A quick DCF (Discounted Cash flow) analysis on KRBL stock

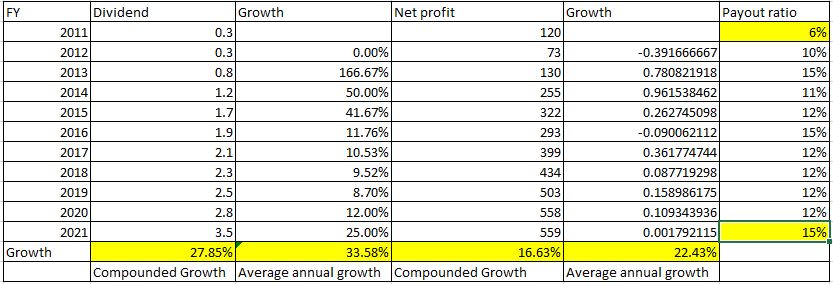

This is the data table for the past 10 years

.

Dividend in INR per share, and Net profit in Crores of INR

.

.

Range of Price in 2011 was 12.65 (low on 22nd December) and 41.35 (high on 6th Jan)

Growth rate of dividend from 2011 to 2021 was a CAGR 27.85%

Based on this the expected Dividend in FY 22 should be around Rs 3.50 * 1.2785 = Rs 4.474750

Let’s compute the implied expected return to shareholder at the current price of around 250 Rs.

Expected return on equity using the dividend discount model

eR = expected dividend next year/ current share price + growth rate

eR = Rs 4.47/ Rs 250 + 27.85%

eR = 0.01788 + 0.27850

eR = 0.29638

eR = 29.64 %

Meaning shareholders can expected 29.64% CAGR returns at the current market price if the historical growth continues.

For 10 years it means = 1.296410^10 = 13.4067 times the price

If we try to use this number to find the historical price 10 years ago, then

Price 10 year ago = 250 / 13.4067 = 18.65

The share price indeed was Rs 18.65 as we saw the range was between 12.65 and 41.35

Mismatch between Profit growth vs dividend growth, A reason to worry?

As we can see in the chart that dividend has grown at faster rate than the growth of profits.

This can be reflected in the Dividend pay-out ratio as well. Which has grown from 6% to 15%.

Do we have a scope for similar 29.64% CAGR returns in the next 10 years?

Answer) Yes!

Even if 15%/ 16% growth in profit continues, then increasing in dividend pay-out ratio to 30% (which is a reasonable estimate) would enable the company to be able to deliver such returns.

Such a return would mean 13.4 Times the investment in 10 years.

Drawbacks:

-

Use of Historical growth rates to estimate future growth rates,

It is possible that the growth may not actually be realised, leading to lower expected return or fall in fair value of share -

the data selected has been from 2011 from where we see the growth happening,

If we check older data from 2003 the dividend fluctuated between 0.10, 0.20 and 0.30

Only after 2011 we see a pickup in growth of dividend. -

This research does not consider the ongoing problems relating to Augusta Westland case, and perception of poor corporate governance due to this case.

These factors may have negative impact on the expected returns or the share price.

Disclosure: KRBL forms a small portion of my Portfolio,

have not bought any stock recently (past 3 months)

.

Data based on closing price of 10th December 2021 (Friday)

Current share price = Rs 246.65

Market Capitalization = 5,805.89 Crores

P/E ratio = 10.33

P/B ratio = 1.50

Would be happy to hear Views and opinions for this!