

- Based on simplified DCF analysis (₹912 Cr intrinsic value), the stock is trading above its fair value (₹1,318 Cr market cap).

- The market seems to be pricing in higher future growth or lower risk.

-

Cyclical Business, Dependent on Government Policies:

- Any reduction in fertilizer subsidies or policy shifts in NBS could hurt margins.

-

Limited Geographic Reach:

- KPL is still largely concentrated in a few states (Madhya Pradesh, Chhattisgarh).

- Need to expand into high-demand states like Maharashtra, Gujarat, and UP.

5. Final Thoughts & Investment Outlook

Krishana Phoschem Limited has strong revenue growth, expanding capacity, and a well-integrated business model. However, key concerns like working capital management, high debt, and margin compression must be addressed for sustainable profitability.

Who Should Consider This Stock?

- Long-term investors looking for a high-growth fertilizer company with strong expansion potential.

- Investors betting on the Indian agriculture & fertilizer sector boom.

- Those willing to hold despite short-term cash flow issues, expecting strong free cash flow once capex slows.

Who Should Avoid?

- Short-term traders, as subsidy receivable delays and working capital crunch could cause volatility.

- Conservative investors who prefer positive free cash flow and low debt.

“Please forgive me if I made any mistakes, and kindly correct me wherever I am wrong.” (DISC:: IM INVESTED FROM AROUND 200,WILL ADD MORE)