I happened to chance upon some interesting data points on Kotak Mahindra Bank while doing research for my Coffee Can Portfolio and comparing different Banks/NBFCs.

I’m sharing the same here along with my observations:

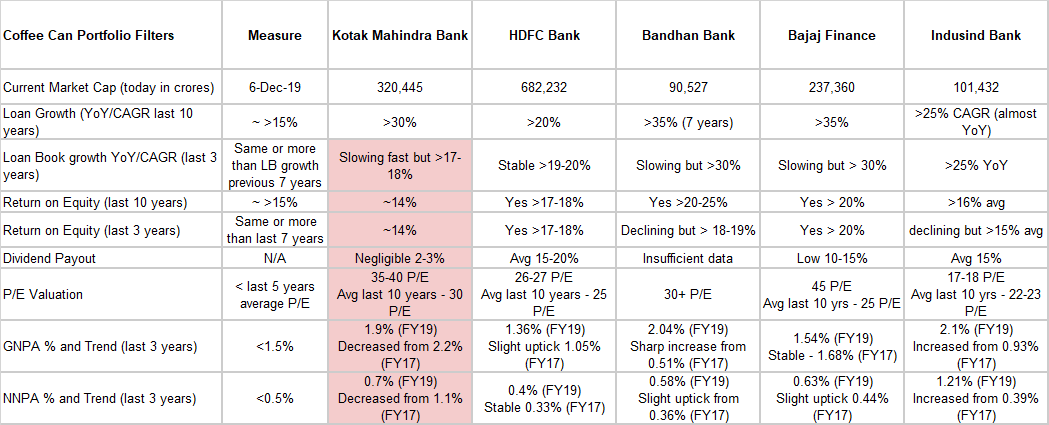

Please note my observations are till FY19 only and sharing them here only to arouse discussion on the market fancy and valuation for this bank vis a vis peers. Personally, I find Kotak Mahindra Bank to be one of the best banks in India with top-notch management but it’s financial metrics do not reflect market leading characteristics:

The banks/NBFCs chosen for comparison are ones with loan book growth > 15% on a 10,5,3, last year basis and RoE > 15% each year for last 10 years (might have given benefit of doubt for one/two years here or there for a particular Bank/NBFC). Hence, the following make the cut

HDFC Bank

Bandhan Bank

Indusind Bank

Bajaj Finance

Prima facie, Kotak Mahindra Bank’s recent growth and financial metrics appear to be inferior when compared with any other leading Bank/NBFC.

-

Kotak’s loan book growth has slowed down considerably in the past 10 years from 30% CAGR to 17-18% levels which is currently the slowest amongst all peers

-

Kotak has the worst Return on Equity across all peers not only for last few years but also avg RoE for last 10 years is sub 15%

The management has mentioned this in their Annual Report 18-19 regarding low RoEs:

“The Group’s return on average networth was 13.34% for FY 2019 compared to 13.47% for FY 2018. One of the key reasons for low ROE of the group is low leverage (debt-to-equity) ratio. The Bank has been conservative and has been maintaining high capital adequacy

ratio which results in low return on equity.”

Whatever said and done about Kotak management approach, other leading Banks/NBFCs have been able to grow faster with better return profiles

Basant Maheshwari tweeted this about RoEs for a company - (definitely not infering Kotak falls in crooks category, but definitely infering it doesn’t fall in market leaders category)

-

As a fallout of maintaining high capital adequacy, the management does not like to distribute meaningful dividends and only gives token dividends 2-3% payout. Even the super fast growing Bajaj Finance has much higher payout

-

Asset Quality - This is where Kotak compares favorably with most lenders in terms of NPA ratios but still falls behind market leading book quality of HDFC Bank and is not a clear market leader in terms of asset quality as well. Both Bandhan Bank and Bajaj Finance have an equally good quality of book

-

Valuation - Now given all of the above, this is the final piece of the jigsaw which should help explain where and why Kotak’s stands compared to peers. However, when it comes to valuations Kotak appears to be the most expensive bank given it’s lower loan book growth, lower Return on Equity, lower Dividend when compared to other Banks/NBFCs.

I’ve used the P/E ratio for valuation here, but even if you use the P/B measure you’ll find it to be more expensive than likes of HDFC Bank, Indusind Bank which is extremely puzzling.

The only joker in the pack for Kotak I can think of is the AMC and Insurance business which the market has taken a lot of fancy for and can explain such high valuations with inferior growth / return metrics.

Views invited.