Kontor Space Limited

Co-Working (SaaS – Service as a space) has been in tailwind in corporate India for last 1 year, the tailwinds are so strong that a listed company out of no where came and conquered the market, made huge wealth for it’s shareholder almost 30x in 2 years and still at reasonable valuations are projecting to almost double it’s growth at even current rate from 450 crores to 1000 crores

Before we deep-dive into this,

Special Thanks to @Dhruv_Bajaj and SSS team for their deep dive analysis on Co-working space

(for those who haven’t seen the same - https://www.youtube.com/watch?v=gkQJMqkHI4c) the above helped me understand why there’s immense leg of growth for co-working theme in India.

Before we start with Kontor let’s understand the business model –

So before we start let’s understand the 3 key player

i. Developer Developer is the person developing the project/Piece of real estate Infra with either the objective of selling the project or collect rentals from the same. If sold they don’t fall under this value chain but is used the same for rental, the developer generally doesn’t rent it out on itself, reason they don’t want to get involved with 100s of tenants, they either prefer to deal with one person than 100 (Understandable right?)

ii. Operator Here comes the person who saved them from the headache of minute details of tenants, So basically they rent out the whole floor in commercial area from the developer and following to which they Sub let it. Meaning Business Just like a bank, Deposit liyya and Loaned it out

The operator can either operate in a way where they Rent it out (office) to a single tenant or rent it out to multiple tenants (Co-Working space), Multiple tenants benefit you and your tenants in a big way.!, the rent charged here is per person, per seat, per month, meaning you pay for the seats your employee occupies for the particular time. Whereas total accumulated rent over the total Sq. feet is higher in comparison if the total area was leased out to the single tenant as the bargaining power in volume of Sq. feet increases (Kontor, EFC (i) Falls here)

iii. Tenant Tenant as explained above has huge value proposition main reason being that the rent to be paid is limited to the seats occupied, meaning that no extra cost to be incurred on rental, let’s understand the value proposition and what’s driving the value in Co-working space and what’s causing tailwinds in detail

Whenever you take a corporate office on rental you not only have to incur rental expenses but also start having overheads from the very first Day, such as Security guard, housekeeping, Cafeteria, Electricity, etc.

Infact above are just the revenue expenses you also have to incur substantial capital expenditure Expenditure such as Renovation/Decoration, Interior designing, Requirement of furniture + electrical appliances and last but not least decommissioning cost.

The above coupled with many small reasons have resulted in major corporate rental inventory to shift from single company rental to Co-working rental.

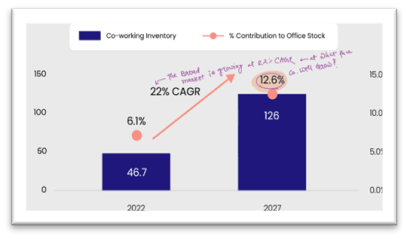

Infact the attached SS from SSS’s YouTube video states that the broader market is it self growing at 22% CAGR on account of double sword Increase in co-working inventory (Real Estate Infra made particularly for the Co-working space) + Transformation of existing inventory in Co-working Space due to preference of the worker. Resulting in low OH cost + Focus on core operations

Shifting our focus towards main operators now:

Business Is fairly simple à Take on rent, Given on rent à what causes the differentiation than differentiation is basically the tenure for which your customer stays,

The average lease tenure for Kontor is Around 5 years, meaning no matter what they’ll have to pay 5 year’s rent (If lock in period exists than 3 – 4 months’ rent based on notice period through which Kontor can terminate the contract)

Hence if you have long enough lease with your tenant that it covers your rental period à it immunizes you heavily since the confirmation that your inventory will be occupied for x years at least gives you cashflow predictability.

With Rental coming in is the main income and rental going out is main expenses where your rental going out < Rental coming in Your cashflows are superior with almost -ve working capital since the leases spaces are to corporates who generally don’t default on rents unless there’s a black swan.

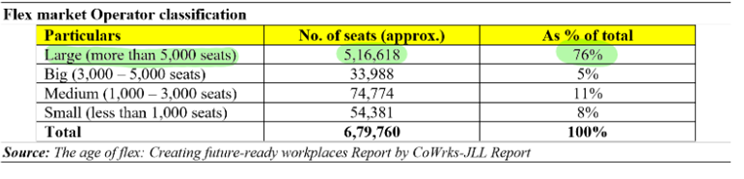

The market is so concentrated at this point with large players (Refer below Exhibit: )

The Source: DRHP states that major market is covered by the players with seating capacity per player is cross of 5,000 seats.

Interesting Data point from Dhruv’s video that Pre covid there were 100s of Players in this field the same has now reduced to 7-8 with material market share (Indicating the capital cycle has been played out at least on downside side for now and resulted in consolidation.

The Source: DRHP states that major market is covered by the players with seating capacity per player is cross of 5,000 seats.

Interesting Data point from Dhruv’s video that Pre covid there were 100s of Players in this field the same has now reduced to 7-8 with material market share (Indicating the capital cycle has been played out at least on downside side for now and resulted in consolidation.

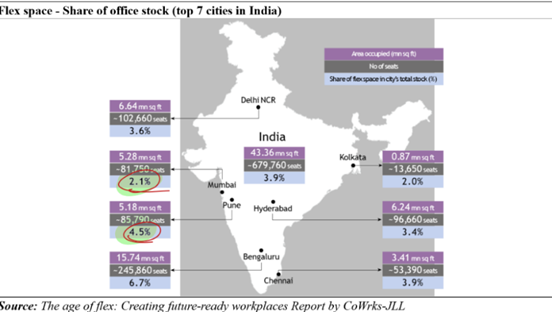

Here the major tailwinds can be witnessed in area where there are affordable seats: Refer below exhibits from the SS

Even EFC (I) is focusing on providing seats at the price of $ 100 or less meaning in high tailwind are

However the penetration in comparison to developed economy where the same is across 5% Which is also growing at 7% p.a. (Mind you for developed market any industry at 5%+ is tailwind) India is at 3.5% (of total rental space not just corporate offices)(Same source)

The penetration has to reach somewhere between 4.5% to 5% but we have to decide where the penetration has to grow

Lowest penetration is in Mumbai and Kolkata

Mumbai is the major market for Kontor but will discuss the next section.

Kontor Space: core business revolves around acquiring and leasing properties, which then they sublease to a single or multiple clients on a per-seat basis, providing flexible and modern workspace solutions.

The company incorporated in 2018 was bought out by current promoter Mr. Kanak Mangal who with his wife runs the operations as of now

3 Months lag between the operations Hire/Rent from developer, renovate/Design and than lease takes approx. 3 months of time hence the rental for the same period is deducted from their pocket if you see Q4/H2 Margins they took a big hit, reason being that they didn’t had any anchor and then too went forward with the inventory that caused them to pay 3 months rent without the property being occupied by the tenant

The company did IPO at the price of 93 per share in October of 2023, the entire issue was Fresh Issue, not a single OFS a good soft sign where in environment IPO are predominantly IPO are for dumping stocks on retailers

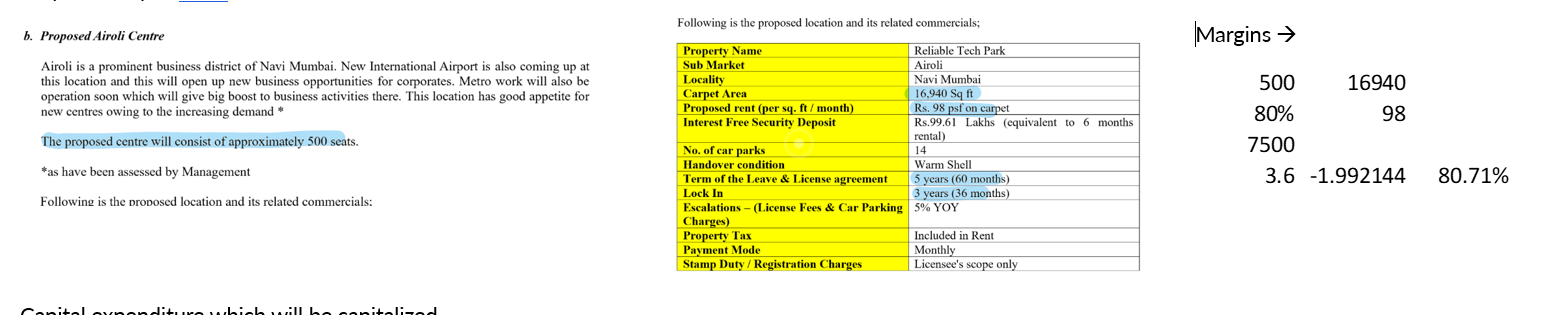

The IPO was of Quantum of 12 crores where the majority chunk of money is to be used for à Capital expenditure (i.e., Designing and renovating the office) + Security deposits for new office in Andheri east (300 Seats) (4.71 crores) and Navi Mumbai (500 Seats) (6.69 Crores + Security deposits) (Will discuss the calculations later)

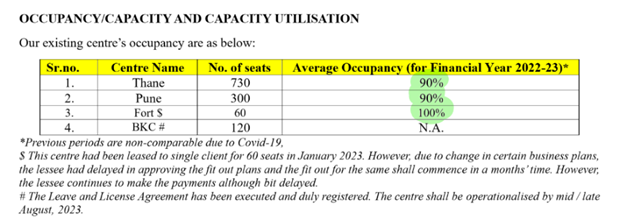

Currently they are predominant into Maharashtra: With location in Thane, Pune and Mumbai (BKC and Fort)

Revenue per seat is

à Thane à 10,000 – 15,000 Per seat Per month

à BKC à 45,000 Per seat Per Month

à Fort à 800,000 – 900,000 Per Month (Lump Sum)

Currently they are predominant into Maharashtra: With location in Thane, Pune and Mumbai (BKC and Fort)

Revenue per seat is

à Thane à 10,000 – 15,000 Per seat Per month

à BKC à 45,000 Per seat Per Month

à Fort à 800,000 – 900,000 Per Month (Lump Sum)

For FY – 25 they are targeting to double the Seating capacity to 5,000 Seat from current 2,500 Seats à moving from small to big league, Even post that they will be targeting doubling seat capacity in FY 26 to 10,000 Seats (This is Under delivery target) they want to under promise and over deliver hence if investing one can assume if execution goes smooth and tailwinds prevails than the seating capacity can be added more than initially guided for, not against adding more in the words of promoter himself, however this will require a huge capital, infact around 30 – 40 crores, which will be put by promoters + Internal accruals

However they’ll also try fit out financing as the option (% of rate of interest is attractive here)

Fit-out financing refers to a type of financing that is specifically designed to cover the costs associated with fitting out or renovating a commercial property. This type of financing is typically used by businesses or individuals who lease or purchase a property that requires customization or improvements to meet their specific needs.

Fit-out financing may cover expenses such as construction, renovation, interior design, installation of fixtures and fittings, and other related costs. It allows the borrower to spread the cost of these improvements over time, rather than paying for them upfront, which can be particularly beneficial for businesses with limited capital resources.

Fit-out financing can be structured in various ways, including term loans, lines of credit, or leasing arrangements. The terms and conditions of fit-out financing will vary depending on the lender and the specific needs of the borrower, including factors such as the cost of the fit-out, the borrower’s creditworthiness, and the overall financial health of the business.

Cash accruals:

The business model is such that major receipt and Major payment in itself is rent, at 1st of the month you get the payment of rent at charged up % and you have to pay the same to your developer, hence the chances of cash getting sucked is faar less.

The major cash flow issue here is Security deposits, however they are offsetting in nature if the occupancy is there

Industry Tailwinds:

As Dhruv Explained how We work US was killed by Asset liability mis-match and how you need a good Demand side/Tenant side period for long term to evade this risk, company is doing the same where the period of tenancy = Period of their lease agreement

Risk Averse Management 50% Anchor in place will mean for them than 50% occupancy is confirmed from the very first day, However 50% anchor will mean that they will be charging low rent in corner of 5% - 7% against the market rates (however, management is happy to let that 5% - 7% go if that mean they can have certainty over uncertainty)

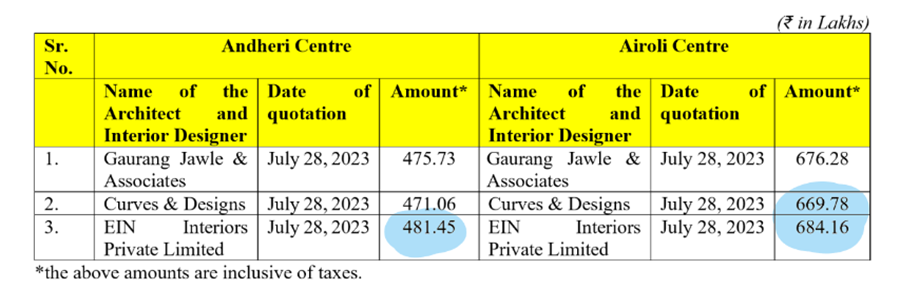

Interior Designing the Capex for designing is outsourced to contractor that is big competitive deficiency EFCI has it’s own team where as this being a pure play Coworking space it outsources such work

Difference from EFC (I) EFC (I) has it’s own employees undertaking the task of interior decoration, Fit out contracts, etc. but Kontor outsources the same, this can be competitive advantage from EFC (I)’s perspective as the cost per seat charged to the customer will be lower that the Company.

Furniture building which is the major cost of the Capex is in house that is the good competitive advantage for EFC (I)

Leave and License Currently the company is in leave and license agreement where by the company takes the rental property from the developer and than re rents it, however the time period is generally 5 years with pre fixed % increase in the rentals the same may not be aligned with the market rate of interest after x years for new tenant since the tenancy agreement of the company with tenant is generally less in time period than that of the agreement with the developer

Very Similar Story to EFC (I) EFC (I) listed company taken over by existing promoters and did the huge fund raise for the purpose of capacity expansion did the huge execution smoothly and made great money for investors,

Kontor Incorporated in 2018 was taken over by the existing promoters Mr. Kanak Mangal at the price of Rupees 10/- Share in 2022

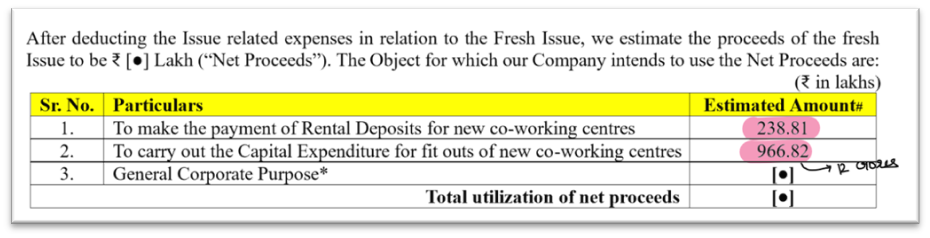

Proposed Capex From IPO Proceeds Andheri 50% anchor already given, 100% utilization should be from July of this Year

Proposed Capex From IPO Navi Mumbai

Capital expenditure which will be capitalized

In margin calculations what gives me so confidence in occupancy is this exhibit:

Service Portfolio

Red Flag

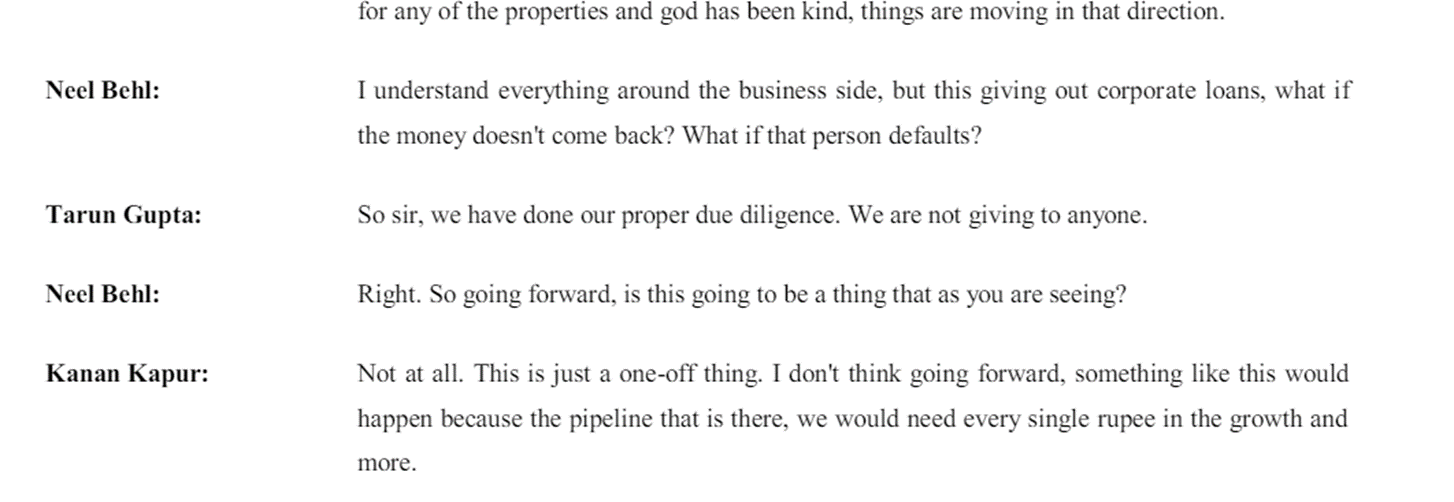

Inter-corporate loan given out from the monies raised in IPO Because the same where to be utilized after certain point of time, couldn’t understand the risk aversity of the management at one point they are putting anchor lock in of 50% to remove the cap of uncertainty and giving away money to corporates at loans which funds were to be utilized for the purpose of Capex?

Even Neel Sir was very pissed it seems from this decision

2nd Red Flag à The company has the loan outstanding of 60 Lakhs which Is for Rolls-Royce of 60 lakhs the book value of which is around 1.01 crores.!

The car is completely used for the purpose of management/Promoters

However I feel, that’s how microcap are, there will be some or the other issues,

But if tailwinds are so strong you can’t wait on sidelines.!!

3rd Red Flag Market Maker Rikhav Securities Involved in Market making of Varanium Cloud and QMS Medical Allied services A potential Red Flag

Summarizing: When the sector is growing at a staggering rate the lined up capex for the company is huge, from 1250 seats in 2024 to 25000 Seats vision is a huge thing,

Company is moving from Big boy league, I’ll be happy if they achieve 75% of what they have Guided (10,000 Seats) leave alone 25,000 seats

Red flags are something to keep tracking, this might blunder up the whole thesis

Disclaimer → Invested Recently

Edit: Added the snap shot In Industry tailwind column