Thanks for this post. Meaningful data based analysis like this adds value to the thread.

I have a different way to interpret the calculations, however.

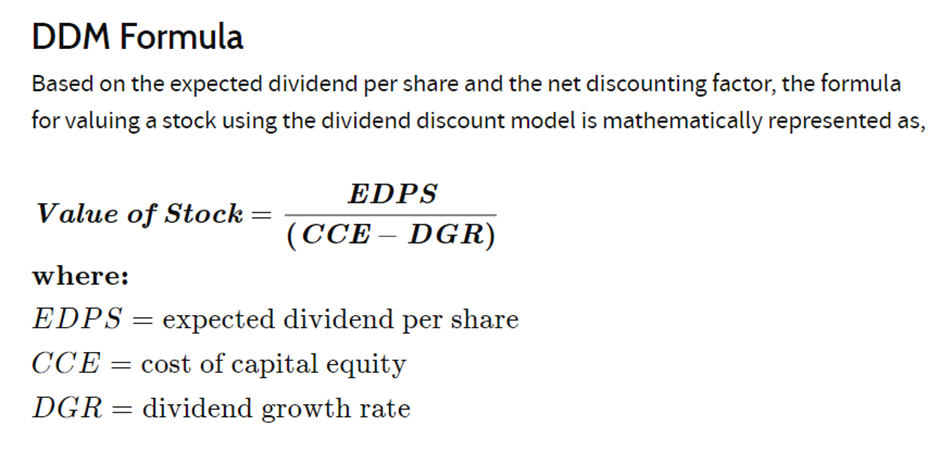

Dividend Discount Model says that the present-day price of a stock is worth the sum of all of its future dividend payments discounted back to their present value. From Investopedia,

In your case, you have taken the current price of the stock, the current dividend per share, assumed a dividend growth rate and worked backwards to calculate the Cost Of Capital. And this comes to 29.64%. If you invert the formula, the interpretation changes because the Discount Rate and the Cost of Capital are conceptually not the same, even though arithmetically they perform the same function.

Discount Rate is the rate at which future cash flows (i.e. dividends) are discounted to their present value. Cost of Capital is the minimum rate of return the shareholders expect for investing in the stock. Normally, it is arrived at as the Risk Free Rate plus an Equity Risk Premium. In the Indian context, one would take the Risk Free Rate to be around 6 – 8 % and Equity Risk Premium at say 5 %, giving a Cost of Capital of 10 – 15 %. In your case, this value comes to 29 %, which means an Equity Risk Premium of more than 20 %.

I would therefore interpret the whole calculation to mean that the equity investors are demanding a risk premium of 20+ % for investing in the stock. This is extremely high but also logical given the controversies surrounding the stock.

(Disc: No positions)