Anyone planning to attend Kitex AGM on June 4th.

Would like to meet up.

Anyone planning to attend Kitex AGM on June 4th.

Would like to meet up.

Kitex is a very interesting story.

Most of us now own Kitex and many of us also doubt many things about Kitex, like integrity of management, quartely numbers, auditors, gross margin numbers , why so much cash in current account, why in $ not in rupee, some even call it Satyam like case.

Only time will tell whether all these doubts will get cleared or increase with time, now one thing is getting clear that Mr. M might have started liking and trusting the numbers. As they say it may climb its wall of worries, which can be a good thing for stock as it may never be over owned due to these concerns.

Disc : invested, view are biased

@sethu,KITEX -according to the latest report from the KITEX WEBSITE is the second largest apparel in the world.(so no longer 3rd)- another feather to its cap-

A part of the renowned Anna-Kitex group of companies, founded by the legendary Late Shri M. C. Jacob, Kitex Garments Ltd is the largest employer in private sector in the state of Kerala. It is located near Kochi and has easy access to sea and air ports. The company was established in 1992. With unmatched global connections, this company caters to prominent and renowned conglomerates in USA and Europe. The company currently employs over 7000 people at its facility, and has been a business provider to many satellite businesses in the state. Having started with INR 1.8 Crores turnover in the year 1995-96, the company has now grown to a turnover of over INR 524 Crores in 2014-15. The company is currently the second largest producer of children’s apparel in the world, and is now in the process of setting up operations in the United States of America.

@Sinha, I was reading the Thoughtful investor- by Basant Maheshwari- pg no 185, while it is important to be cautious on management pedigree is is also essential not to be unduly suspicious unless an investor has serious reasons to doubt the integrity of his promoter, in the absence of any indication to the contrary an investor while evaluating the mgmt. shld generally follow the theory that a person is innocent till proven guilty because most of the debate on mgmt. quality happen around the small cao whose potential for gains remain multifold and hence the costs of exiting an investment due to FAULTY Judgement is very high. when I discussed these concerns with one of my colleague(visited factory) he said its atrocious to compare KITEX with SATYAM…shri M.C.Jacob was a very visionary leader in kerala,on par with yousuf ali, varkey group etc…lets see how the kitex story unfolds!!

Kitex Garments trading at a rich valuation of 46 PE.

Does bigger means better pricing power ?

Have you find any supplier of Walmart in fortune 500 list ?

Just Curious.

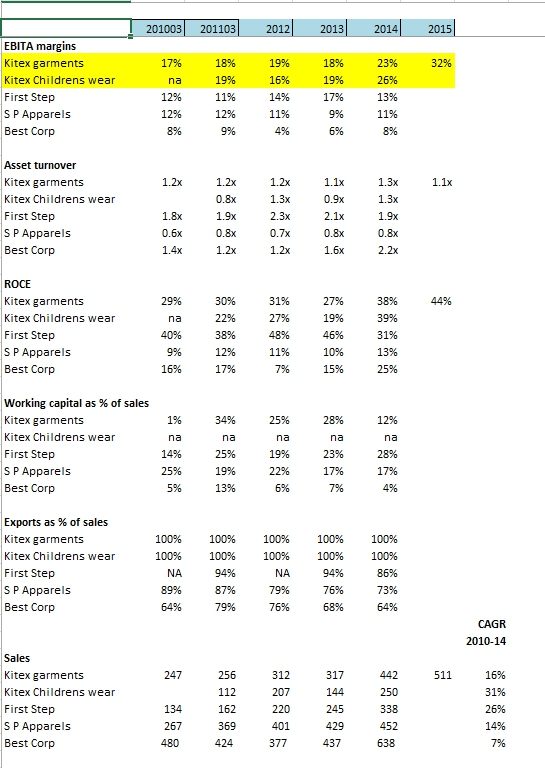

@Donald, it might be late but could be still useful… peer comparison of companies who identified few months bac

This is what I noted in my diary:

**

**

Mgt gives quite aggressive guidance. Unable to digest that EBITA margin of 30%+ in 2015 is sustainable, but mgt insists that its sustainable. Its due to productivity gains and not decline in Raw materials pricesMgt is entering diversifying into whole sale segment which is the natural progression from being a manufacturer, but it also means risk of going completely wrong, but if sucess this will put the company into completely different orbit.Valuation projects 25% CAGR for next 10 years and EBITA exit multiple of 20xi suspect that mgt is diverting KCL income into KGL. Imagine once KCL gets listed [mgt said exploring option in AGM] can he buy fabric from outside for KCL

while using captive fabric for KGL… there must be other reasons like

this for low profitability of KCL over KGL… [In Mar 2015 conference call mgt admitted KCL sales flat and margins lower than KGL because its buying fabric from outside]

Relying on two things 1) Not judging mgt by single instance 2) His reason to exist is Kitex Garments and probably 30% margin is sustainable and he will be able to diversify successfully into whole sale segment.3) He could infact really diverting KCL income to KGL but it could be one of his fault, lets ignore that…

Disc: Safe to assume vested interest… Not recommending a buy at this price, am personally will not buy at this price but will not sell either…

Who all are attending AGM starting today, it will be an interesting AGM with too many questions to promoters, esp on 200 Cr Cash in current a/c etc, People are expecting 1:1 bonus also, Let us see how it turns out.

I am expecting atleast @ayushmit, @Donald and few others will be attending for sure.

Hi,

I had attended the AGM. Here are the notes. Everything was noted down in a jiffy…do cross-check for errors.

AGM speech - Mr Sabu Jacob

Kitex has 98% business from US. US retailers have become profitable with their profits growing 5-25%.

Infant garment players are clocking big growth - Carters sales grew from 2b$ to 3b$ in a year. The Children’s Place is adding 100 stores per year and Dollar General (lower end) has plans to add 900 stores a year.

Target is the second largest retailer in US. Kitex has taken up a “special” project for them to supply “fully” organic garments. So far manufacturers had organic certification only for yarn. Kitex is the 1st in the world to have organic certification for processing and garmenting. We will get the certification in couple of days.

Our technology is not just state-of-the-art…its different. Nobody offers natural processing of cotton. We don’t use steam and do not do chemical processing. Dyes are naturally absorbed. Have the only plant in India which does yarn dyeing instead of fabric dyeing.

Another large buyer (cannot name now) is also in advance stage. Kitex in a position to offer special/specific requirement based projects to clients due to its unique backward integration and technology prowess. Signed up a New York based designer for “different” designs for a a client. This kind of business will make our sales less seasonal and stable.

US com registration already done. First sales in fall 2016 (March 2016) under own and pvt label brands. Is in final stages of completing the contract with a very famous brand for pvt label. In CY 2016 10m$ sales expected under pvt label (I think he meant 5m$). Also registered own brand. This is expected to have $5m sales in CY 2016. Both the above are then expected to grow at 5m$ additional business every year. The new capacity will be used for direct US business.

Now clients are doing logistics, we will take it up and save 2% margins.

Q&A with Mr Sabu

Organic edge of Kitex - by 2020 all 18 metals will be banned at-least for infant garments. Kitex is the only player already there implementing this.

Have plans to do backward integration into spinning yarn. Yarn is low profitability business with manufacturers making loss at times. But own yarn spinning will give Kitex many advantages, We can import US cotton (duty free) and use that for making yarn. This is 100% better quality, has no contamination (due to mechanized harvesting etc), the fiber is longer and will lead to lower wastages. But spinning foray not finalised. Even if we are starting we will do in stages. For current requirement about 35000 to 45000 spindles capacity required. Can start with 25% of that and then keep adding to reach a full capacity of 80000 spindles. This 80k spindles capacity will need 150 Cr capex. Not decided whether to put the spinning unit under KCL or KGL!!!

US company will be 50% owned by KGL and 50% by KCL. US company will give direct savings on logistics (client using their own set up spends around 6000$ for a 50 lac worth consignment, we can do that under $4000) for existing FOB business. Win-win for clients and Kitex. But no own wearhouse in US for this. Third party logistics will be employed.

Pvt label products to be sold through wall-mart and Target. Own brand will be sold through outlets where Kitex has no presence currently - Rose Stores, TJ Max etc. Pvt label will have royalty costs of 5-7%. Internal target is 100m$ sales in 5 years from direct US.

KCL 200 Cr sales and 22% PAT (not sure). Merger not finalised…also considering listing of KCL. Has meeting with E&Y this week, will look at various proposals. Investors had complaints on transparency, once KCL is listed we believe transparency will be there for KCL as well.

E-Com business in US can be big in the future. Will start E-com sales also in CY 2016. Estimates that upto 70% business in US retailing could be through E-com by 2020.

Last year volume was slightly less than previous year. The value addition was higher, hence number of pieces reduced. This year the mood is again to lessen embroidery and hence volumes could be higher.

The cash in dollars is not abroad. It is in SBI EFC account but not converted to rupees. We are very sure that dollar will appreciate…US interest rates will increase. Already getting forward contracts at 68. (defended vehemently that dollar will appreciate and com will benefit).

Existing business will grow at 20% with additional capacity to be used for direct US business.

Has an agreement with textile ministry under training scheme. Ministry will pay Rs 15000-20000 per new recruit for their training for a maximum of 400 new recruits per month. This will take care of training costs…already started and already getting the funds.

Margins will not fall below last years 33%…will only improve.

Thanks @Vedant for your beautifully written AGM summary. It seems most of the doubts are cleared now.

The story it seems will be fully unfolding in next two years, whatever we have seen is just beginning of this fantastic journey of value creation for all stakeholders.

Cheers

Santosh

Hi Thanks for the notes,

Mgmt had earlier indicated merger of both entities but looks like they are going back on it.

while transparency can increase due to listing of KCL wouldnt it mean they will 2 sets of share holders to answer to? Is this because they would get better valuations for KCL now?

Little unclear on the same, hope senior investors can help,

Thanks

Shankar

Hi, does this mean demerger of KCL? will it mean existing shareholders of KITEX Garments get free share of KCL? please clarify…

The US venture will be owned 50:50 by KGL & KCL. Does it mean that Mr Sabu is trying to get a bigger piece of the pie? The way I understood the structure was that KCL was supplying to KGL which was creating the final product. If this understanding is correct, then why have a 50% ownership of the US entity with KCL?

Hi,

KGL fabric division sells fabric to KCL, but KCL is involved in the same business of infant garments and caters to the same US market. KCL factory is new where-as KGL one was built in 1995. Capacity wise both are equal…just that KCL needs to reach its full potential.

As per MD each company has its own management team though they operate out of same compound (65 acres out of which KGL will be 35 acres or so) and have distinct set of clients. In his mind there is more than enough business for both and hence there is NO issue of which client is allotted to whom etc

I am just hoping they merge. Imagine spinning unit coming up under KCL. KCL would sell yarn to KGL with which KGL would make fabric and sell to KCL and both sell their garments to US market

And if spinning comes up in KGL there would be more complaints of the lowest margin businesses being under KGL - spinning and fabric.

When-ever the MD speaks he always speaks with KGL+KCL as one unit. For example its not true that the listed entity is No 3 in the world…its the KGL+KCL combine that is No.3. Same with capacity (5.5 lacs), number of employees, client list… Investors think he is talking about KGL!!! But to be fair to him, I think its just his natural way of talking and does not realise that analyst or investors are asking about the listed entity only. So whenever you hear him or read about “Kitex” do not assume its about Kitex Garments Limited.

@Vedant …crucial Q…how will the existing KGL share holder benefit due to merger? was that clear?

Unless we know the exact terms of merger it won’t be crystal clear. But its easy to view the merger as beneficial for share holders as the combined entity will be much stronger and bigger with higher participation from institutions, the corporate governance concerns related to inter company transactions, conflict of interests etc will vanish and as a result valuations might be better.

Agree. The only concern is if KCL listed separately and all the low margin businesses ends up with KGL.

Dear Vinod,

You have captured all the relevant informations.Appreciate it and thanks.

Rz

Shanid VH

IMHO I would consider this political participation, as another CSR initiative.

Key thing being that, they have NOT floated a party.

Highlighting the key points from the article -

Plans to field independent candidates in all 17 wards of Kizhakambalam panchayat

As Kitex Garments’ plant has been denied a permanent licence by the Kizhakambalam panchayat despite fulfilling all criteria, the group has launched a charitable mission that has invested around Rs 28 crore in the last two years to usher in unprecedented development in the panchayat and to emerge as a credible alternative to the entrenched political parties in the area.

Under the aegis of Twenty20, a body registered as a charitable institution, the group has upgraded a whole lot of civic amenities ranging from drinking water plants and roads apart from providing scholarships and medical expenses for the needy. Interestingly, the total spending by Kizhakambalam grama panchayat in the past four years stands at Rs 22.4 crore, less than half of what Twenty20 has spent in two years.

In fact, Twenty20 has become so popular that it has even won over many converts even from ideologically driven cadre parties like CPM and CPI. Members of AITUC, the trade union wing of CPI, have actually gone a step further and publicly display the Twenty20 badge on their shirts.

"Of the 8,000 families in Kizhakambalam grama panchayat 6,700 families have registered with us. While entering the third year, we have spent around Rs 28 crore for development projects and welfare schemes for the residents,’’ said Sabu M Jacob, chief coordinator of Twenty20, and Kitex’s managing director.

Twenty20 is registered as a charitable society under Travancore — Cochin Literary, Scientific and Charitable Societies Registration Act 1955. To avail benefits offered by Twenty20, a family should register with the mission which then issues it a card. The society issues blue, green, yellow and red cards to villagers based on their incomes. Nearly 71% or 4,627 families fall under the red and yellow categories — low income and below poverty level respectively.

To ensure transparency, the mission has a three-tier system. All projects have to be cleared by an 18-member executive board comprising politicians, a retired professor, a retired bureaucrat and local businessmen. Before it reaches this committee, the proposals are vetted by 17 ward-level executive committees and a 200-member ward level-working committee.

Disc: Invested.

I am struggling to understand how Kitex has a less riskier and more sustainable business model than Indo Count Industries whose 75% revenues are from bed linen sales to global clients like Walmart, House of Fraser, JC Penney etc.

Comparisons that come to mind are as follows:-

I haven’t done any research on Indo Count… But from the post above, I am tempted to ask…

If Infant wear is such an extremely value-enhancing proposition - then why doesn’t Indo Count expand into infant wear?

It already has scale of operations - so it can match the low cost advantages of players like Kitex

It already has relationships with various MNC retailers - so it can easily get its existing customers to switch from Kitex/competitors to itself

The other way to put the question is — How difficult is it to replicate the low cost advantage + switching costs advantage of Kitex (the two competitive advantages that Prof. Bakshi attributes to KGL). How sustainable are these advantages?

And if these are not sustainable, and the fabulous results in the last couple of years is primarily due to low cotton prices - then is Kitex not overvalued? Add all the concerns about management and corp governance - it seems like a ticking time bomb to me.

Disc - not invested