BYD is a big concern for all Auto and auto component manufacturing in India and worldwide. Without strong tariff bariers their tech is so advanced that 90% of auto manufacturers will perish. Can other countries catch up, maybe but it will take 10-15 years to catch up.

6 Likes

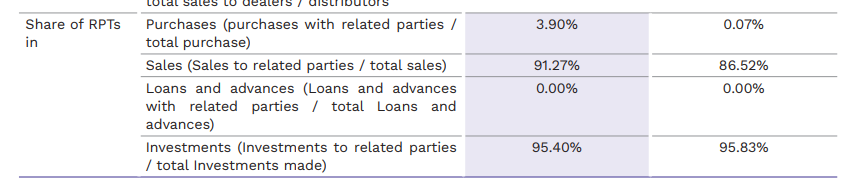

I was reading the FY24 Annual Report for KPIT Technologies and found this. Can anyone explain me why such high % of related party sales are being done here. Is this a red flag in this company?

It might be for subsidiaries, you won’t find many red flags in companies with such Mcap as they are being watched by everyone.

All the Sales transactions are with their subsidiaries based in UK, USA, South Korea, Germany, etc.

100% holding of KPIT in all except 2 which are Joint Ventures.

Besides so much pessimism from the market KPIT may surprise the street with their growth trajectory and better results in Q4.

1 Like

Agree @murali603 but what is the trigger? Let me give you my pov.

Stock is down 32% from pick. Available at PE of 47. Tata Tech and LTTS, though their growth forcast is low it available around 40 PE. Morgan S etc estimate good EPS and revenue growth for KPIT.

It seems market is not giving any weightage of Germany and EU’s “whatever it takes moment”. Germany, led by new leader Friedrich Merz, is planning a €500 billion special fund for infrastructure and defense spending and same is for many EU nation. Due to this german stock index DAX is 20% up and nearly at pick. Same with other EU nation’s stock market.

KPIT’s 50% revenue comes from EU while 20% from USA and remaining India and ROW. EU’s revivle is the revival is the trigger as per me.

Disc: Largest weight my PF. Added between 1200-1300 recently. Holding and views are biased.

9 Likes

When competition intensifies then OEMs will work on cost controls, KPIT take up such projects on cost controls by optimizing the things and give benefit to the OEM’s. Same was explained by the management in the last call.

I am also much convinced with the way things work in the auto industry, OEM’s won’t stop R&D spends rather they will increase the spends to decrease the cost of the vehicle.

As KPIT is adding 2 more new verticals in addition to the PV, it will boost the growth going forwards. I am expecting KPIT to outperform industry with >25% growth.

For me also its one of top holding in PF, I am in since 2022 and added some more qty at the current levels.

4 Likes

Is KPIT the worst contender for new tariffs, being an IT firm having some contribution auto sector as well.

Today KPIT is 7% down due to US reciprocal tariff. To everyone please put your views on the same, will it affect more? As 20-30% KPIT US business will slow down due to additional tariff

1 Like

According to me there is no tariff on software.. I feel this is due to structural issues like Slow down in Europe OEM’s,AI impact and US recession fears..

I may be wrong! this my view

1 Like

IT in general might go through a downcycle because of the recession fear US and maybe a slowdown in projects. While the business may not get impacted as much as the market is reacting a PE rerating can push the stock down further.

Disc: Invested and confused

6 Likes

Adding to that KPIT works in niche space compared to plain vanilla SW companies

But when whole US market will face a downside, obviously they will try to cut down on unnecessary cost which can affect software industry.

with my Vague memory they have 30% revenue from US..Just think how much it will be affected and company has to take alternate measure if it affects

Biased Invested and Working in same automotive domain.

2 Likes

I think we have to take a more holistic here. Since US has imposed tariffs on AUTO, it has a direct impact on cars from EU being sold in the US. Not only that, this tariff war will lead to a global slowdown as all the economies are affected in some way or the other. Demand for cars will fall and hence companies could be tight on budget and will not be left with much option but to cut back on R&D as well.

Unless there is a change in the current stance taken by Mr Trump, there is a lot of uncertainty at the moment. That is exactly what is reflected in the price right now. But since he is so unpredictable we don’t know the true impact yet as he could change things overnight.

Watching closely and tempted to enter again as soon as there is a little more clarity.

3 Likes

True, the current valuation is quite tempting, but on a macro level, things aren’t aligning well which could potentially impact profitability, revenue growth, and margins.

US President Donald Trump is considering to temporarily halt the auto tariffs he had imposed earlier on the sector.

This will indirectly benefits KPIT as well.

2 Likes

This stock has been bitten down on tariffs news only. So any kind of relaxation on auto sector can fire the stock and aided by short covering, the stock can test ATH.

3 Likes

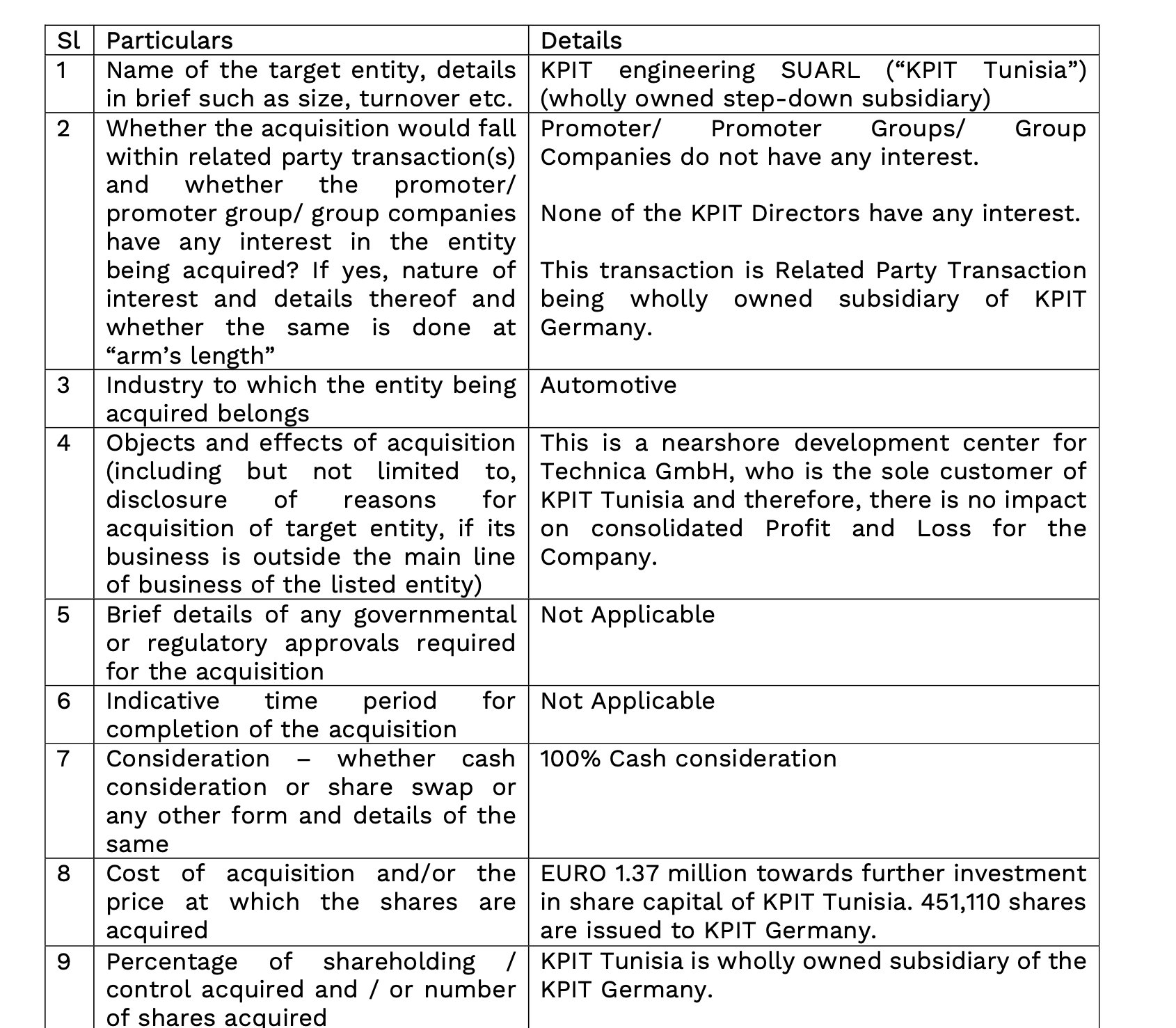

Hi, the company recently announced that they are investing about 1.37 Million Euros in the Tunisia subsidiary through KPIT Germany.

The announcement mentions that the sole client of KPIT Tunisia is Technica GmbH. But Technica GmbH was fully acquired by KPIT about an year ago. So, why not invest directly into Technica? What kind of agreement is there between KPIT Tunisia and Technica? Any info?

2 Likes