Receivables is 314 Cr for the year that is approx. 40% of the total sales with almost 5 months receivables days ! Still a curious case !

1 Like

Just about when they were about to exit Kerala, the recent announcement of the alliance with Aam aadmi party could mean that the promoters focus on business could be distracted, in fact they will have to provide for more CSR grant as they usually do, also, the rising receivables and debt and a mammoth capex of 3400 cr could keep the performance of the company subdued. Until the cloud gets cleared its a wait and watch.

Disc - Exited at cmp

1 Like

I follow this stock mainly for learning insight into management behavoiur.

FCF is the most important sign of management integrity of a profitable company.

Beware

- When the profits dont go to the retail investor’s hands as dividends or .

- When the promoter gets too close to or fights with the govt. Both situations are bad.

- Retail investor is doomed when the profits are diverted as

** increased Debts and recievables (PC Jewellers, kitex)

** Random capital expenditure which was never needed or even never undertaken except on paper. (Sintex?, kitex with telangana buzz)

** Increased extraordinary payout to promoters but does not work once the companies go very big.

** Creating of random subsidiaries generally used to siphon off money. (Kelltron Tech, Kitex USA LCC where the company made more losses than the investement made)

** Very lofty claims about the future by the management which are not backed by results almost always. (Vakrangee which went into the MSCI index claimed to open 1000000000000 atms as an excuse of not paying dividends, kitex about the set up in telangana project)

** You are told that there are sales but u dont see products in the markets. Generally the claim will be its sold in places you dont live in. (Eg: manpasand beverages, Teledata informatics (past), kitex )

** Claim to achieve something that no competition however good can achieve without the presence of any significant “moats” (eg: Manpasand, kitex vs. page)

A friend who is an expert at this once told me. FCF does not generally lie. P&L statement is bs.

This comes from someone who like most of you started off investing by looking at the stocks with the filter showing lowers PE number.

I know people here come to hear good news about their favorite stock. But may be devils’ advocate is not always wrong.

20 Likes

70% funds from debt

it will be interesting to see how they manage the debt

as per Mr. sabu they get an interest subsidy from the state govt. and their net cost will be only 1%. Also, they get PLI and other incentives from various govt. He says almost 70% of the invested amount they will get back in the forms of various incentives over 2 to 3 years.

Disc: Invested

2 Likes

1 Like

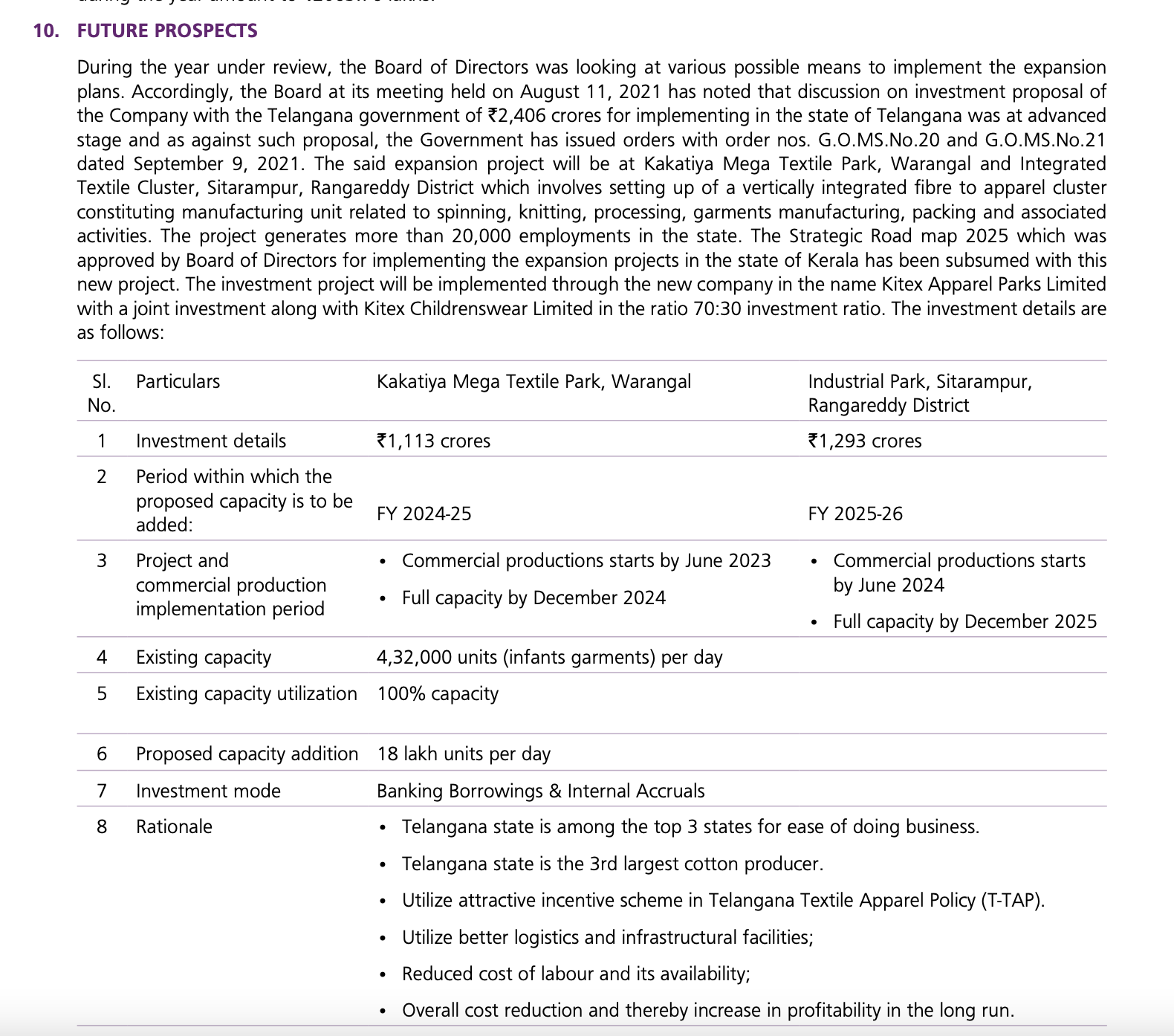

The expansion announcements from Kitex are very good. But I have observed one fact that at the time of first announcement, they said that initial commercial production from Kakatiya Mega Textile Park will start from November 2022, then they forwarded it to January 2023, and then to March 2023 in the subsequent news articles. Now in the annual report they are saying that this will further move forward to June 2023. We can check these dates by searching on Google. I sincerely hope they do not delay it further as there might be a slight slowdown in their main US markets in the next one year.

Disclosure: Invested but slightly reduced my position.

3 Likes

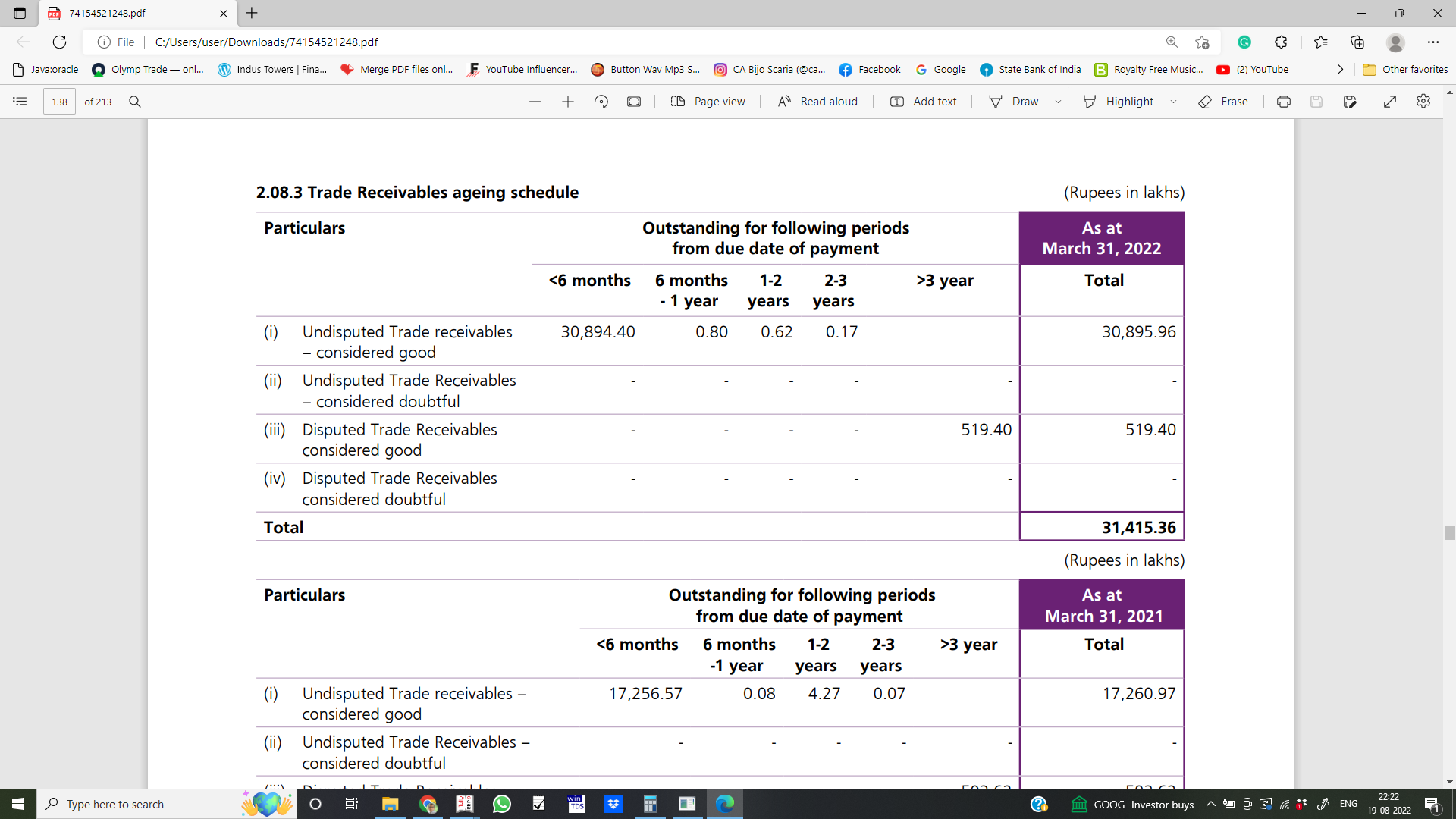

Extract of Trade receivables from kitex annual report 2022. Most of the receivables are due in less than 6 months. Total trade receivables accounts 38% of total sales. when u see the 2021 figures most of the receivables are due in less than 6 months. same account for around 38% of sales. compared to last year no unusual in receivables.

Cash flow only 3 crore fro operation due to doubling the sales in 2022 compared to 2011 accordingly receivables are got increased in 2022

5 Likes

Board Meeting update:

Kitex Apparel Parks Limited being subsidiary company has signed the consortium of rupee term loan for expansion project in the state of Telangana on January 5, 2023 for an amount of Rs. 2023 crores plus Rs. 10.94 crores as CEL facility with the State Bank of India being the lead banker to the consortium of rupee loan along with Union Bank of India, Bank of Baroda, Axis Bank and Exim Bank.

See the board meeting minutes here.

This is a really big bet and will lead to an additional annual interest outgo in excess of 150 Crore once this loan is fully availed(i have not considered any interest subvention / other benefits as claimed by management earlier due to lack of credible supporting details). I can only hope at this stage that the management has incremental order visibility to of atlest 500 to 700 Crore from the new textile park. Note that the current annual PBT is just above 150 Crore.

Disclosure: Remain invested.

5 Likes

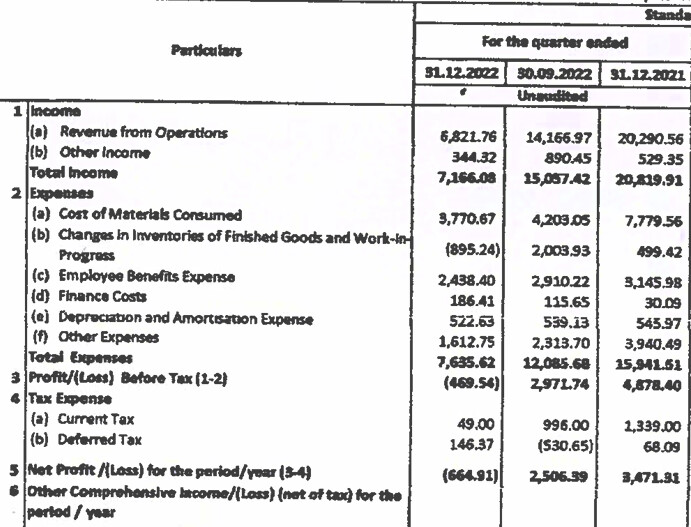

Has the slowdown caused the lowest quarterly revenue in recent years? Wondering what was the level of incremental order visibility that led to their decision to establish a park in Telangana?

2 Likes

Been holding this from 2016 and have witnessed a number of cycles with Kitex.

After reviewing the Q3 result and considering significant capital commitments for the new plants coming up in Telangana, I have decided to book loss and exit my holdings.

My assessment is that this phase(over next two years until new the new plants are fully operational and profitable) is likely to be pose significant challenge to the management. Large capital outlay coupled with lack of operating cash flows is not good news for investors. I certainly hope management can come out of this phase stronger and build a world class Indian company(I have bought their infant and toddler products for my own son and as gift for others and can certainly testify that they are of the finest quality) and hope to re-enter once green shoots are visible.

AJ

7 Likes

Every business goes through its ups and downs. But giving an honest guidance is much better than always boasting about winning the world.

For Kitex Q3 was from October till December 2022. The orders for delivery to customers in October 2022 must have been booked latest by the month of April, May, or June 2022. So they must have known about this huge slowdown much in advance. But even in an article “Kitex Garments entering a crucial phase of growth” dated 6 September 2022, they were quite bullish on the business and literally misguiding the investors.

Now, even for the first phase of expansion, Kitex Garments plans to invest Rs 700 crores (out of total first phase investment of Rs 1,000 crores). Out of this Rs 700 crores, Rs 200 crores is supposed to be from its own funds and Rs 500 crores will be in form of debt raised from banks. Assuming it’s a 10 year Rs 500 crore loan with most of the interest subsidized by the Telangana government, still the company will have to pay at least Rs 50 crore per year as the principal payment immediately after receiving the loan.

As per the company’s announcement in the Q3 results, the next few quarters are also going to be bad. Hence even if they succeed in raising the loan, net of Rs 50 crore principle payment what will they earn as profit. Hence, in my opinion, the next six months to one year is going to be very extremely difficult for the company.

Disclosure: Sold off the entire quantity today to find some other honest company to replace Kitex Garments in my portfolio.

7 Likes

Is Kitex a candidate for mean reversion? What is the reason for such a drop in revenue? Also, it could be a good(?) sign that the company is not doing any earnings management. I don’t think they are going out of business.

Update:

Here is an article that gives an explanation for the bad performance.

Disclosure: Hold

There is no dearth of announcements !

5 Likes

Because of the impending recession in the US, if it does happen, then we will see a continued depression in the revenue of Kitex? Highly likely? Hopefully, the timing of the capex in Telangana is also not going to weigh down on the company. Lot of uncertainty in the near future?

2 Likes

Hi everyone, as per the latest annual report of Kitex Garments, they are now expecting to commence commercial production from their KMTP Warangal Project which is their first stage expansion only by March 2024. It might or might not be full production level. It seems that the benefits of the first stage of expansion will reflect only in the full year results of the year from April 2024 to March 2025. I am quoting from their latest annual report below.

Blockquote

The first Project at KMTP Waranga is well advanced with the Land fully procured, Buildings getting near completion and types of machinery have started arriving with major LCs opened for procurement of machines. The Company has already contributed a major portion of Promoters Equity. Commercial production is expected to commence in March 2024.

Blockquote

1 Like

Kitex kick start second plant at telegana which is world largest manufacturing unit

Disc: Invested expecting to be a turnaround story after 2026

2 Likes