I stumbled across this business as a technical find, however ended up researching about it and thought of sharing my findings.

OVERVIEW:

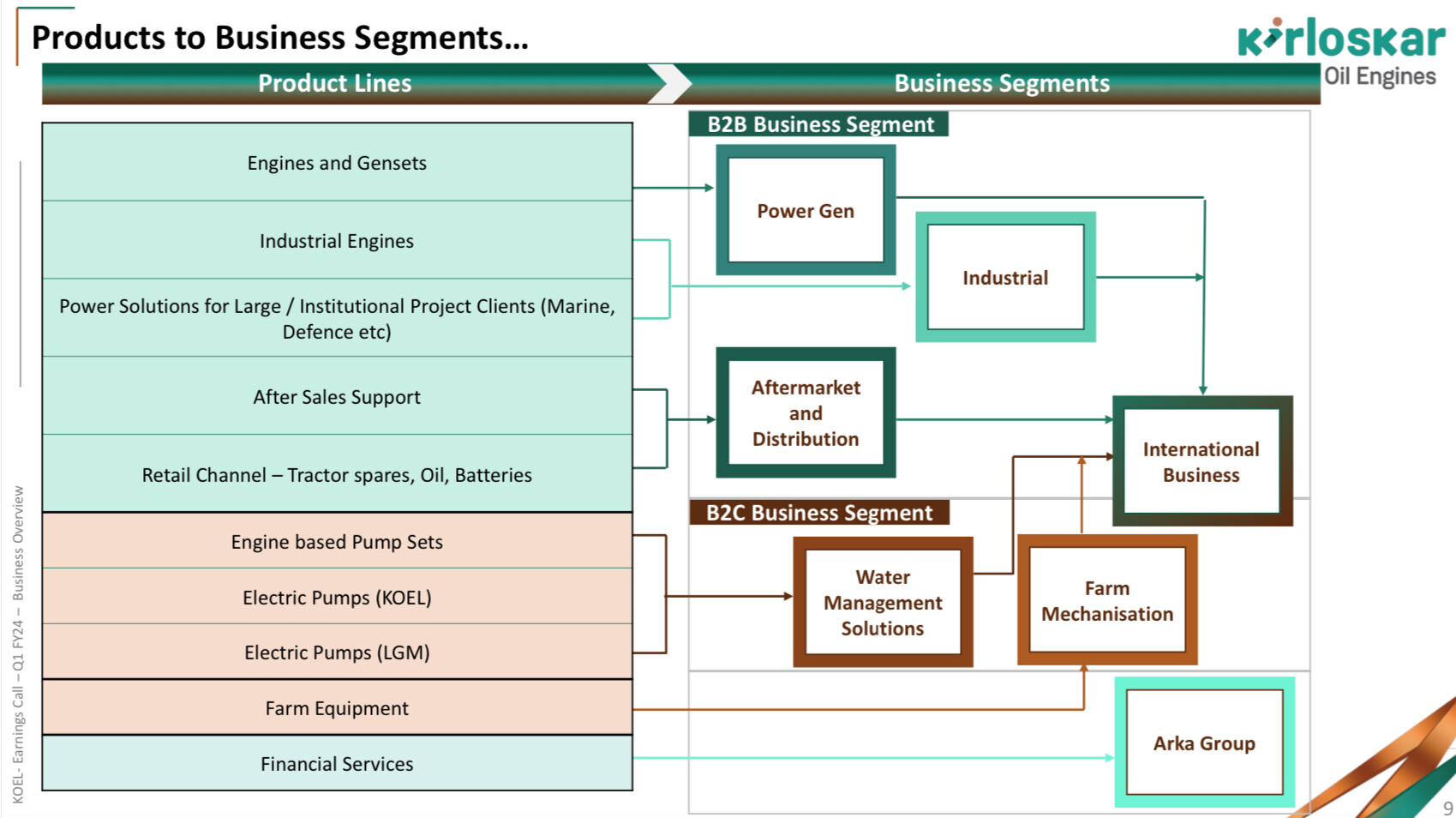

Kirloskar Oil Emgines Ltd’s business is divided into three segments

- B2C

- Engine based Pump Sets

- Electric Pumps (KOEL)

- Electric Pumps (LGM)

- Farm Equipment

- B2B

- Engines and Gensets

- Industrial Engines

- Power Solutions for Large / Institutional Project Clients (Marine, Defence etc)

- After Sales Support

- Retail Channel - Tractor spares, Oil, Batteries

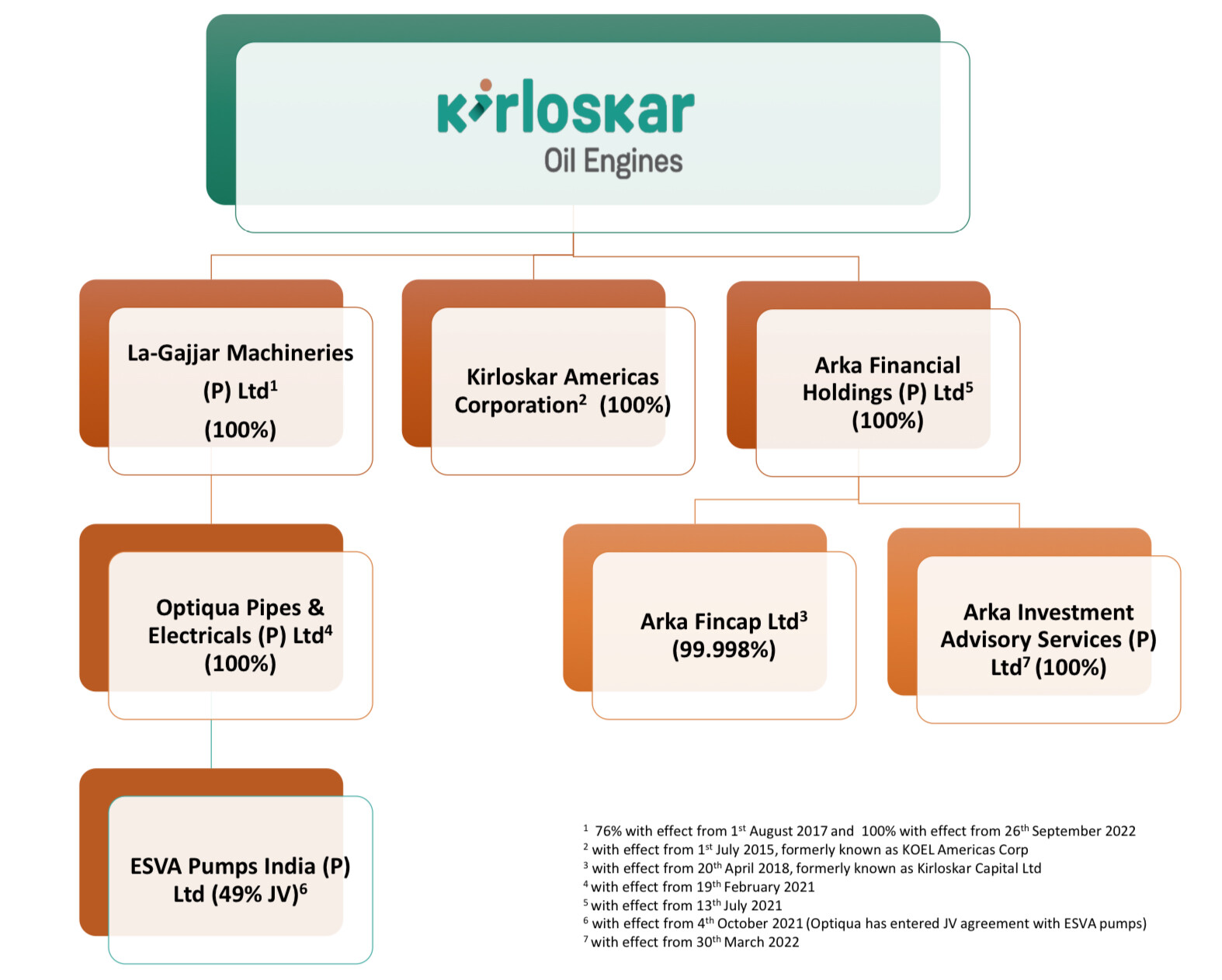

- Arka Group - Financial Services

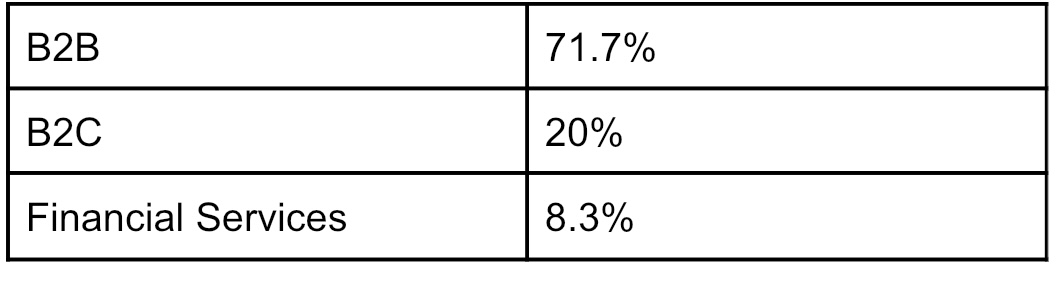

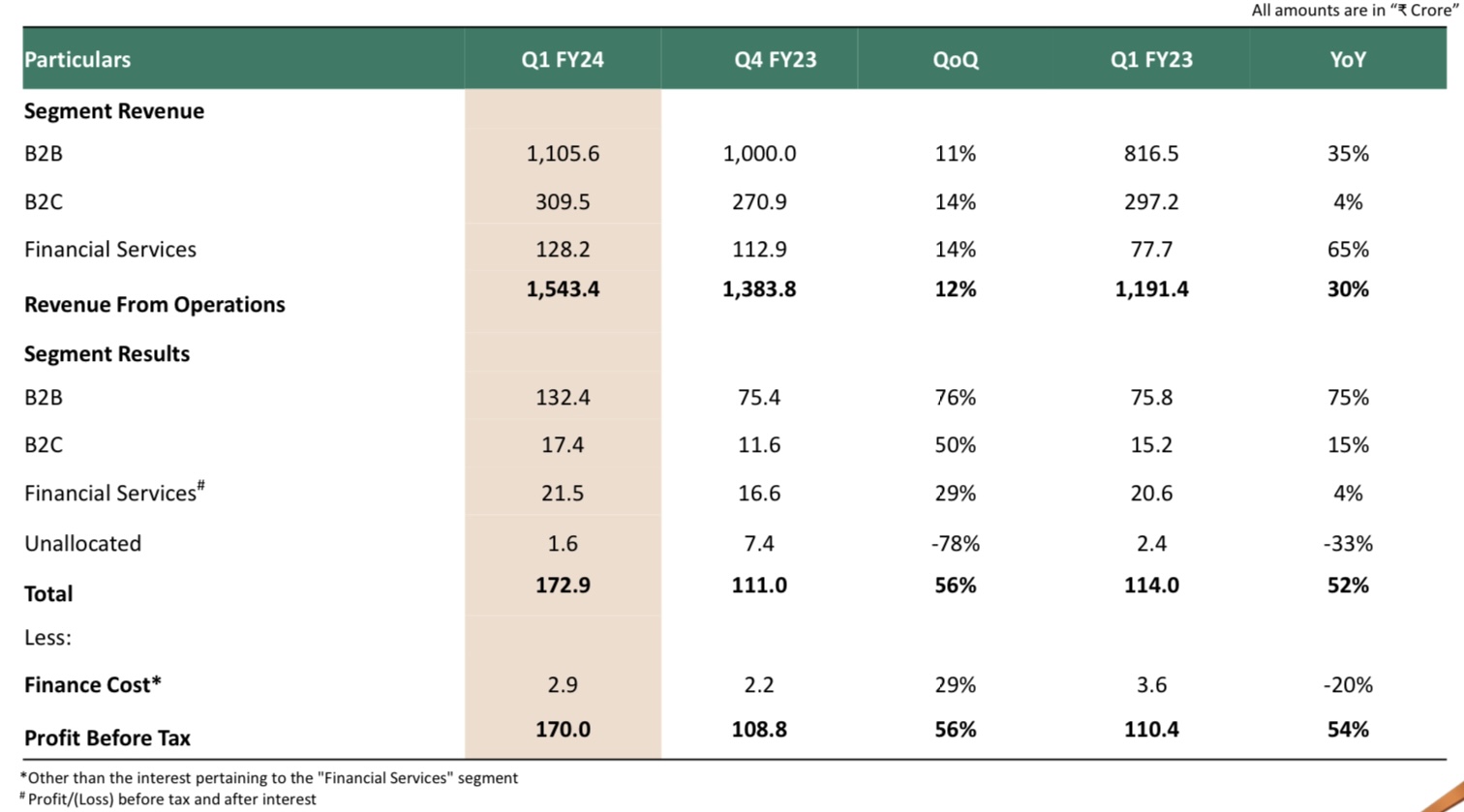

As per the recent Quarterly results; Q1 FY2024, the revenue % breakup for each segment:

-

It’s customers in the B2B business are predominantly from industries like Power, Telecom, Railway, Infra, Railway, Defence and also Data centres

-

B2C customers include ones from Agro and Irrigation

-

Arka Group is a NBFC with focused lending in sectors like real estate, Coporate lending and SME lending (initially started with 500 crores, to diversify business; had very strong and robust balance sheet, and maintained healthy cash positions)

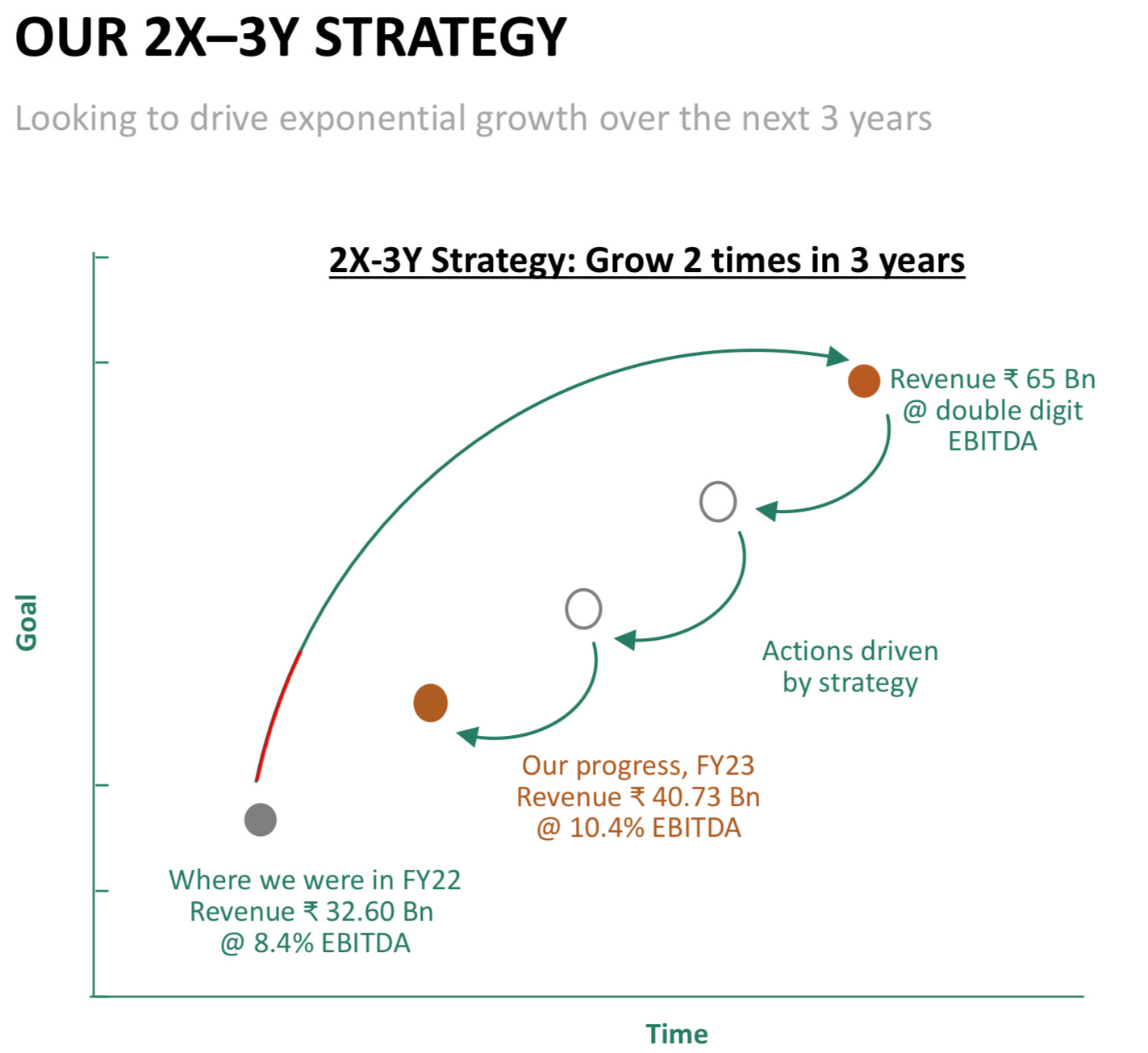

The management had planned for 2X-3Y Strategy; Double the topline in course of three years(indicating an avg revenue CAGR of 24%)

Concall Learnings:

-

It’s part of a legacy conglomerate - Kirloskar Group

-

Not interested in white labelled products

-

Management has shown decent control over fixed costs during volatile times

-

Management is very defensive in terms of its lending business

-

Managements focus on cashing out on the Value added Products

-

OEM’s usually place repeat orders

-

Acquisition of Optiqua (management is keen on water solution segment of its portfolio)

-

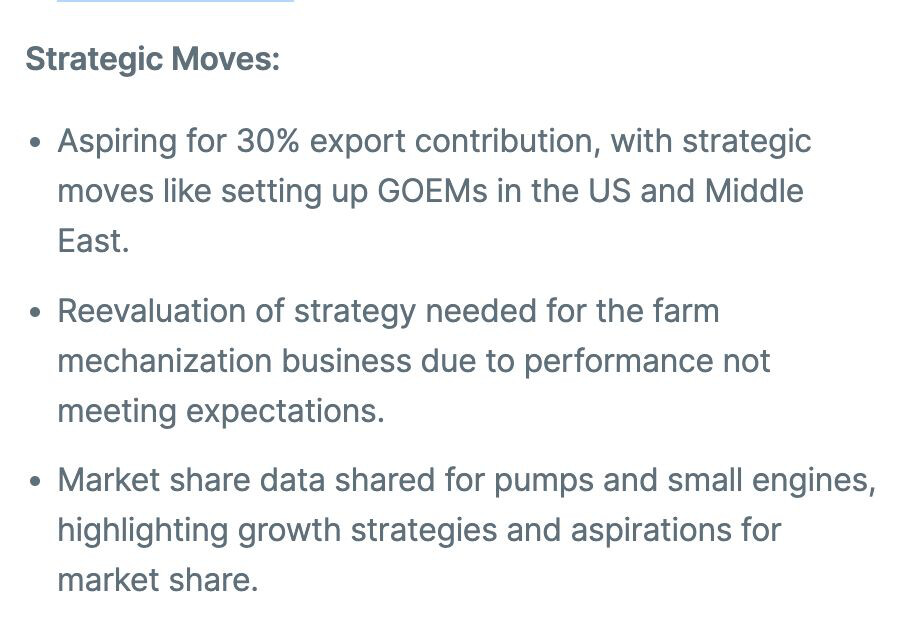

Focus on African Continent - delivering good growth in overall exports

-

A growing sales (also focus) in Ultra High Horse power Genset segment

-

The company is benefitted from both power deficit in the country and growing power needs due to infra capex and general population needs

-

Outlook for Q2 FY24 is cautious but optimistic, with potential for growth in new geographies and expanded product portfolio.

-

Commitment to 2X-3Y strategy to double topline in 3 years.

-

EBITDA margin of 12.1% is sustainable, with potential for improvement.

-

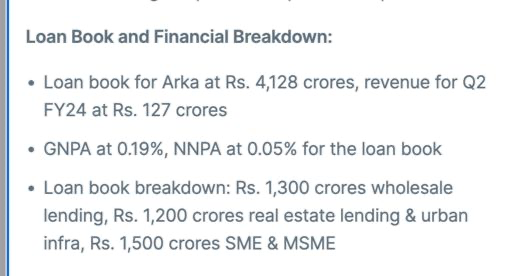

Strong performance in the financial services segment with a loan book of Rs. 3,656 crores.

-

Financial services segment experienced a slight decline in AUM, but expected to rebound

-

The company’s Financial arm earns a decent Fee income from Syndication as a third party participant

-

The management is not in a hurry to lend, wants to play a Calibrated move and play defensively for few years before becoming aggressive

-

the management has divided itself into parts, as in the case of different heads for each division

I’ll add a few more interesting concall excerpts below:

Challenges and Risks:

-

Decrease in profitability due to

-

Raw material price fluctuations

-

Decrease in order inflow

-

Mess ups in financial segment of the company

-

Decrease in demand for the Gensets

-

Competition from Chinese Players

-

The company also has a compliance burden; which results in the management to update many of its products accordingly

-

this compliance is Due to the Emmissiom Stamdards set by the government from time to time

-

Also in case of Fuel efficiency standards

Personal take:

Valuations are reasonable, although P/B is high. Personally invested in it. I’ll hold until there’s a constant tailwind environment

- This is my first time preparing a note like this, and I could have made mistakes(will correct if I find any)

- I hope to see some critical suggestions on the timeline

- My observations are not so redundant amd sought after as other professionals

- I’ve not not gone in detail for each product category (as in case of various Categories of engines like Low to Untra High Horsepower ones)