News on ET Markets on 10th July

Describing engineering services companies specializing in automotive and software services as billion-dollar specialists, global brokerage Bernstein has initiated coverage on four players, including Persistent Systems and KPIT, with up to 30% potential upside.

Bernstein has an outperform rating for both stocks, setting a target price of Rs 5,920 for Persistent Systems, reflecting a 30% upside scope, and Rs 2,120 for KPIT, indicating a 25% upside potential.

“We believe ‘specialist’ engineering services focused on software and auto have a long headroom of growth. They have built differentiated IP, partnered with global innovators (e.g., Microsoft, Tesla), and have built strong sales and management capability,” Bernstein said in a report.

Here is Bernstein’s view on the companies:

Persistent Systems Persistent specialises in software services (90%+) collaborating with major clients such as Microsoft and Salesforce. It demonstrates strong growth leadership with a compound annual growth rate (CAGR) exceeding 20% and expanded profit margins.The company has a leadership in software product engineering (45% of revenue), and technology-led offering (cloud, AI, Salesforce), a strong management team, and a deep client base with an ability to win cost take-out deals.

Bernstein states that the company has been the fastest growing in IT services over the last 3 years (+30% CAGR), with its margins expanding from 12% in FY21 to 14.5% in FY24.

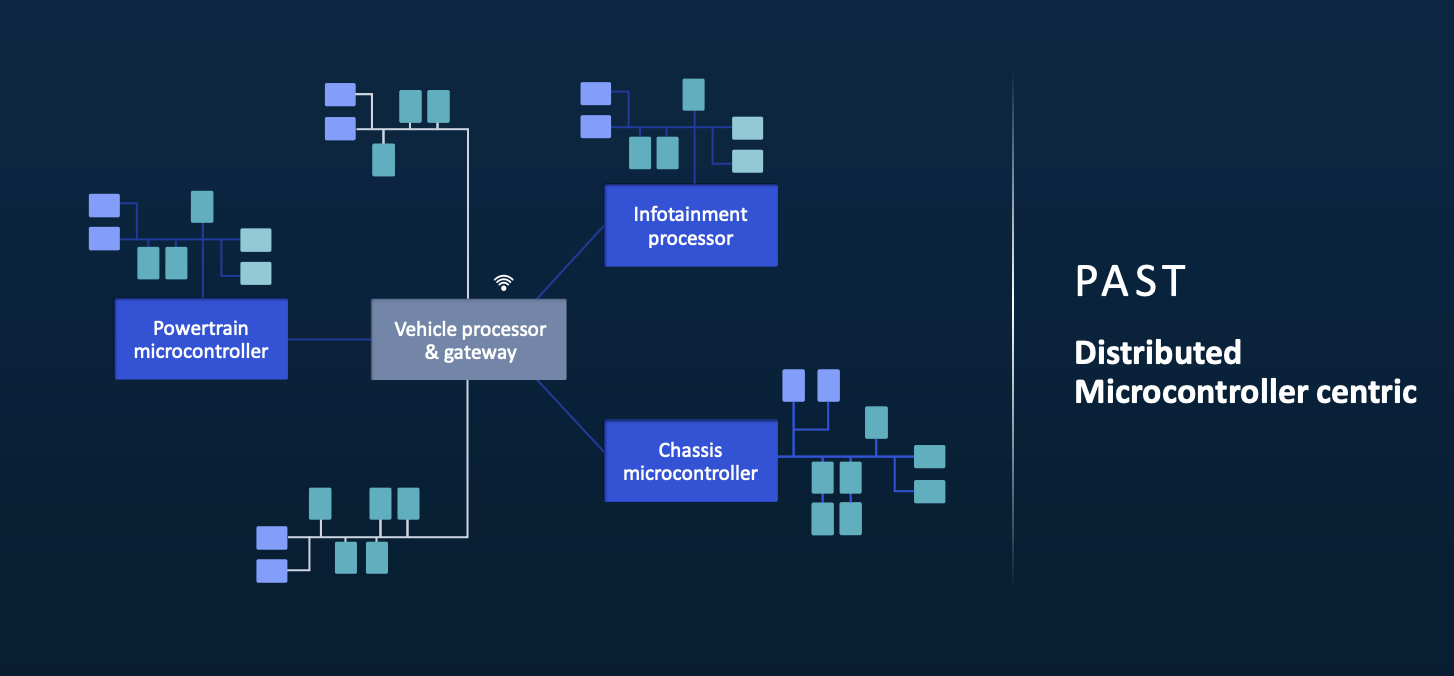

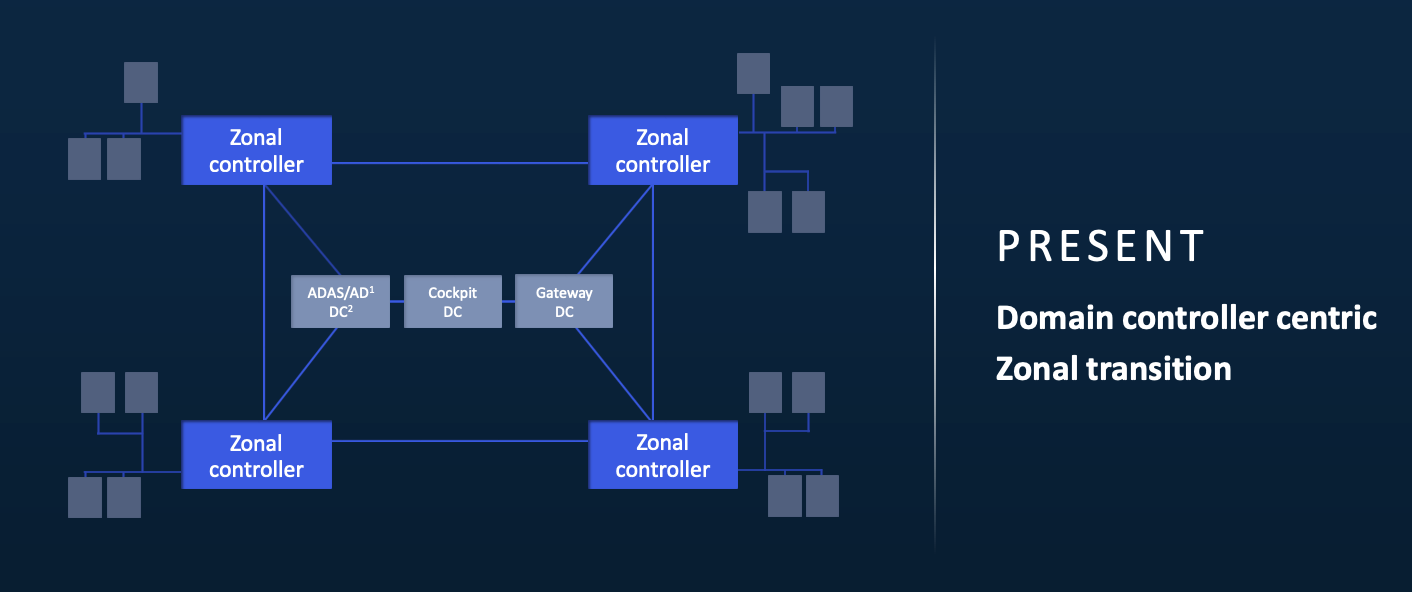

KPIT Technologies -Since its IPO in April 2019, KPIT has emerged as a dominant player in automotive services, achieving a growth rate of 50% CAGR. The company specializes in electrification, Advanced Driver Assistance Systems (ADAS), and body electronics, catering to major OEMs and tier suppliers such as BMW, GM, and Cummins.

KPIT has outperformed ER&D peers with its deep engagement with auto OEMs/Tier 1 (96% of revenue). ER&D intensity from auto OEMs has expanded from 3.6% to 4.5% led by acceleration in auto OEM investments across electric, autonomous, and electric vehicles.

The company’s EBITDA margins are stable at 20.5% and demonstrate pricing power.

Coforge and Tata Elxsi Coforge is a traditional IT services company with a focus on BFSI (55% share) and Bernstein expects larger IT services companies to be better positioned in traditional services and to gain market share over time. The recent acquisition of the testing company.

The recent acquisition of Cigniti is likely to see headwinds due to AI disruption. With this, the global brokerage firm has a market-perform rating for the stock with a target price of Rs 6,080.

Tata Elxsi has delivered the slowest growth among engineering peers, with a 17.1% revenue CAGR over the last 5 years. Revenue concentration is a key risk, with the top 5 clients accounting for 44% of revenue. Additionally, the stock appears expensive, trading at 50 times earnings (P/E), amid slowing growth momentum.