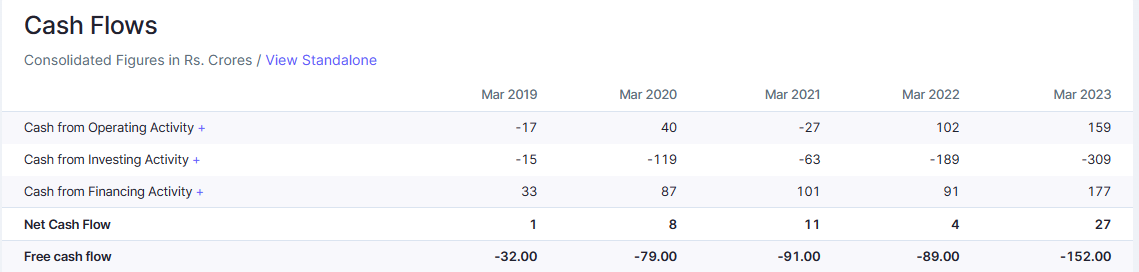

Extraordinary sales and PAT growth. I am very much interest in business only concerning me is 1) Debt now is 800cr which was 139cr 3 yrs back. I can understand this is capital intensive business, hence debt could be high.

2) another concern is why free cash flow is negative ,any idea ?

I did some maths -

Units generated under IPP - 14.78 4.31 2.92 - FY23, Q1, Q2

revenue - 97 42 31 FY23, Q1, Q2

Per unit revenue - 6.53 9.70 10.71

How can rates increase so drastically. 10rs / unit seems wrong … what am i missing here?

1 Like

Also, Q1 they did 22MW of CPP and CPP revenue was 148 cr. Q2 they did only 7 MW of CPP and revenue is 185cr. How are they recognizing revenue ?

3 Likes

Any view on yesterday’s acquisition. Promoter giving his own company to Kpi for 126 cr.

Basically KPI only buying land by giving shares.

Acquired company has no revenues.

60af2d07-ced5-4887-b295-3bb3c99d4ca8.pdf (513.0 KB)

2 Likes

They don’t won’t to pay up and freely acquiring 2% stake.!!

Now one can argue 100mw capacity etc… But 2019 incorporated. Now generating revenue 15 lacs.

If they want its their company without any complexing they can merge. ( If they want to be minority friendly)

I see this as negative development in the company.(CG issue)

On the +ve side, they see good potential in coming years so without paying, wanted to increase stake.

1 Like

Why would one give away anything without consideration? and here things are in crores…

The Target Company is engaged in the

business of development of solar power

projects. The Target Company proposes to

set up a 70 MW solar park at Dhrangadhra,

Surendranagar, Gujarat, and a 30 MW solar

park at Kantvav, Surat, Gujarat, aggregating

to 100 MW of solar power projects on

Independent Power Producer (“IPP”) model.

The Target Company also owns 2,11,367 sq

mtrs. of land at Surendranagar, Gujarat on

freehold basis for development for solar

power projects. The Target Company has also

secured necessary approvals from Gujarat

Energy Transmission Corporation Limited

(“GETCO") to evacuate the power generated

at the respective solar power plant to the

nearest 66KV / 220KV sub-station. The Target

Company has already entered into long term

power purchase agreement for sale of 30MW

of solar power proposed to be generated

from solar park located at Kantvav, Surat,

Gujarat. Further, the Target Company has

also received interest from certain customers

for sale of 70MW solar power proposed to be

generated from solar park located at

Dhrangadhra, Surendranagar, Gujarat.

But what’s bothering me is why build another company when you have KPI green to do the same thing? It is not a B2C business to choose a multi-brand model as a means to increase sales and also the land I suppose is not worth more than 30cr. but the good part as stated earlier, the promoter is trying to increase stake and not take money.

Note- Shareholder’s approval is pending and we should utilize our powers after having better clarity about the same.

2 Likes

This is big negative… Only value here is land … Can someone please confirm the value of land Surendranagar, Gujarat. There is no other value here… and get the stock @830. discount to market…

I check 1 more thing on KP group website, they have 35 companies in total… Also, they are doing hybrid in KP Green. Why do they need KP energy?

There are clear signs of CG issues… Lot of things are unanswered here.

- why do you need 35 companies? tax / debt / etc…

- His political linkages / influence is very high in gujrat. I doubt they will be able to replicate the same in any other state. Thats why in concall also, he didnt answered that question that y they are able to go much better than peers

- IPP revenue model - seems extraordinarly good. so good to belive for long term or outside Gujarat.

They can do exceptional well in Gujrat and target shared by mgmt are achievable in Gujarat. what they have build is commendable but again i might not have all the knowlege to give concreate opinion.

I feel you can ride on the bull market to make some qucik bucks but keep caution. This is my personal opinion. I can have divergent view going forward. This is as per my reseach till date.

Disc. - no positions

2 Likes

Precisely for these reasons I exited the stock completely in good profit and entered Waaree Renewable Technologies Ltd.

Somehow, I was not comfortable given their leadership is ONLY in Gujarat. I may be completely wrong about this company and their future plans.

1 Like

The other factors that started worrying me are:

- Mounting debt

- Most of the promoter holding is pledged

- Most of the disclosures to exchanges is done by the chairman & MD (Mr. Faruk G Patel) him self. I am wondering why are these not coming through a company secretary/compliance officer? Do they have in place ? Now a days even smallest SME companies have this position in the company.

- Also, I have a feeling that they are paying dividend for the sake of paying. I would rather expect the company to come forward with a plan to reduce the debt and release the pledged shares.

2 Likes

Have tried multiple times to get in touch with the CS Ms.Rajvi in the past 1.5 years but have always failed miserably, today again a receptionist answered the call and told me to call back in an hour, as you might have guessed they stopped answering again, and there is no response to emails either.

Disclosure - Have moved out of the company completely and will have no regrets even if it goes 10x from here or no joy if tomorrow some fraud is exposed, will only associate with people who let me sleep peacefully.

KPI Green gave me 400%+ in the last 1.5 years so yeah no regrets anyways.

Happy investing! cya KP!

6 Likes

Good to see the detailed analysis on this stock and results.

Also good to see people exiting based on thier exit plan.

What i feel the company has a smart promoter, as all it says gujarat based and focused, its double better because this govt is very biased with certain things. Once the govt is favourable its like luck working with you.

Better to stay with where the water flow.

1 Like

Smartness is good but when utilized for the growth of everyone and is disastrous when it is self-centred, ever checked out KP group’s YouTube channel? Filled with auto-biographies of Mr.Farukh which nobody is interested in watching and now this deal clears his intentions and where the company will end up in the long run…the land is not worth more than 25-30Crs. as the outskirts of Surendranagar which is a small town (45 km²) in Gujarat has land prices between 80-100rs/sqft so 2275135.45 sqft x 100 = 22.75Crs. and these guys are ready to pay 126Crs. for that. If you see the AR this guy owns 25+ such companies (why?) more than enough to buy back the entire KPI green for peanuts. Already the debt/equity is at 2.4 and they want to do a further fundraising…amusing! Things were manageable until the developments in the past few days. Would you distribute water if you don’t have enough to drink? but they do! Generous? Don’t have money to fund projects and distribute dividends and who benefits the most out of dividends? Smart? There are many many fishes out there so it is wise not to waste your bait on a fish that might just break the line and take it away.

8 Likes

How do you arrive at a land price of 100 per sq ft?

It definitely needs to be ₹500/ft2 at least to make up the math considering the company didn’t have any meaningful revenue.

1 Like

https://www.99acres.com/agricultural-land-in-surendranagar-ffid

https://www.magicbricks.com/agricultural-land-for-sale-in-surendranagar-pppfs

Actually to make things more digestable for everyone and thinking “Kpark” has the most premium land of them all i chose the upper end of the prevailing market prices, to be honest the average is no more than 40rs/sqft. which makes the land not worth more than 9.1Crs. and such huge land parcels are only situated in outskirts of a town, mostly agricultural land. What else do you expect the land prices to be? in a place none of us have ever heard of. Solar farms need the cheapest of land to make things workout.

5 Likes

Yes, it is always a red flag when company is unable to explain it’s competitive advantage and high accounting profits when others in the same region are making losses in the exact same business they are. And, two things as investors we should look for as signals - 1) whether promoter is engaging in building own brand and not of the company, and 2) related party transactions that promoters benefit from substantially.

From above, it is absolutely clear that price may go up / down (who knows) in near term but in the long-term investors will stand to lose.

please share screen shot where mentioned 35 companies total of KP group

1 Like

Please , share information which indicates promoter get benefitted from related party transaction ?

promoter already holds more than 50 percent stake , so our power useless while voting for Kpark buying decision

2 Likes