I found it surprising to not to find a thread on this company. It has already been a 10 burger in last two years.So with whatever little information I could gather I am starting a thread.

Krebs Biochemicals & Industries is a 155 Cr company established in 1991, KBIL is headquartered in Hyderabad, India with two manufacturing plants in Nellore and Vizag, India.

Highlights are:

- Undertakes both contract manufacturing for large pharmaceutical and multinational companies as well as product development by KBIL for sale in global markets

- 600 employees across 3 locations

- Certifications include: USFDA, ISO 9001, Indian GMP Approved, EDQM and EUGMP Approved

- Ipca Laboratories took 18.92% stake in Krebs Biochemicals in Feb 2015

- Primary products in market are pain killers, anti-asthmatic(Ephedrine), anti-HIV drugs and Anti-Cholesterols(Simvastatin, Lovastatin)

- Products in pipeline:

- Adenine - Anti Cholesterols

- Atorvastatin - Anti Cholesterols

- Phenylephrine - Anti asthmatic

- Orlistat - Anti obesity

Some open questions on which looking to gather some data points.

- Which are the markets KBRL sells?

- What is the split of revenue among its products?

- How is the prospect/demand of anti-asthmatic and anti-HIV drugs in coming years(assuming these are main sources of revenue)

- Who are its competitor in these products ?

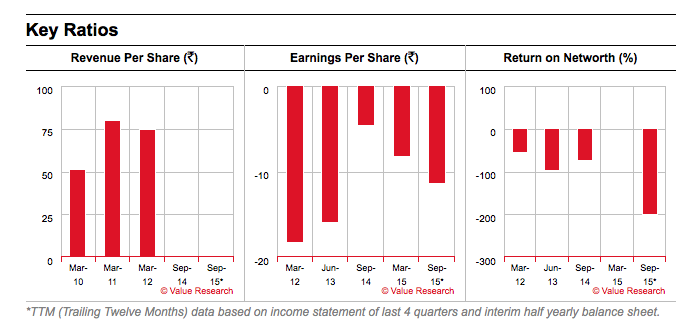

- EPS and ROE are negative, so what makes investors to be so bullish on it ?

Disclosure: Not invested yet

3 Likes

I have been tracking this stock since Oct 15, and have been surprised what is it that’s keeping the price of this stock around the Rs.110 Rs. 120 mark.

If you look at the figures, they have zero sale in the last couple if quaters, yet what warrants the price.

I know they are working on a very niche way to produce certain pharma based products using the process of fermentation, but when will it materialize and by the time it does will it be actually used by any other pharma company as a raw material or directly be used as a product that be sold OTC.

Many unknows, but have some gut feeling that this might be a good stock to stay invested in, especially when the markets are falling (along with the stock price of KREBS)

Some Screener data : https://www.screener.in/company/524518/

I am planning on uptaking some of krebs and accumulate parnax labs.

Cheers

Krebs is coming up with a rights issue however the draft document was not on BSE.

They have 2 products and they are doubling production of both after the rights issue

On their quarterly p&l, I assume the fixed costs like labour wont change much. Material costs will increase and 25cr of new additions will be depreciated over 20 years giving a monthly additional depreciation expense of 1.25cr

The new expansions are going live in June 2019

They are also developing 2 products, one of which is to target obesity which commands quite a high premium

In the attached most of the calculations for the 25cr are from page 58 onwards

On page 18, there is clause 23, which says they have insured their plant and assets at 581 crore on basis of replacement value. If this is true than the current market cap is a huge discount. The 581 crore assets eventually should generate much more revenue and profit

http://www.krebsbiochem.com/documents/6307bb64dd77f34859e2f40b1bec2977.pdf

I am aware this is a an old topic, probably this time everything will go right for Krebs !

disclosure: invested 1pc of my portfolio recently

1 Like

This company is into enzymes and fermentation… Is this a reason why IPCA and Sun Pharma have such a huge ownership in this loss making firm.

Experts from Pharma… Please guide me.

Management statement from AK Jain…

“And apart from that, we have Krebs as another associate where

some kind of fermentations and some synthetic products are there. That company currently

is in losses, but hopefully, we should turn it around in the next financial year.”

4 Likes

Hi members

I saw very little discussion on this scrip.

The stock has has gained momentum after 22 MD July.

As per media

Krebs Biochemical fermentation plants are expected to break even towards the end of this fiscal.

Please share updates if any.

Thanks

Sajal Kapoor has talked about this scrip in one of his videos with soic. I Did some research here. Looked promising but I had so many questions that I couldn’t find answers to, due to lack of availability of information and my own limitations in knowledge. Let me know if you find something

3 Likes

Corporate Governance issues highlighted in this article

4 Likes

Hi, is someone still tracking this company? If so, why has the stock been hitting circuits for consecutive?

1 Like

Hi, thanks for the update, but are they not trying to obtain majority through open offer at far lower price than current market price? How will they be able to actually restructure?

1 Like