I found it very strange when the MD said that the money lying in EFC account has not been converted into rupees or has not been put into any other interest bearing instrument as they expect the Dollar to appreciate and wish to convert once Dollar appreciates.

Ialways find it weird when the managementintentionally tries to makesome gainsbecause of forex movements or risky treasury income. It becomes a bit irritating to hear such a reply when one is a shareholder of that company.

@HR very disappointed to see the attitude. I don’t believe much in this kind of un-hedged strategies. What happens, if suddenly INR appreciates a bit and goes against the wind in the short run.

I am also disappointed by the performance of the stock. I got here late and I see it giving up the gains too quickly, even when when the market rocks

Ialways managementintentionally tries to makesome gainsbecause

This is plain currency speculation. How much is the amount involved? This is sort of stupid behaviour which led to blow up of many mid-caps’ balance sheets during the last crisis. They should have transferred to India and invested in mutual fund if they really want to get higher returns.

However, it could be ignored if the amount is too small to matter.

Kitex result was not bad,in fact it was a good result with superb margin.But what is interesting is the management commentary on sustanance of margin.They seem to have improved internal efficiencies and thus better margin.

Everyone comparing Kitex with Page,but don’t expect every year 20-25 % top line growth from Kitex .There will be a period of consolidation after every expansion.

I expect 10-12 % of top line growth for next year and zero growth for FY 17,hope they can complete the next round expansion by FY 17, then FY 18 should be a bumper year.

How market reacts to these scenario is a thing to watch,any correction will be an opportunity for long term investors.

Pl refer Sunil comments on increase in Authorised share capital from Rs 5 Cr to Rs 25 Cr. Will there be any rights issue? how will impact the share price going forward?

The key takeaways from the concall were as follows

Mr Sabu Jacob guided the revenues will grow 100% over the next 3 years. He guided 20-25% growth for FY16, 30-35% for FY17 and 40% for FY18.

E&Y has not submitted on the proposed merger between KGL and KCL. MD assured it will be done in a manner keeping the interests of both sets of shareholders in mind.

Majority of the questions were directed towards the company’s ability to sustain the current margins. The reasons for it and if it will sustain in the future. MD as usual told it was due to new machines, technological advancements and so on. He opined that raw material is not a major contributor to this high margin. As a result, he was of the strong view that current level of margins will sustain in the future regardless of future raw material costs.

They are in talks with a private label in US to launch through private label by paying royalty. Talks are going and first shipment may begin by the end of this year.

Overall, there were lot of positive vibes from the call. If the promises are met, Kitex will keep rocking.

Kochi-based Kitex Garments and Andhra Pradesh-based Redox Pharmaceuticals and Jagruti Foundation have recruited a total of 1,000 candidates on the initial day of the drive aimed at generating more employment opportunities in the country.

The selected persons will be provided placements at different units of the companies after imparting 3 to 12 months training in various skills. Post training, the company will accommodate the candidates with full salary adhering to the Central Governmentas labour laws. During the training period, the government will provide food, accommodation and transportation free of cost to the selected youths. According to DDU-GKY state coordinator Abdul Azad, despite 2,575 vacancies only 1,000 candidates were eligible to be recruited on Monday.

aMore aspirants are expected to get jobs in the selection drive to be held in the coming days,a he said.

Kudumbashree is the state recruiting and monitoring agency of the project being implemented jointly by the Union Ministry of Rural Development and the state government. aAltogether 30 companies have been enrolled under the DDU-GKY so far. The recruitment will be held at various districts in the coming days. In Alappuzha alone, more than 6,300 candidates have been registered,a Azad said. While Kitex will commence the training programme for the selected candidates in Ernakulam from May first week…

Sabu Jacob new proposed remuneration is 68% higher than current. However it is mentioned that any year it cannot cross 5% of net profit. Still it looks on higher side.

Other directors proposed remnueration also mostly >40% higher than current.

Related party trasactions

Cash is sitting idle in bank account while company is paying debt interest without pre-closure plan. Interest rate is 12.40%

Software aka Intangible asset is almost written off. Beginning value of 336 lakh ended with 35 lakh value! 90% depreciation ?

Overall asset allocation is poor.

In Other Income section, Foreign exchange gains stands at 10.7 cr. In the same AR company says, it says company doesnt use the foreign exchange forward contracts for trading or speculation.

Well could not resist to follow up after going through Annual report for FY15. Find enclosed my observations:

No where company mentioned about realisation or volume. So the only way to use quasi indication is power consumption which has grown by 29% during FY15.

Please go through segment wise numbers in Annual report. In addition to Jump in PBIT margin in Garment from 30% in FY14 to 36% in FY15, what is interesting to note is turn around in fabric business from -10% in FY14 to 4% in FY15. If we adjust intergroup transfer from fabric sales, nearly 97% of outside sale is to Kitex Childern Wear and Kitex Limited. Same was 84% for FY14. So what factor contribute such turnaround with no change in client is worth exploring.

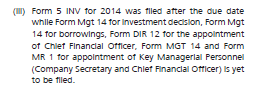

Refer to PAge 55 of Annual report in Secretarial audit report. The company continue to miss timeline on various regulatory filing with ROC

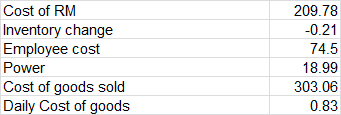

Finished Good inventory at RS 0.81 Cr is less than 1 day of Cost of Sales. Cost of sales calculated as under for FY15

Cost of RM 209.78

Inventory change -0.21

Employee cost 74.5

Power 18.99

Cost of goods sold 303.06

Daily Cost of goods 0.83

Page 74 Shows Balance in Bank in Current account at Rs 199.39 Cr as on March 31 2015. Why so large fund kept in current account? Even at 9% Fixed interest, average current account balance of Rs 150 Cr (31-3-2014 Balance 98.5 CR) , the company has lost Rs 13.5 Cr of interest.

Page 77: Interest on other than borrowing Rs 1.19 Cr during FY15 as against 0.56 in FY14. On one hand we have great liquidity of more than 100 Cr in current account, on other hand we continue to pay interest on other than borrowing (Which is for what purpose?). Need further understanding.

Please check contingent liablities specifically with reference to EPF delay. The company appears to face major problem in this area.

Page 89 give impression that company internal auditor as same as statutory auditor.

As per Chairman Letter, the company intend acquire/expand into backward integration. (Page 9 Annual report)

Missed to mention, even in FY15, Director Report and Auditor report are signed on April 4, 2015, i.e. just in 4 days of closure of year. This with delay in ROC filing continue remain an issue which needs further exploration in my understanding.

flags in Kitex AR

flags in Kitex AR and if we find ethical growth minded management then nothing like that.

and if we find ethical growth minded management then nothing like that.