Although results are good, company decided not to provide guidance for FY 26. This unnerved the market IMHO

2 Likes

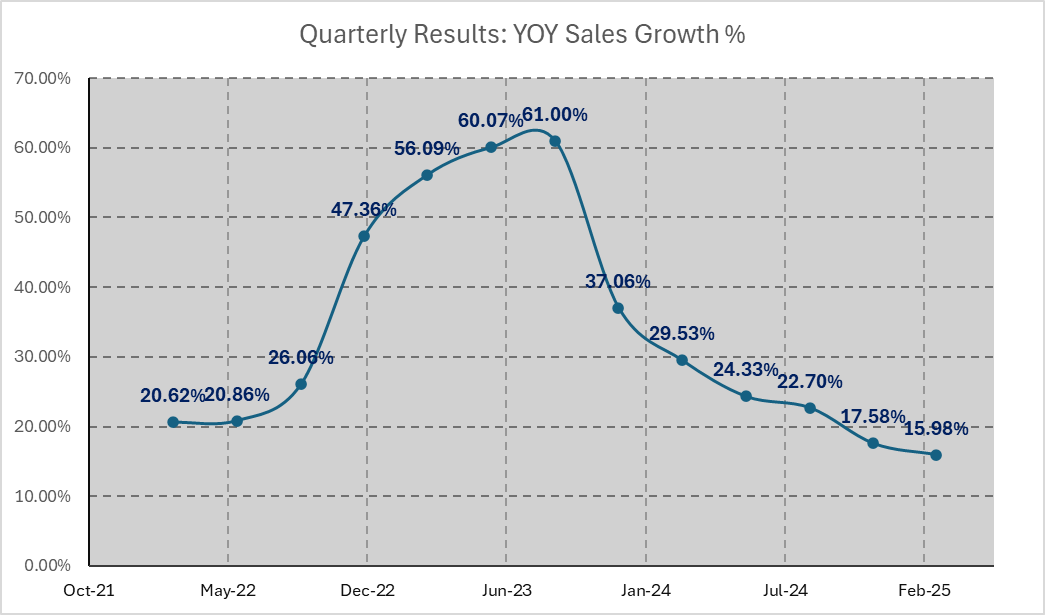

I think lack of material price movement today is also due to the fact that their YOY sales growth has been weakest this quarter with overall sales somewhat tapering off since last few quarters likely due to a). high base & b). global macroeconomic factors. It appears the current earning growth trajectory is well priced in with limited upside impetus in short term.

2 Likes

No @apoosh both yoy and qoq looks good for me ?

Below graph shows their quarterly sales growth compared YOY, tapering to some extents in recent quarters. Their sales is still significantly better than other ERD players and their profit growth is still robust, slowing sales growth may have put pressure on their PE which had been north of 50 for more than 3 years.

Disc: invested

9 Likes

Nice data illustration,got it. thank you..

Which website provides this data? Could you please point me?

1 Like

@GrowthValueInvester data is sourced from Screener and plotted simply on excel.

Would just like to emphasize that revenue growth looks optically slow in recent quarters due to high base effect (owing to bumper results in FY23-24), but still head and shoulders above the likes of Tata Elxsi, Tata Tech or LTTS. Plus they demonstrated significant uptick in profitability and efficiency ratios. However, given the global macro headwinds specially in European Auto sector, market needs new triggers in order to sustain their high PE going forward, in my humble opinion.

9 Likes

Considering the fact that they mentioned in their earnings call, that they are getting good learnings from their china operations which is helping them learn to make their services more cost efficient and cheaper and to provide them to their Europe and USA OEM clients. They also mentioned about entering and getting new clients in Off highway market. So are these triggers not good enough to probably help them get higher revenues possibly in the upcoming quarters.

5 Likes

Good Management commentary! Management said they are closing monitoring the situation in China and would be ready to onboard a Chinese OEM as they can help it do localisation and enter new markets.

Disc - Invested and bias. Have made no transactions in last one year.

4 Likes

Very good company…current results are head and shoulders above the rest of ER&D players…management focused on asia and usa once they realised there is slowdown in europe and showed growth in both these geographies…they also said they will learn from chinese oems what needs to be done forward…overall great management, great results!

4 Likes

I wish I had attended the concall.

I would have loved to ask them regarding their inroads into Chinese OEMs, "How much of scope they would have, given how advanced Chinese OEMs already are in the EV space. What do they do at present? What kind of an ecosystem and current players do they have in China for the offerings KPIT has?

Anyone having insights into this, please share! ![]()

You can still ask them, KPIT has a great investor relations team. You can send a mail to sunil.r@kpit.com

1 Like

Thank you for the nudge.

I shall share the response to the questions I asked

"How much of scope do you see, given how advanced Chinese OEMs already are in the EV space. What do Chinese OEMs currently do regarding all the areas we focus on, at present? What kind of an ecosystem and current players do they have in China for the offerings KPIT has? Do you hope to replace Chinese or other service providers or are our offerings unique in that regard?

"

2 Likes

Received any response from Kpit plz share

No, I didn’t. I sent them a chaser yesterday.

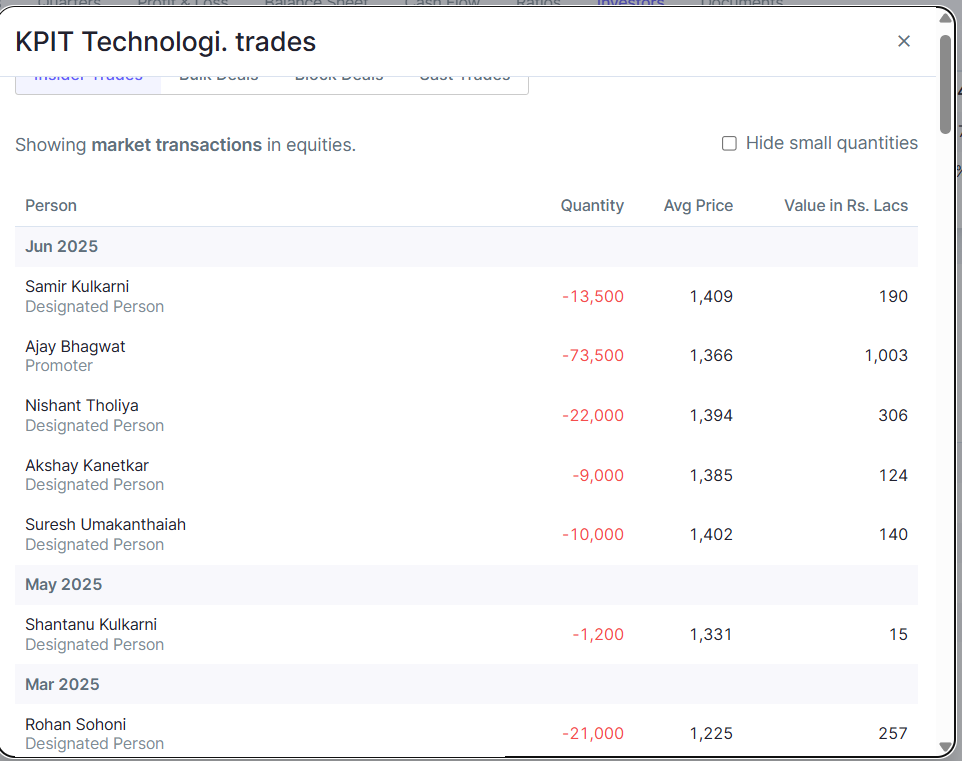

Company came out with mid quarter update on 23rd June, which disappointed the market and share price dropped from 1400+ to 1270. But some of its key employees sold lot of shares just before the announcement. Clearly they knew about it and decided to sell their shares before bad news becomes public.

KPIT always took pride in its corporate governance practices and this event puts question mark over that. I have lodged complaint on Scores and planning to write to company also about it. I hope its a one off and would not get repeated in the future

9 Likes

I would also like to do the same. Follow up on scores..

Yesterday I had written to Mr. Sunil Phansalkar who handled investor relations for KPIT about sale by Mr. Nishant Tholiya… today I found exchange notification that Mr. Phansalkar himself sold 43% of his holding on 23rd June…No wonder I did not get any response to my email yet

Highly disappointed by behaviour of company executives

Disclosure - Part of core PF. Held for last 4+ years. Purchased more shares during the week.

2 Likes

To the standards of corporate governance indian companies follow, IMO these type of things shouldn’t even raise eyebrows…

1 Like