Funny that the AGM did not address the elephant in the room, the (lack of) corporate governance issues. Makes everything else a bit pointless.

3 Likes

What issues exactly?

Thank you so much Ayush and Shikhar, great help for those who are unable to attend AGM.

So all things said, there is no price advantage to Kitex, in spite of all quality and processes implemented. It is a commodity for the US customers. In that case, the only extra money Kitex can make is in the higher efficiency, isn’t it?

With this, will it be able to go back to the older margin levels of 25-30%?

Why is capacity expansion such a huge issue for Kitex. As far as I understand, their competitors Jay Jay was able to ramp up capacity, they even have a manufacturing unit in Ethiopia now. Of course with a much lesser margin and efficiency.

The methodology for scaling that Kitex is trying now - satellite mother units - is something new to them, and they aren’t replicating what they have done successfully until now. Isn’t it a risk again?

Disc: Invested

2 Likes

Thanks for the notes @Shikhar and @ayushmit really appreciate the effort of travelling all the way to attend the AGM. Hope the weather was all right in Kochi!

On a serious note, while it is nice to know that Little Star and Lamaze are doing well, did anyone talk about the actual turn over achieved by these brands? I couldn’t find these numbers in the Annual Report as well - i believe the growth in margins will directly be proportional to the growth of turn over achieved by these brands.

Thanks,

Disclosure: Invested

@johnsgeorge.cet - Its not easy to make out on exact pricing cause the answers are not very clear. Management also says that sourcing is spread across different countries and hence even if one country is cheaper, cos will continue to source from other countries too to have diverse supply chain. As per them, the quality and safety is very important and many players are not able to delivery the right thing in right time…and many people cut corners. While Kitex has been able to deliver consistently. Also, such large qtys of supply are not possible so they are able to negotiate a bit with client. But overall its competitive. They get preference from buyer.

Yes, efficiency and integrated operations are the reasons for better margins.

Management continues to promise around growth and better profits - however we all have learnt to take guidance with bucket load of salt

Jay Jay did grow in between but I think they were also flat last year. Also, Jay Jay is spread across various geographies. Perhaps the challenge for Kitex is having more employees at same location hence they had been trying for automation etc and now several small units. Yes, its a risk and we should not bank on the same till they deliver to some extent.

@AJ41 - i have mentioned in my note - revenue was just $2mln from little star and lamaze.

7 Likes

Thanks @ayushmit and @Shikhar for detailed summary of the AGM.

I attended the AGM as well. To my mind there were a couple of major developments which indicate weakening in the business model.

Accounts receivable: Four to five years back the customers used to pay Kitex pretty much immediately. Now the credit period has increased from 30 days to 90 days. There is no guarantee that it cannot become worse. The only reason for this is competition whose unwise credit terms has forced Kitex to do the same. The bargaining power of the customers has definitely become much stronger.

This situation is sort of reminiscent of what is said of commodity businesses - Pricing is determined by the dumbest competitor. Here it seems like both pricing and the terms of trade are determined by the dumbest competitor.

This situation is worsened by:

Customer concentration risk: With Jockey and TRU no longer being customers of Kitex, the customer concentration risk has increased materially with just 2 customers forming a large portion of the sales today. It felt like Little Star and Lamaze are ramping slower than expected.

Having said that the infrastructure of Kitex ensures that anytime a customer wants to procure garments, Kitex remains the first port of call - provided they match the credit period and the price.

And it does seem like there is a lot of orders at hand.

Also, there was a huge worry last year of Auditor resigning. It is pertinent to note that Varma & Varma remain associated with Kitex. My thought here is if the auditor is really uncomfortable, they would sever all existing ties.

8 Likes

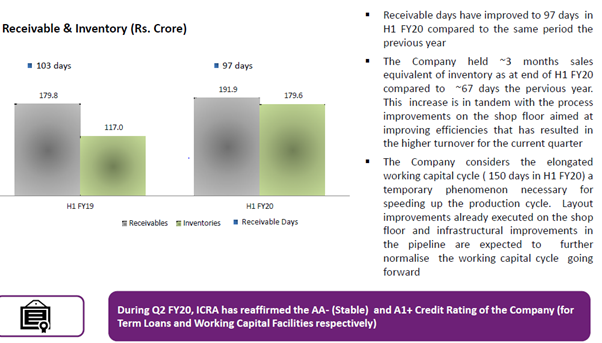

Quick notes from the H1 results -

- Sales has grown by 17% while the gross margins have slightly improved by 1.5% in comparison to previous year H1.

- Noticed sharp increase in inventory level - at the current sales runrate, closing inventory of Rs. 180 Cr would be sufficient for the next 180 days - note that the inventory levels has been at undesirable levels from quite some time now.

- Receivables position is deteriorating and i believe this is due to a change in business model where the US associate is now procuring directly from the company and much of the receivables must be outstanding from them. Additionally one need to note that Associate company accounts are not consolidated into KGL(it would be really difficult to find out the actual receivables outstanding unless the company voluntarily disclose those numbers).

- The share of profit/loss from associate is left blank - (i’m not sure of the reason and i believe, this could well be a disclosure error from management while the financial statement were is prepared and a clear lack of due-diligence on part of auditors considering they have included Kitex USA LLC in its purview of review for the current period) considering the past trend, the company should have ideally disclosed a loss for the period - note that the associate has been declaring loss from the time of its inception.

- Other expense continues to show undesirable trend - increasing by 50% on an H1 comparison and it could well be due to its contribution to trusts and CSR.

- Income tax gains are as expected.

- The cash position has improved significantly as compared to March 2019 levels and the balance sheet shows a net cash positive position.

Over all the trends are mixed with the sales and profitability showing signs of improvement, the balance sheet while continue to remain strong is showing early signs of quality deterioration and the quality of financial statement disclosures continues to be a miss.

See the results here

Thank you!

AJ

Disclosure: Invested.

7 Likes

Disclosure: Tracking

6 Likes

Good extracts, @Lajja_Shah. As they mentioned at the AGM, the company seems to be delivering on the growth numbers and sharing more details in the presentation. If they can repeat the recent quarterly run rates or the numbers they are guiding for, the stock is trading at 5-6 PE multiple (the credit rating report also hints of strong order book and growth) and turnover would be much higher than what it was 3-5 years back. The concern remains the deterioration in balance sheet quality in terms of receivables and inventory along with fall in margins vs 3-5 years back…though the receivables have increased for everyone in the industry. Market has lost complete trust on this company, don’t know if the same would be regained. The stock had got PE multiple of 40+ at one point of time. Interestingly since then, the interest cost has fallen from 20 Cr to just 3-4 Cr pa (co is kind of debt free)., company continues to pay high taxes and there has been zero dilution.

Disclosure - Invested

12 Likes

I have performed a few checks using the data source from screener

Check 1

Expanding Profits or decreasing Profits ??

mar 17 Mar 18 Mar 19

Raw material cost 38.64% 45.59% 46.61% ( expense increased squeezing profits )

Cash form operating activities 44.66 cr 28.62 Crs 8.56Crs ( Where is the cash ???)

Export incentive 6.84% 5.56% ( It is decreased )

Job work charges 1.24% 1.42% ( expense increased squeezing profits )

Check 2

where is the company’s focus : company is focused on value added products

Readymade garment as % of sales 91.77% 92.82%

Check 3

is stock popular or cornered ?

Price to Sales ratio/share 2.66 2.68 1.12 (INVESTORS is wiling to pay premuim per Rs Sales) i.e pessimism among investors about the equity

Check 4

What is driving EPA is it WACC or ROIC ?

Invested Capital 452.23 497.7 652.22

RoIC 22% 15% 13%

WACC 12% 12% 12%

So EPA (Economic Profit Added) 43.96 14.08 5.62

observations : RIOC is pulling down the EPA … result something is missing to achieve effiecency in operations

Check 5

Dhikra rokra kidhar gaya ?

Borrowing increased 0.92 86.68 i.e 9321%

whereas the fixed assets increased YOY growth 23.75%

investments decreased 9.02 0.07 i.e -99.22%

Cash form operating activities 44.66 cr 28.62 Crs 8.56Crs ( Where is the cash ???)

Export incentive 6.84% 5.56% ( It is decreased )

Free cash flow

Check 6 is company going to break ? i am not sure but the data reveals a trend

Altman Z-Score i have taken following weights

Working Capital/Total Assets 1.2

Retained Profits/Total Assets 1.4

EBIT/Total Assets 3.3

Market Cap/Total Liabilities 0.6

Sales/Total Assets 1

company is moving the grey zone as per Altman score last Five years Z score

5.57 5.01 4.74 3.64 2.65

Regards

Disc Invested this is not any stock recommendation to buy or sale , i am not any SEBI approved Analyst

7 Likes

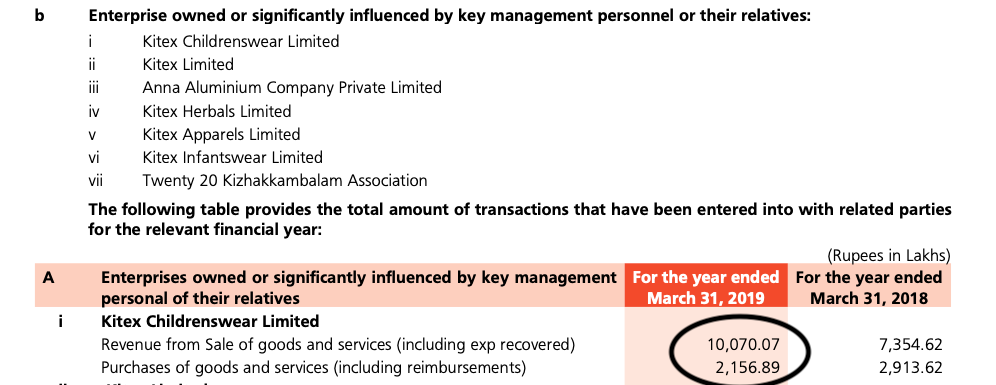

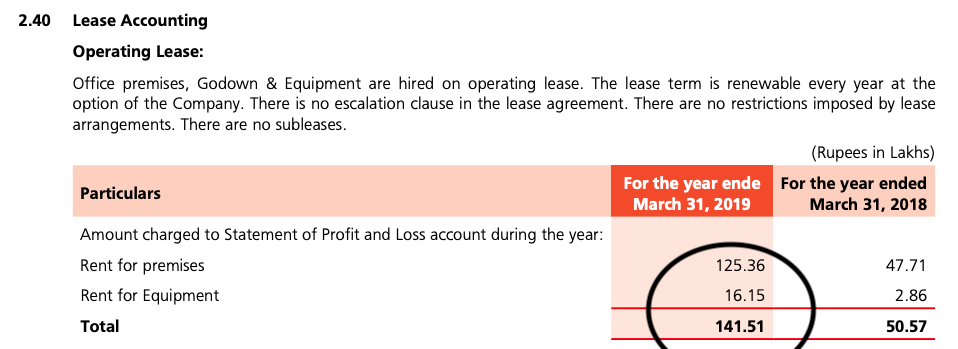

2 aspects to be brought to notice.

- Business with Kitex Childrenswear Limited is rising YoY.

Kitex Childrenswear is not a Subsidiary but here their promoters have significant influence. I am unable to get the AR of Kitex Childrenswear.

- Operating Lease agreement / payments are also on a rise (though the current figures might not be considered high seeing current scale of operations of the business) .

A note what are operating leases.

Another one is 50% of their sales is to their US Subsidiary .

Nothing particular about but just a few points highlighted to keep a note of while going through the business.

Disclosure - Not Invested but tracking

1 Like

Kites USA LLC is a sales office in US. Since last 2-3 years indian entity exports the goods to the US entity and this entity ultimately sells to the retailers (This structure is quite common in all exporting companies…eg pharma sector). US entity is a 50-50 JV between kitex garments and kitex childrenswear. (May b reason for JV is- both kgl and kcl can use it as front office for exports).And Kitex childrenswear is one of the promoter of KGL…though kgl and kcl into same kidswear…kgl’s debt is negligible compared kcl…

Major concerns what I feel is - increase in receivables, donations to the twenty twenty .which is quite high that too during CapEx cycle…drawbacks /receivables from govt . Project execution risk

Can anyone find the Financials of kitex children wear which should answer several questions. The website has no info i guess. Only will have to get it via MCA.

Since then, Kitex has gained a virtual monopoly over every aspect of public life in the village—from laying roads to directing the electorate to vote for a particular party in parliamentary elections. Its high form of populism is driving out politics from governance… that is, every strain of politics except that of its founder, Sabu Jacob, who is known simply as “Sir" or “Company Chairman" or the man who built the supermarket.

1 Like

kitex.xlsx (11.5 KB)

3 Likes

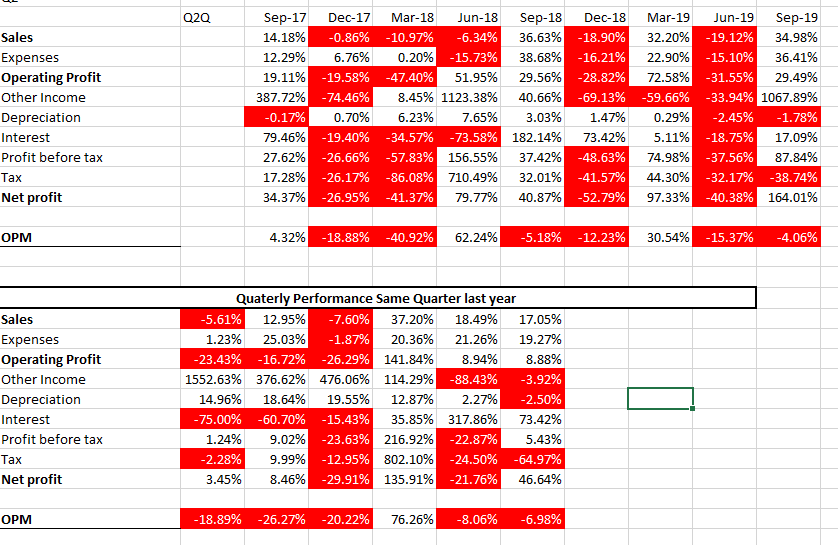

Looks like the maverick is back. Kitex posts good topline and bottomline growth (inspite of 10 crores reversal of MEIS).

For q3 fy 20, topline jumps from 136 to 250 crores and net profit goes up from 12 to 35 crores.

9M fy 20 eps 13 per share. Interim dividend of Rs 1.5 per share declared.

disc: invested as a techno funda bet.

kitex q3 fy 20.pdf (437.9 KB)

18 Likes

It seems operating profit for this quarter is lower by almost 19 Cr! had this govt retrospective reversal not come, results would have been even more spectacular. Anyways, despite substantially lower incentives, PBT for 9 months results is close to 20%. Also, there seems to be some inventory reduction in this quarter. Tax provision is still high. Seems finally what Mr. Sabu (whom most would not believe and continue to doubt etc) said at the AGM and for last few years is finally happening this year.

Also, if one keeps tab on their little star updates, it seems some interesting things are happening.

Lets see how sustainable is this. Has been a crazy thing.

Ayush

21 Likes

If one looks at the presentation of q2 fy 20 results, he has given guidance of topline growth of 198 crores for q3 fy 20 and 205 crores for q4 fy 20. He has managed to meet the guidance for the first 3 quarters (and surpass q3 guidance comfortably exceeding by close to 25%) . Coming to what he mentions in annual report, he aims to take company’s turnover to 2000 crores by 2024-25 which is a time period of 5 years from now and amounts to almost 3 fold increase in topline. That seems a tall ask and we all know what kind of claims he has made in the past and what he achieved.

But of late there seems to be less talk and more delivery from his side. He seems to have stopped concalls, even coming on tv etc seems to have reduced drastically. Shareholders would hope that this energy is channelised towards business which would result in good numbers.

Since there is a lot of disillusion with him and kitex among shareholders, it will take a few consistent quarters of good growth for the market faith to return to some extent As of now, a once 50 PE stock is available at below 10 PE based on FY 20 estimates inspite of decent numbers in the face of MEIS writeback headwinds. . I think in the coming quarters this write back of MEIS would not be there because as per my understanding, the write back has been done by most companies. Last two days have shown huge volumes along with price rise, so lets see where this is headed. Personally I have been positively surprised by the net profit numbers, Including the MEIS writeback this is a huge jump in profitability.

Technically 200 week moving average which is usually support during downswing for good companies in market favour, is at 177-180. In this case it might act as a temporary resistance. Beyond that the bigger resistance can be a falling gap at 197-220 which needs to be monitored.

16 Likes

We should be careful while analyzing the numbers of Kitex. I have highlighted this in the past and let me reiterate - the consolidated financial statement should include the share of profit/loss of the associate entity in US and this number is shown as “Nil” -which i’m sure is incorrect considering most/all of Kitex’s sales in US is channeled through this entity. Note that the US entity has consistently reported loss from the time it was incorporated(9.8 Crore is the loss reported last year).

Also note that all sales made to an associate entity is recorded as normal sales in the financial statements. We also have no idea of the amount of inventory as well as receivables in the books of the US entity.

This should be highlighted to the management (hopefully some of you might have access to them) and get rectified. Not able to understand how an audit firm of International repute like BDO not look into these aspects before signing off the limited review report.

AJ

Disclosure: Invested.

10 Likes

Yes, Kitex has been one crazy ride.

Have been holding 2 Kerala based companies(Manappuram and Kitex) for last 5 years and each of them behaved in such diametrically opposite fashion.

When I look at the biz and stock performance of Manappuram - I feel like I have become a better stock picker.

But when I look at the stock performance of Kitex - I don’t know where to hide.

Market has its way of keeping you grounded and humble.

On a serious note, this Dec quarter results seem to be very encouraging. The research reports which kept saying( in the last year) that they have good order book seems to be finally materializing in terms of financial numbers.

@ayushmit

Also, if one keeps tab on their little star updates, it seems some interesting things are happening.

Regarding your above statement, are there any new updates you are aware of regarding Little Star? Thanks in advance for your response.

Also, it would be interesting to look into their receivables and inventory after Q4 results. Also, interesting would be to see the financial performance of KCL at the end of the financial year.

Hoping these numbers sustain. Also, need to understand the long term impact of MEIS reversal - Can it be passed onto customers without much trouble?

5 Likes