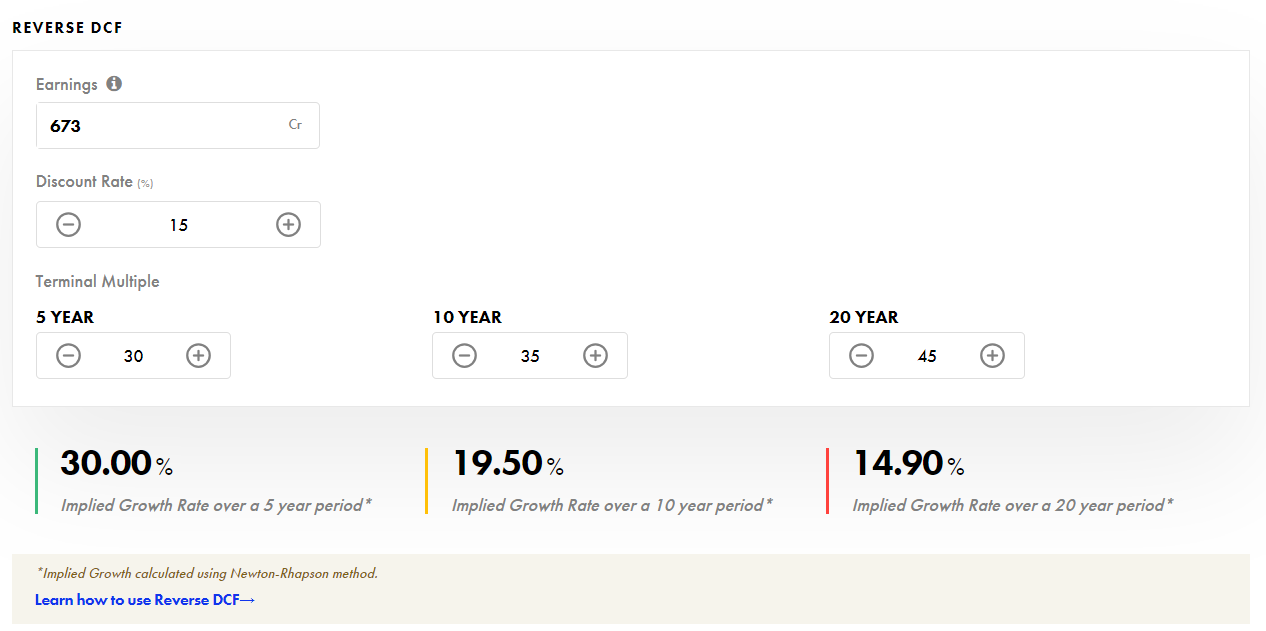

Seems like it is overvalued… very expensive at the moment. The Reverse DCF indicates the market expectations and whether it is realistic.

1 Like

You are right but I have often seen market ready to pay the premium till the company has tailwinds and performs good. KPIT has been delivering consistently good results which is why it still remains expensive.

Any update on KPIT guidance in Q3FY24? is there any change?

@Ameya_Vaidya KPIT provides annual guidance, so expect it in Q4.

Gone through concall, they indicated that current yr is exceptional, so I believe Fy 24-25 revenue guidance may be slightly lower. I believe they have many upwards levers for margin, so if they lower revenue guidance than possible they increase margin guidance. My sense is that they can increase margin comfortably, which is dragged down by future investment.

Said so all the speculation as per my studies. I know few who sold KPIT in past due to valuation, which they thought will enter later, which was not possible for them. So for me it make sense to hold. Also when we got appro 40% revenue growth for non-cyclical company it won’t possible to cruble down the growth, growth may come down gradually if so.

Disc: Invested and my views are biased.

4 Likes

It seems very good stock from its business and management perspective. Adding on huge dips seems decent bet.

Disclosure, invested and biased.

PM Modi launched first hydrogen powered ferry, hydrogen fuel cells were made by KPIT. KPIT is working on tech like Sodium ion EV batteries and hydrogen fuel cell which it can possibly license in future.

6 Likes

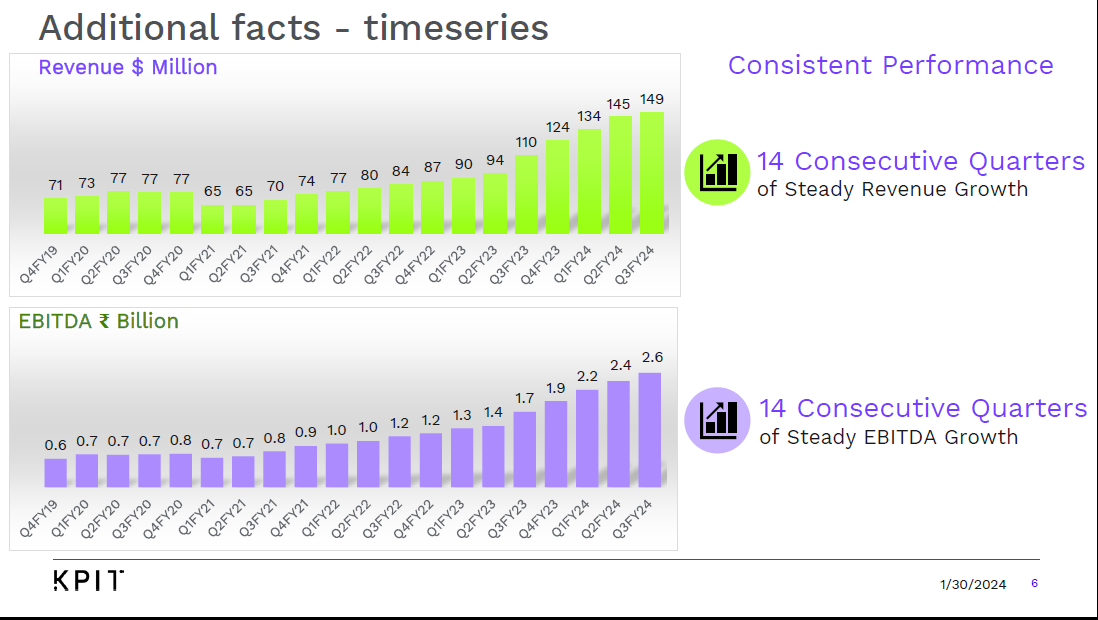

Another solid set of results with continuing strong guidance

Results

Investor presentation

5 Likes

What do you think about guidance being lowered to 18-22% with no margin improvements? The valuations are a bit rich for this growth.

Company is conservative in its guidance. Last year, they have guided for 27-30% CC Revenue growth and 19-20% EBITDA margin for FY 24 (ref Mar 23 results investor ppt) but actual CC Revenue growth for FY 24 is 39.1% with EBITDA margin of 20.3%

7 Likes

Company is great and they have good momentum & have such model which may results in continuation of growth for foreseeable future. Let’s play with numbers to judge valuation.

Company is aiming for USD 1 B revenue till FY 27 (Source CNBC interview).

This implies 20% growth for 3 years.

As per Mr Patil, margin will improve to 22% from current 20% as we reach 1 B revenue. Hence profit will increase little more vs revenue. Let’s take profit estimation as 22% CAGR.

Current EPS is 22 and PE is 69, with 22% CAGR EPS will reach to 40 in Fy 27 (3 years).

CMP is Rs. 1500. If we expect 15% CAGR of price improvement than Share price in 3 years will be Rs. 2300 and PE at that time will be 57.

Considering all this, as per my opinion, current valuation seems on high side. In Q3 KPIT revise guidance (if any), if it gets some upward revision, it may be considered for investment.

Calculation 2:

Current PAT margin is 12.2%, if PAT margin improves to 15% than at 1 B sales PAT will be 1275 cr and EPS will be 47 instead of 40 as considered above.

If consider share price in 3 years = Rs. 2300 than PE at that time will be 49 @ 47 EPS.

Disc: Highest holding in my PF. Not sold not added any in last year or so. My current position is hold and track. Not sebi registered and it can’t be considered as investment recommendation.

6 Likes

Q4 FY23 Concall Notes

-

Honda, Renault, BMW - clients who have announced agreements with KPIT

-

Evolving Automotive - Company’s want to move from One time Car Sale to continuous developments - Immersive Digital

-

We will look at other mobility spaces

-

CC Growth at 39.1%, led by Passenger Car

-

Guidance: CC 18-22% and EBDITA Margin of 20.5%(after ESOP Costs)

-

ESOP Costs ~ 100 Cr.(roughly 60% of cost for further years) For FY25 (FY24 was around Rs. 10 Cr. - end of FY20 ESOP Cycle) - 0.2% dilution. Attrition in Single Digit.

-

KPIT is focused on future technologies like SDV

-

OEM’s are engaging more with specialist Software Integrators (like KPIT Tech) than from Tier-I suppliers

-

Where will Growth Come from ? : pivoting from Diamond customers > Platinum, Gold customers > then to adjacencies like Industrial Farm Sector > then adding companies from India and China to Top-25

-

Engineering Spend: 30-50% captive - JV’s to build their own(BMW - Tata Tech JV). KPIT - IT and ER&D - High End Contracts

-

Clients 2-3 add every year drop 1-2 clients. Shift from Tier-1 to OEM’s

5 Likes

It is solid guidance given what is happening within the peer set. Also they typically give a conservative estimate in the start of the year and then look to upgrade guidance in the second half of the FY.

A good analytical report

Discl: Invested and hence I may be biased. not a buy sell recommendation

please do your own assessment before you buy sell.

1 Like

@1957 Great report, thanks for sharing. what are your thoughts on the promotor holding being less (39.27%)? How do you look at this?

In my view, promoter holding though an important parameter , company products, and history of company performance, promoter background should also be taken in to account before an investment decision.

There are many companies where inspite of promoter holding being low these are respected companies with investors flocking to these counters…

Apollo hospital, Mahindra & Mahindra , many Tata group companies such as Tata chemicals, Tata steel , Cipla , dr Reddy’s lab , Gokul das exports… and th list is endless

Thanks @1957 Om, I just wanted to understand the reason behind less promotor holding in KPIT. can you provide your input if possible?

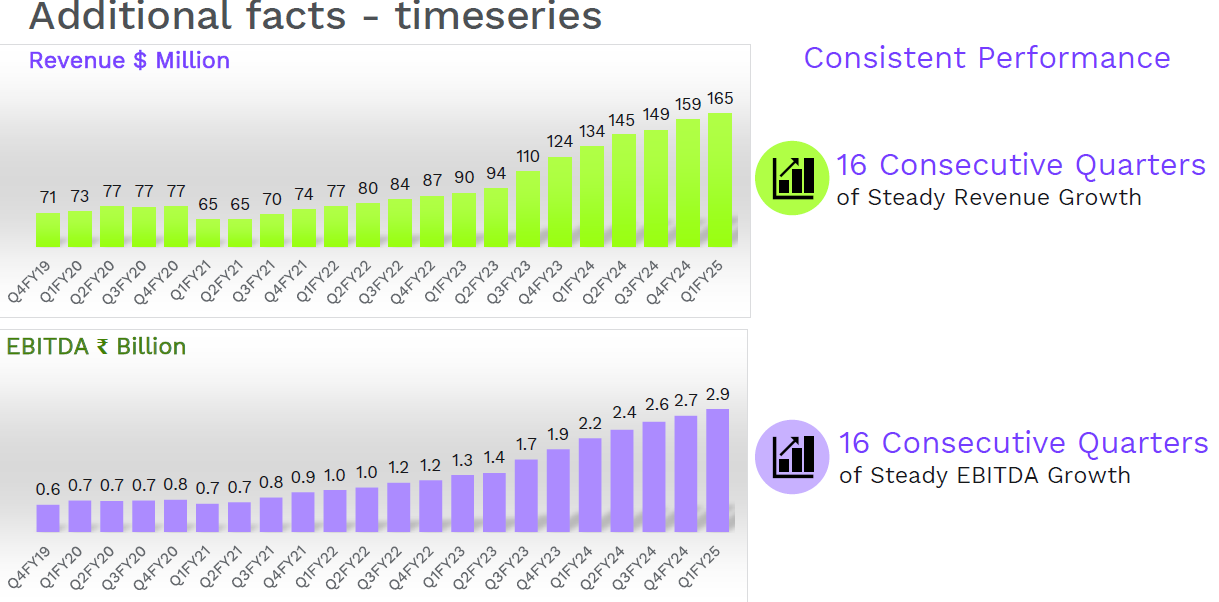

Amazing set of number by KPIT, when rest of the peers are struggling…

HDFC Bank of IT/ER&D world in the making…

5 Likes

@Marathondreams hi, Why I cant open this pdf?