Thankful for the detailed analysis and notes mentioned above. Had done a small analysis on various hospitals during Yatharth’s IPO.

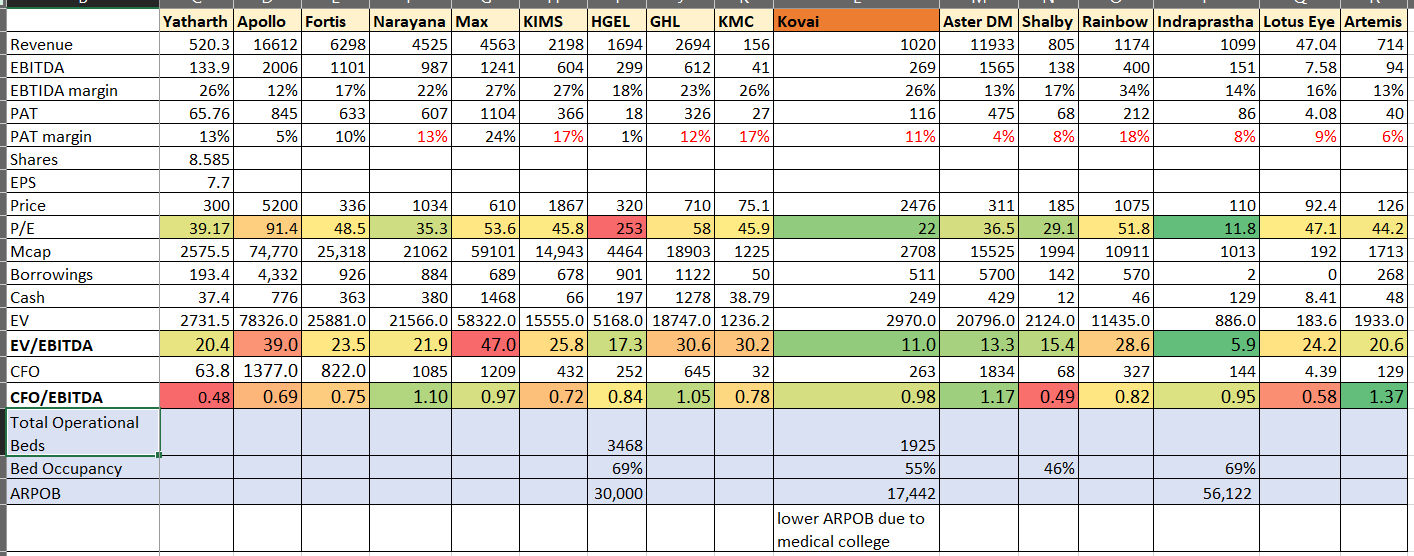

Considering the run-up of various hospitals, Kovai is the only one that seems reasonably priced. Indraprastha is stuck in legal issues considering their agreement with Delhi govt. for providing free-of-cost treatment in lieu of lease of hospital land.

Note: Data is from early Aug for other hospitals

The only issues I can see are:

- The company doesn’t seem to have geographical expansion plans. It’s a good stable business that appears to be undervalued but no amazing story

- Medical college is impacting PAT margins and the company has high interest costs

- Lack of institutional interest and low market vol. depth

- The Google reviews (not sure how reliable they are) are not favourable. Usually they’re above 4 for major hospitals in most cities, see Royal Care is 4.3. This might impact patient inflow

- Lack of medical tourism, which is a very high margin business for most hospitals. They don’t have MTQUA certification (only NABH) which Sri Ramakrishna Hospital in Coimbatore has

- From annual report, their Inpatient nos. increased 25% while revenue only increased 5% (decrease in ARPOB) which they need to pass on

Pros:

- Promoter holding has increased this quarter

- Cheaper valuation (P/E, EV to EBITDA, CFO to EBITDA) compared to other hospitals (see KIMS) considering the no. of beds and strong brand image (as per their AGM and comments from people above)

- Most of Coimbatore population is in urban areas and it is growing at 2.65% rate per annum (same as Delhi)

- In Tamil Nadu, IPD per 1000 is double that of India, implying people are more inclined towards hospitalization services in the state

Happy to get feedback, insights from other people

Disc: Invested and averaging down