This is my first post to this forum. I would like to get some inputs from the experts on KPR mills.

Please have a look on the following data. I am currently holding 10% of portfolio with kpr mills as no loss no gain and invested in since last year. Query should I stay invested or exit.

KPR mills:

KPR Mill Ltd. is an apparel manufacturing company engaged in the production of yarn, knitted fabric and readymade garments. It has one of the largest vertically integrated manufacturing capacities in India, enabling the company to utilize and customize the products as per client specifications. Building on its maiden business in 1984, the company currently has 0.35 Mn spindles to produce 90,000 MT of yarn per annum, knitting facility to produce 27,000 MT per annum and garmenting facility to produce 95 Mn pieces per annum (one of the largest garment manufacturers in India). The power requirements are met through the company owned 66 wind mills and through green power through a Co-gen Cum Sugar Factory with capacity of 30 MW and 5000 Tons Crushed per Day (TCD). The board, including Chairman Mr. K.P. Ramasamy and Mr. K.P.D. Sigamani, the Managing Director, has vast experience in the textile industry, which has aided in the company’s evolution into fabric and garment segments.

Vertically integrated operations

KPR has one of the largest vertically integrated manufacturing capacities in India, producing superior readymade apparels, fabrics and various types of value added yarn. Vertical integration has helped the company diversify the business and move up the value chain (into fabric and garments) along with maintaining cost benefits. As of Q1FY18, nearly 44% yarn and 29% of fabric are used for captive consumption in the manufacturing of value added products such as fabric and knitted garments.

Risk Analysis

Volatility in cotton prices, Raw material price fluctuation

Forex volatility

Change in government policies (international and domestic)

Slower than expected ramp up in the garment business

Holding Disclosure: I am currently holding 10% of portfolio with kpr mills at no loss no gain and invested in since last year. Query, should I stay invested or exit?

The management appears to be careful while deploying capital.

They are setting up a garment manufacturing unit in Ethiopia. The land- building is being provided by the local govt. on lease basis. The investment will be only on machinery. They plan to invest Rs.30 cr. There are tax benefits associated with exporting from Ethiopia and labour is cheap. The fabric will be supplied from the Indian plant.

I think this is a good strategy.

2.They are studying the benefits of launching their own garment brand. This is taking quite a time. Either the management is lazy or else they are making sure that nothing goes wrong when they launch their brand.

Nearly 40% of the revenue comes from export. Depreciating Rs. will be helpful.

Garment manufacturing capacity is huge and as the capacity utilisation improves , so will the EBITDA.

Disc : Invested

*Plan to start wholly owned subsidiary in Ethiopia @ subsidy by Ethipian govt.

*Plan to start innerwear segment

*Expect growth from present year since environment has turned favourable from the beginning of 2018.

*Reduction in debt compared to previous year.

*Investment in Reliance mutual fund.

As mentioned in their latest concall , it is certain that they are fraying into men’s undergarment segment. They will have their own brand besides having a tie up with some already established brand. They mentioned that it will be an asset light business with no heavy capex. Already existing capacities are enough to cater to this new line of business.

Gradually they are ramping up production of value added yarns to enhance margins.

Ethiopia business is expected to have an overall 10 % points better margin.

All in all , if the branded undergarment business does well the stock can easily be a multi bagger.

Thanks

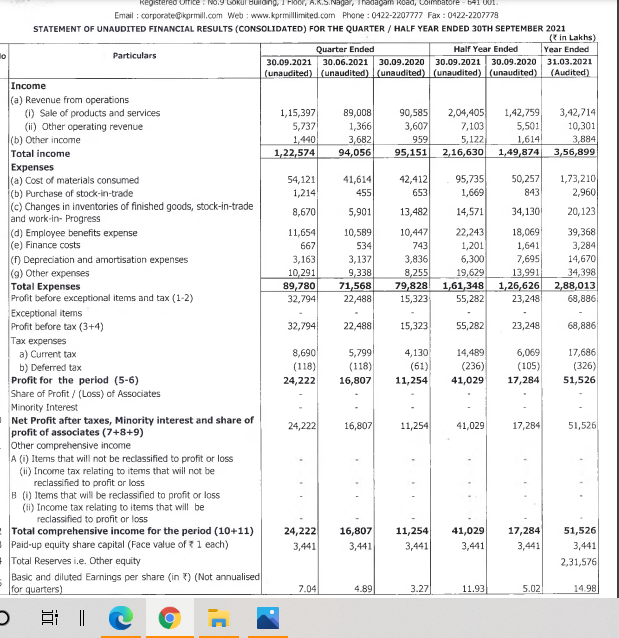

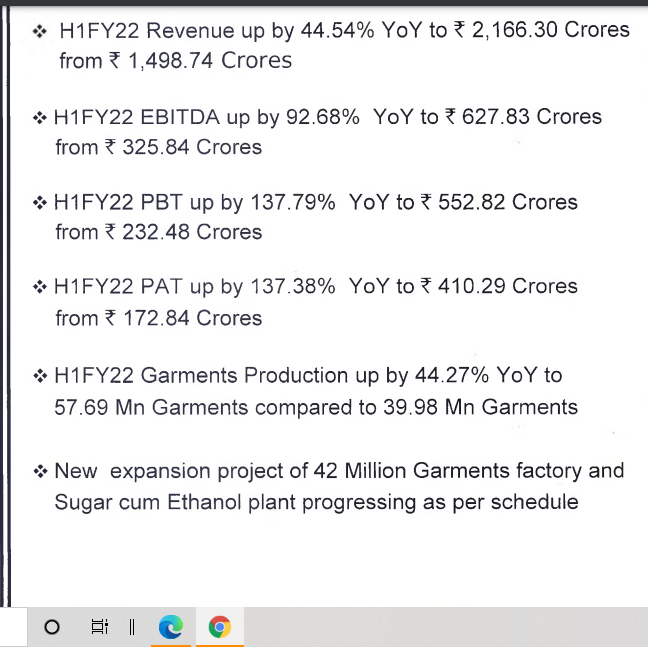

The company has posted decent results but the share prices reacted in a very negative way. Can anyone share their views on the future prospects of the company.

Textiles division took a hit in profitability as per the segmental results. Topline was as expected but I think lack of MEIS subsidy probably took a toll on profits. Or it could be higher raw material prices but with changes in stock inventories of finished goods and stock in trade its difficult to make out.

Sugar division seems to be back on track and with the new ethanol capacity is less likely to witness too much cyclicality.

Lower taxes helped the net profit figures especially in the consolidated numbers. Notes with results does not mention the proportion of revenues from garments for the quarter.

The top notes mentioned that garment production was up 10% and they have also started a new line of men’s undergarments in Southern India. The structural story is intact and they are performing as per expectations. The fall seems to be overdone, can we buy this panic dip?

hi @hitesh2710 bhai, whats your strategy here now? would you suggest waiting on this for another quarter or trimming position now? Technically the expected breakout did not happen ?

I came to know about KPR in April, but got no clarity, do they have their own brand now? how is their B2B ? any brand they work with? all i got from their website is they produce cloths.

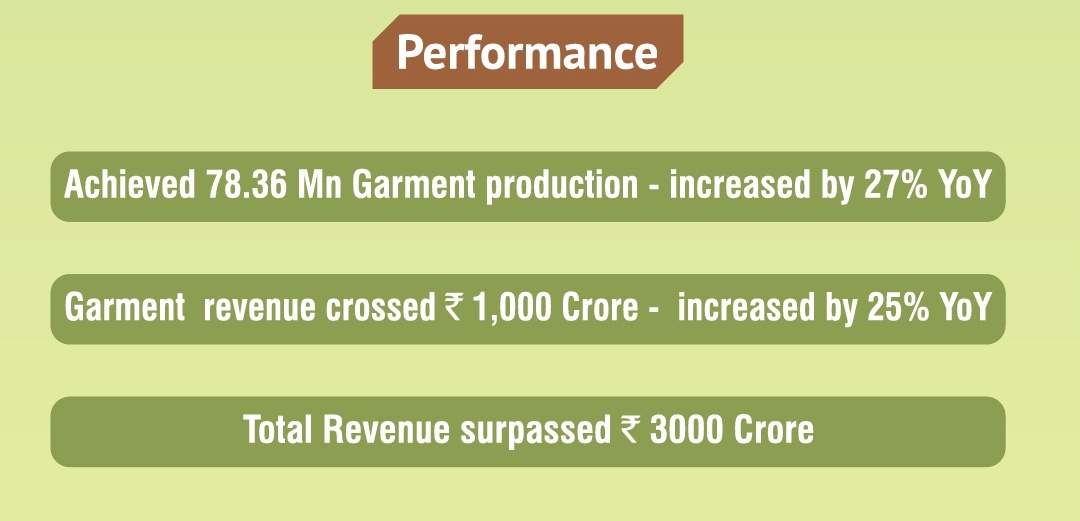

Go through their investors presentation from February from the nse website. Very under the radar company so the only info you’ll get is from the quarter reports. I’m considering investing due to their amazing vertical integration… very rare to see a company so independent on outside factors. They produce their own electricity and power. which they use to run their own factories and spinning machines to produce yarn and garments to sell across India and abroad. which they also now use to make their own final product (the Faso brand for innerwear). Overall they have set up a beautiful self sufficient business model and hence I consider them a safe long term bet with huge runway now that they have delved into retail. If I do invest it will be for the looooong term though. Expect headwinds due to lower demand due to Corona + they have been increasing their exports abroad the past few years(used to be 60-40 domestic Vs abroad but is now 58-42) so things may be slow there too + their jump into retail with Faso may take a while to gain traction and market share. However, the business model is so good that I’m probably going to start an SIP on Monday. Still Undervalued at present and I can see it being a giant over the next decade. As a bonus they’ve managed to reduce the cyclicality of returns in sugar too. Just fyi… their revenues right now are nearly 3400 crore a year at present and it’s MCAP is still just 3500. Just for reference Page industries(not a direct competitor yet but considering their move to retail and their low costs involved due to backward integration for the same I can see them being one in the future) makes approx 3900 crores per year are present ie just 500 more. And look at the MCAP difference.

Results are out today… and imo they are ok. Revenue and profit for Q4 is lower as expected however overall they’ve still managed a profit increase from 334 to 376 crores overal from FY19 to FY20. What I’m struggling to find is figures on how Faso is doing and commentary on how they’ll be handling the next few quarters? Does anyone have the con call transcript if any? Is there anyone here still invested in KPR mills to discuss the results with? Cheers

Good news is FASO is available on big online platoforms (Flipkart, Amazon, Myntra etc) but not so good news is high pricing. They are even higher than jockey!! I don’t know why people would even give them a try.

Although the company has decent fundamentals and some of the industry best HR practices (sponsoring higher education for employees, teaching roller skates to traverse the shop floor), the numbers don’t add up to exhibit long term sustainability in earnings.

Looking deeper into margins, it comes to notice that bulk of the company’s OP is contributed by export incentives. These incentives all come from export of garments only, since yarn and fabric are domestically sold, and as garments have been growing significantly, export incentives become even more important –

Particulars

2013

2014

2015

2016

2017

2018

2019

2020

Textile OP

236

266

283

317

413

434

481

484

of which

Export Incentives

28

44

58

67

91

99

92

115

Investment Subsidy

0

24

16.8

17.7

20

9.5

0.8

0

Export Inc. % of Tex. OP

12%

17%

20%

21%

22%

23%

19%

24%

( investment subsidy has not been considered since it’s a part of Other Income)

OPM

15%

13%

13%

14%

16%

15%

15%

14%

Garment OPM

16%

14%

14%

15%

17%

16%

16%

15%

Garment OP

39

52

71

89

118

140

190

193

Export Inc. % of Garment Exp.

71%

85%

82%

75%

77%

71%

48%

60%

Exp. % of Sales

23%

25%

33%

37%

38%

40%

43%

42%

One could argue that the export incentives are priced into the contract while accepting purchase orders at a specific quote. If that is the case, its very difficult to determine KPR Mills competitiveness to firms in Bangladesh and China, especially since despite the INR depreciating against the USD, KPRs realization per garment has reduced over the years, and has not yet crossed 2016 high -