Can anyone explain this please?

Kridhan already acquired 36.6% stake in VNC.

Now they’ve issued 76,79,662 shares of Kridhan to the investors of VNC for 31% stake in VNC.

This means, the total stake of Kridhan in VNC should be 67.6%, right? (36.6 + 31).

Then why does the presentation say 50.5%?

Could you pls explain what does this pattern indicate ?

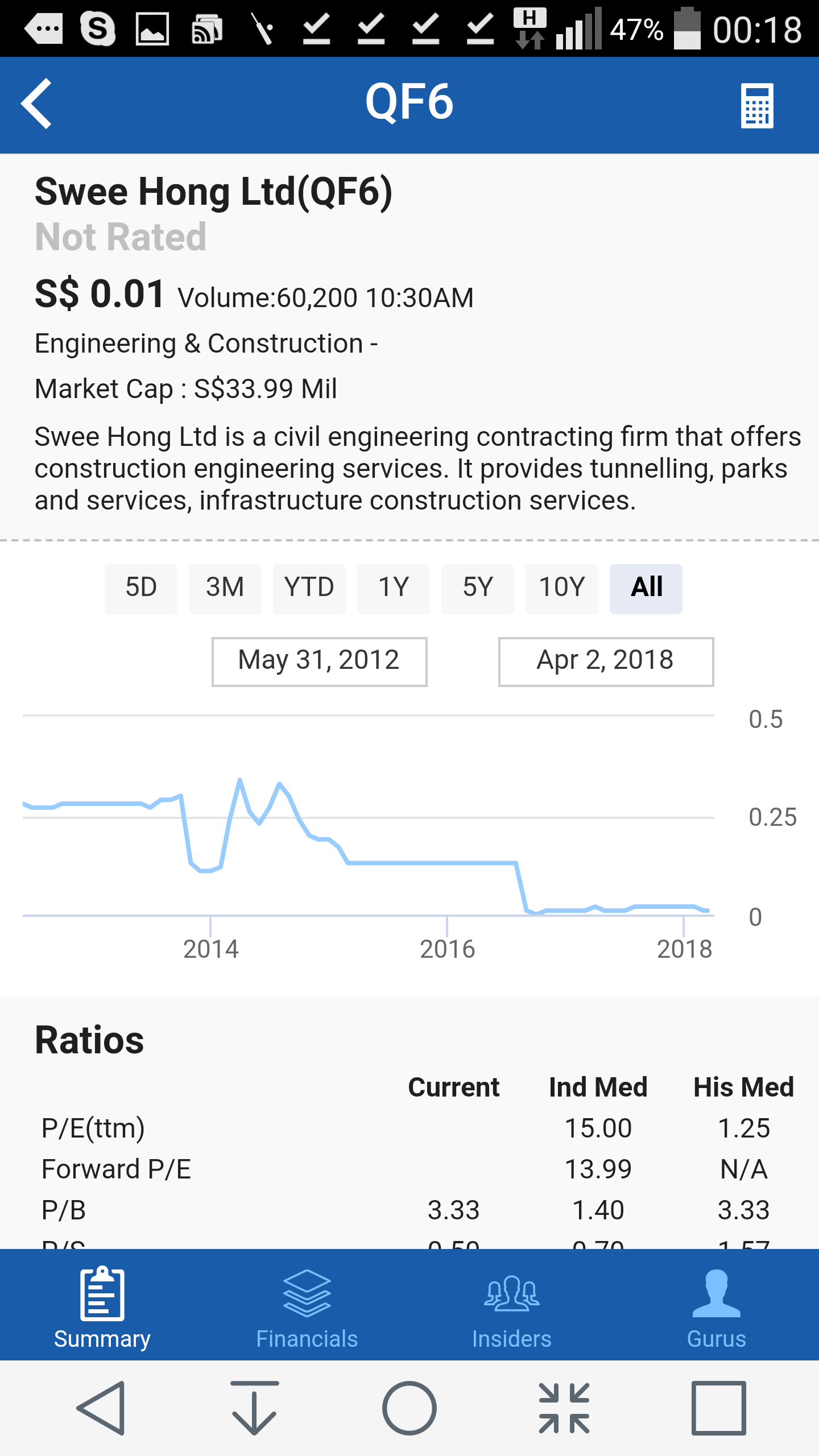

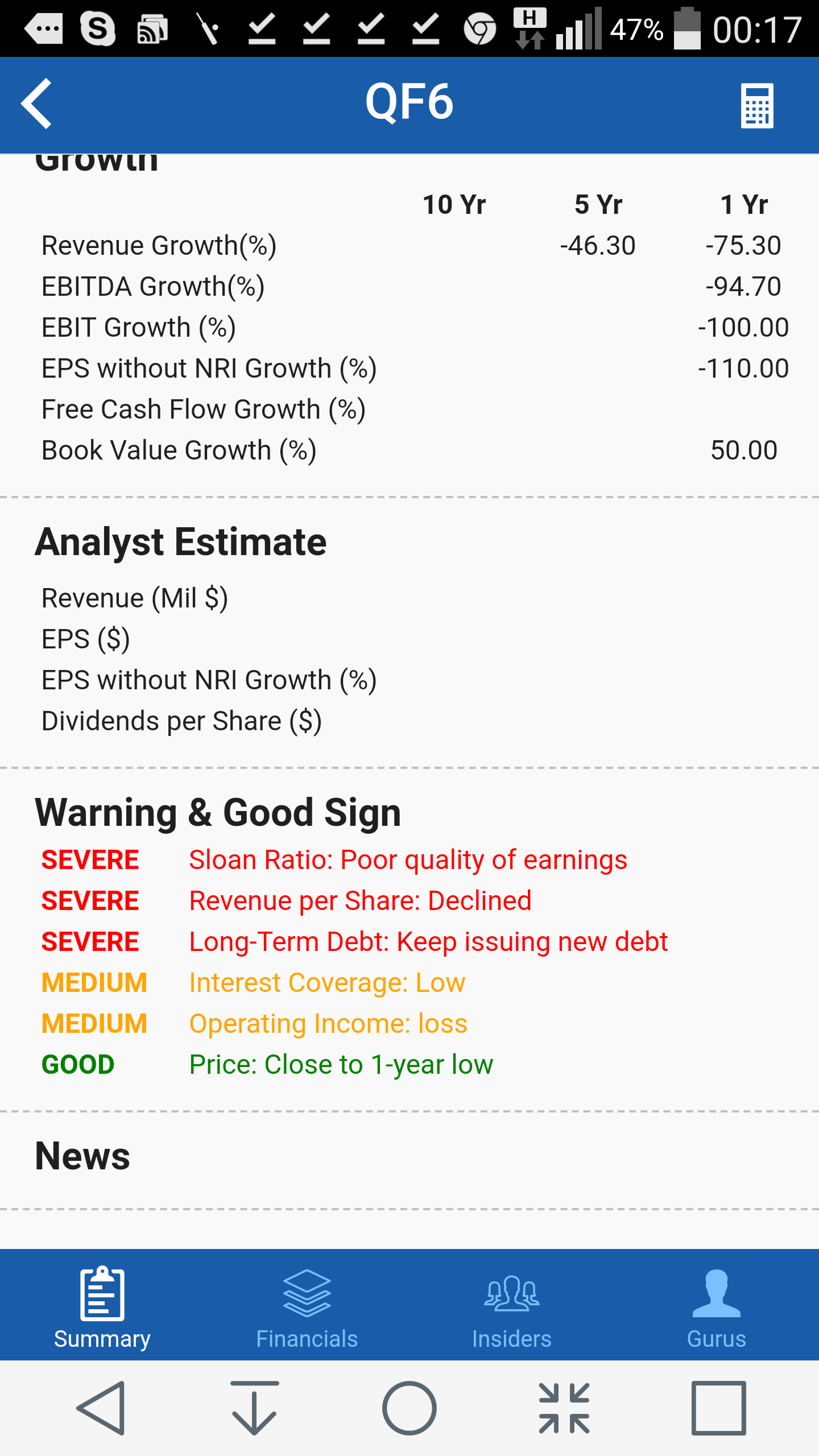

These are the screenshot of the company swee hong in the singapore exchange according to gurufocus app (available for android and ios)

Also it shows sloan ratio which indicates manipulation and poor quality of earnings.

Disc: tracking not invested currently

1 Like

interesting formation of a Bearish Gartley Formation on the recent developments in Kridhan

Kridhan Infra Limited Wins Order worth INR 1,340 million in Singapore. Another big piling contract for its subsidiary KH Foges to be delivered in 4 months time.

March 2018 quarter SHP:

Promoter holding has come down from 51.19% to 47.04% because of the dilution. Promoters still hold the same number of shares as prev quarter - 44583160. Acquarius Capital has got 3160156 shares (3.33%)

DSP and HDFC funds, Singapore govt, Ashish Industrial and comm enterprises, and Satpal Khattar hold the same number of shares. Monetory authority of Singapore added additional 244452 shares.

4 Likes

Bulk deal: Kridhan Infra: Satpal Khattar sold 5.35 lakh shares of the firm at Rs 109.19

2 Likes

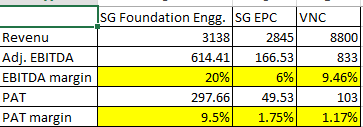

The latest investor presentation provides breakup of SG Foundation engg, SG EPC, and also VNC figures.

Foundation Engineering has the highest EBITDA and PAT margins. SG EPC margins are poor. VNC EBITDA margin looks okay, but PAT margin is terrible (probably huge debt?)

I was invested few month back and came out after LTCG with handsome profit in 3 month (JUST LUCKY;NO TRADING SKILL) because of follwing reasons:

Few management issues:

- History of Mr Anil shows that he does not take responsibility of minority shareholders. Go from RMS days.

- I have invested with view that now he has learned his lesson but check he still try to siphon out money through his wife.

- Two type of promoters are there in Indian market- one who partner with minority shareholder and want their capital to grow the bussiness which they can’t do alone, and other who just want to transfer all the risk of bussiness to minority shareholders- you go through Anil’s history and present condition and decide in which he falls. I was and I am still shareholder of Vakrangee as well as Manpasand. In Vakrangee I have never lost any money because when I was investing I was knowing that promoters are fraud but in Manpasand I got stucked because of credibility of its auditor. But now postfacto I can tell with 100% surety that companies’ auditors are also accomplish in company’s crime. Now you see how full story was cooked by Delloite and Manpasand over 6-8 years that it had not only fooled individual investor but also great fund managers.

- Not having great growth mind set of management- it is my personal opinion after reading and listening the management.

- No depth in management. Dependent on few experienced people.

Bussiness quality:

- It is capital intensive bussiness. However this company was having better ROE & ROCE than other construction company with lesser debt.

- I accept DD Sharma view that size of opportunity is big and risk to reward is in favour of investor. However, in India it is very difficult to compete in this sector without close monitoring, whereas their prime focus is singapore market.

- This work is very routine job and nothing great patented work as touted by Sharmajee. In Bihar itself in past 10 years we have build 1000 or more bridges all with pilling work and soil investigation. Most of the pile were ranging from 30-60 meter. Big companies like L&T use to sqeeze the margin by taking benefit of competition. And many like gammon are having there own piling machine. Simplex is more nimble footed and understand Indian market better than Kridhan.

So only people who can keep close watch on the company and review its performance yearly should invest; Not by listening to DD Sharma😴

It is a risky bet- don’t get blinded in love of multibaggers. Try to understand what Sharmajee is telling- Numbers will come then it will become multibagger. So please evalute the capability of management.

2 Likes

U invest in business where the promoters are fraud?!

Brother dont take out sentences out of context like news editor. It is been written for Vakrangee. You go and check the history of Vakrangee -2011. You will come to know what I mean to say.

Anyway, it is very easy to say that this management is good and this management is bad- postfacto. But honestly and fraudness of management is something which can’t be judged 100% in advance. And this is a big risk associated with all investment. Most of the Indian management are not of high standard in start; however many of them use to become honest when they use to become successful or market use to forgive them or overlook.

help me with the facts when u say, the anil is siphoning money through his wife…

Please go through management salary section in annual report 2017. Now you have to take call because it can be controversial- if his wife is eligible for the job then it is fine; if she is not then only it can be termed as siphoning.

I was not comfortable so I have sold out my full position at around 120 which I have got at 81with profit of 50k.

I like the company at current juncture if it will be able to deliver the promised things. That’s what I have written it is very difficult to predict honesty of any management in advance because “PEOPLE AND SITUATION BOTH USE TO CHANGE WITH TIME.”

Management interview in CNBC

1 Like

@Nolan Have you been following this company over last few months? I can’t understand the reason for price falling… any insights highly appreciated.

Just a time correction for all mid/small stocks. Company has a healthy orderbook and VNC consolidation should help it scale up operations in next 2-3 quarters hopefully.

1 Like

Another pump and dump stock

1 Like

With VNC consolidation, Fy19 guidance is 1800-2000 Cr but the PAT guidance is 75-90 Cr which means PAT margin of ~4-5%. If we were to look at VNC numbers alone, PAT margin for Fy18 is ~1.2%(103/8800). VNC constitutes 80% of Kridhan’s order book, hence further increased pressure on PAT margin going forward. Just confused as to how should this company be valued?

1 Like

Can you please share the source of full year VNC margins? Being a privately held company, I couldn’t find their detailed financials.

VNC financial data was mentioned in the latest investor presentation. Check my last post where I mentioned this.

1 Like