I have kept the report short and precise about the key points

ABOUT THE COMPANY-:

Krishana Phoschem Ltd is a subsidiary of Ostwal phoschem (India) Ltd. And a unit of the Ostwal group.

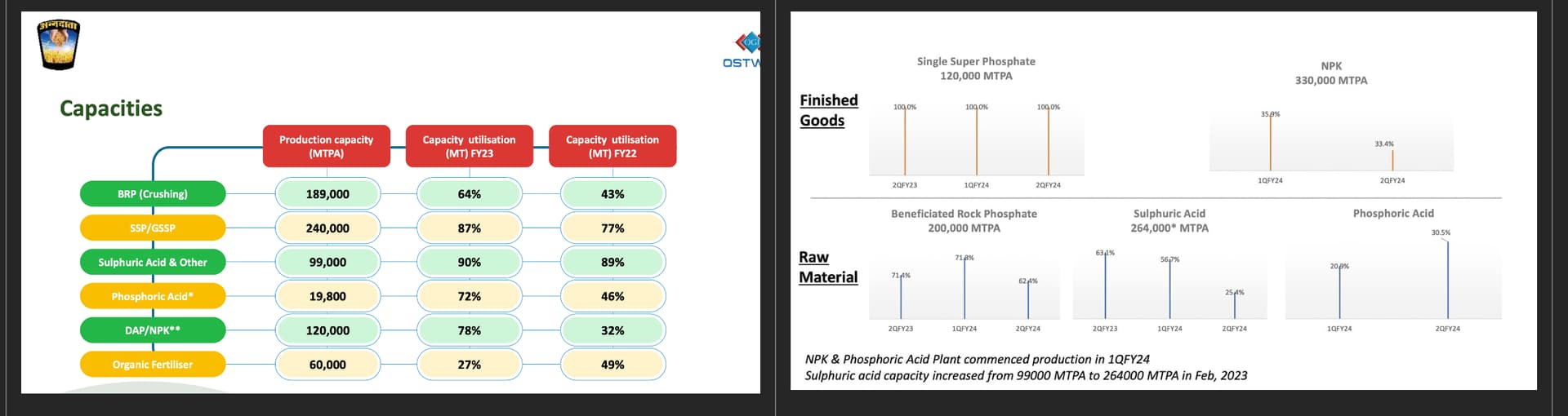

The company is in the production of Beneficiated Rock Phosphate (BRP), Single Super Phosphate (SSP), Granulated Single Super Phosphate (GSSP) that are greatly required in the agricultural industry and Sulphuric acid, H-acid, dyes and other chemicals. KPL has distinction of having fully integrated SSP, GSSP manufacturing process which is one of its kind in the country.

The Ostwal group is marketing its fertilizer products under the own brand name of “ANNADATA” in the states of Madhya Pradesh, Gujarat, Maharashtra, Rajasthan, Punjab, Haryana, Udisha, Himachal Pradesh, Utter Pradesh and Uttarakhand. The group has appointed a network of 1000 distributors who in turn supply to more than 9000 dealers

INDUSTRY AND PRODUCT SPECIFIC TAILWINDS -:

• Consistently good Monsoon Augurs well for fertilizer demand

• Government subsidy release and other reforms are very positive

• Company is consistently increasing its distribution network and adding to market shared. Plus, there remains a big addressable market (which is growing too…)

• Company manufactures mainly SSP (single super phosphate) and other phosphate related fertilizers. In short it helps in replenishing Phosphate in the soil which was taken by previous crops. Nitrogen fertilizer type (Urea etc.) is the major type of fertilizer used (65%) compared to (25%) of phosphate. But excessive use of nitrogen causes adverse impact on soil, crop and overall eco system. Growing use of nitrogen is a cause of concern in many countries. China is reported to have decided to freeze the consumption of nitrogen at the existing level. So, there’s a good chance of substitution demand. 41% of phosphate fertilizer demand is satisfied through imports. So, there’s a good chance of substitution of import as well.

BRAND NAME: A very marketable and frankly great brand name “ANNADATA”

BIG CAPACITY EXPANSION PLANS:

KPL is planning to setup new project Di-Ammonia phosphate (DAP) 1000 TPD, Phosphoric Acid 100% 300TPD & Sulphuric Acid 500 TPD at AKVN Ind. Area, Meghnagar Dist. Jhabua (M.P.). It has envisaged to commence project work from FY22. This mega capex project is expected to done in phases. The land is already been allotted to the company and the plant machinery is starting to arrive at the site.

This should allow the Company to Increase its scale very fast and offer clear growth drivers for the future.

INCOME STATEMENT:

HIGH OPERATING MARGINS -: Average last 5-year ebidta margin – 21% (probably the highest amongst fertilizer companies). Above is a result of integrated business operations (the high margin chemical division helps a lot in the overall margin profile)

HIGH AND CONSISTENT REVENUE GROWTH -: 16% CAGR over the last 5 years (this along with consistent increase in profitability is a very good sign)

BALANCE SHEET:

Low Debt (16cr) (15x Interest coverage ratio)

Working capital Position is satisfactory (especially for a fertilizer company)

CASH FLOW:

Satisfactory Cash flow generation

OCF/EBIDTA -: 80%

FCF/EBIDTA -: 17% (acceptable considering the growth they have had and that the company is in growth stage

RETURNS ON CAPITAL:

Satisfactory Returns on capital -: Average 8-year ROCE (14.1%)

Average 5-year ROCE (15.8%)

Average 3-year ROCE (19.0%)

Return on capital is consistently increasing on average

ROIIC (RETURN ON INCREMENTAL INVESTED CAPITAL) -:

10 YEAR ROIIC – 24%

5 YEAR ROIIC – 39%

ROIIC numbers show that company is reinvesting its capital at great and increasing returns.

VALUATION-:

Company is currently trading at a very fair value

8X EV/EBIDTA, 10X EV/EBIT

Meaning we get all the future growth of the company for free along with multiple re-rating possibility.

KEY RISKS:

EXECUTION RISK: The Company’s capacity expansion plan is very big and ambitious. To the tune of 321 Cr. Of which the company estimates 60% will be debt and 40% will be internal accruals. It will be implemented in phases, taking annual internal accruals and debt as required.

So, the execution risk is definitely there. (But it’s the one kind of risk , that we as investors bet on/ can’t do away with.

Following isn’t a key risk but more of a negative point-: Loans given to Group companies. (Note: all loans have been duly paid along with interest) Company has a big capex coming up. Don’t follow the idea of giving loans to companies when it can be deployed in the capex. Maybe it would be rectified in the coming quarters when the capex program actually begins.

Disclosure: Not Invested. This may change in the next few days.

Thoughts and comments are welcomed. If anybody has any Scuttlebutt Info, that would be more than welcome. This is my first post on the forum, so take kindly to any mistakes