Kings Infra Ventures Limited is a focused aquaculture company with activities in aquaculture farming.

They are involved in the operations of shrimp hatcheries, grow-out farms, contract farming, feed distribution and other ancillary services related to aquaculture. They cover the entire aquaculture value chain right from broodstock to packaging, branding and marketing the end product. It operate aquaculture farms in Tuticorin, Tamil Nadu.

CMP - 135

P/E- 27

Website - http://www.kingsinfra.com/

PROMOTERS-

- Mr. Shaji Baby John, Chairman and Managing Director

- Mr. Baby John Shaji, Joint Managing Director

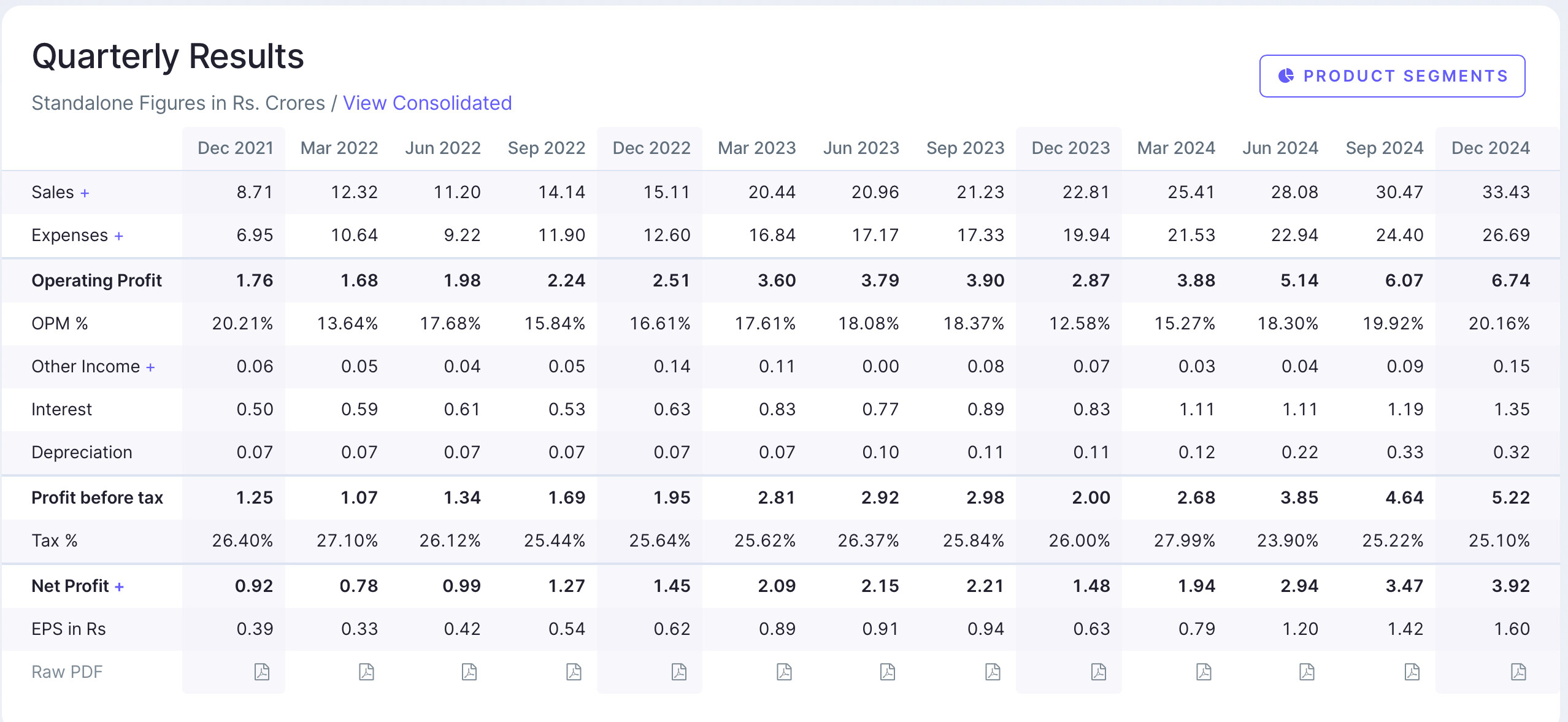

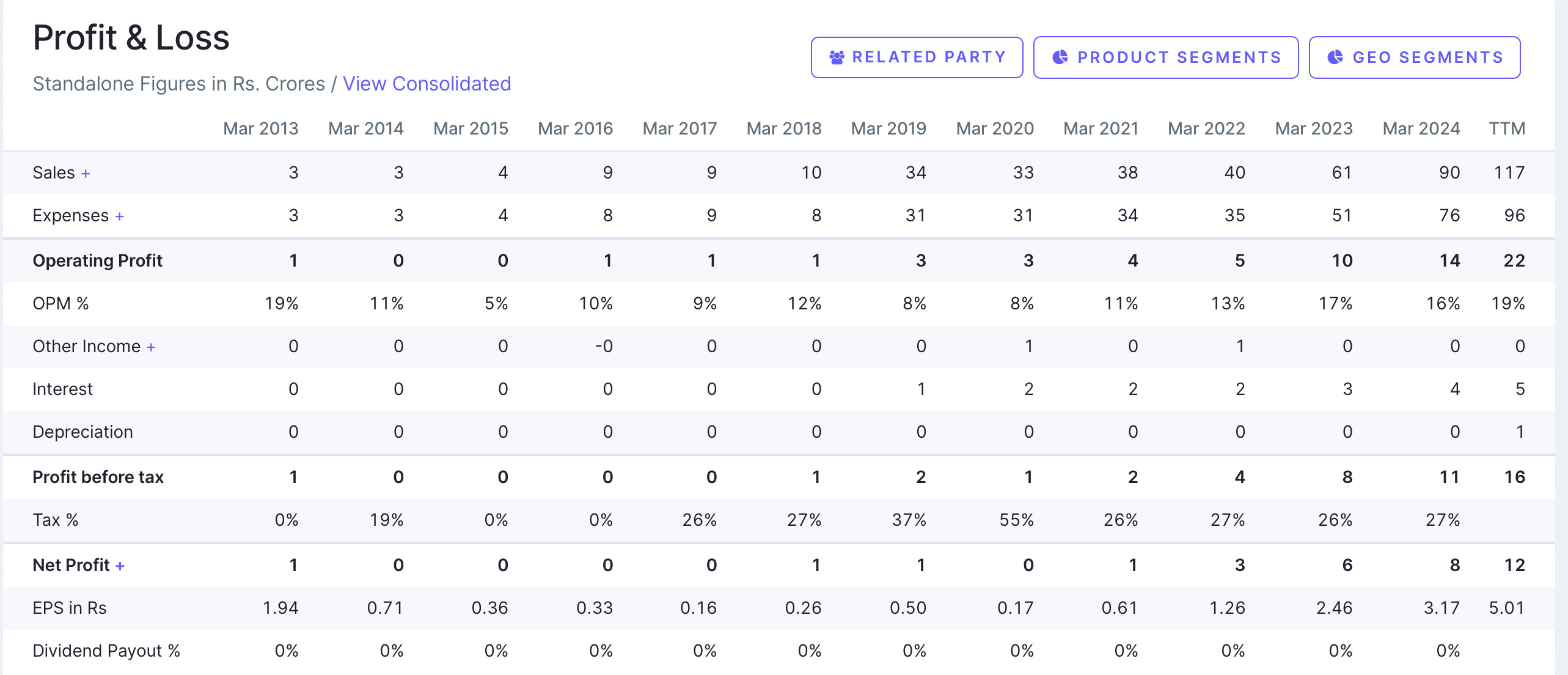

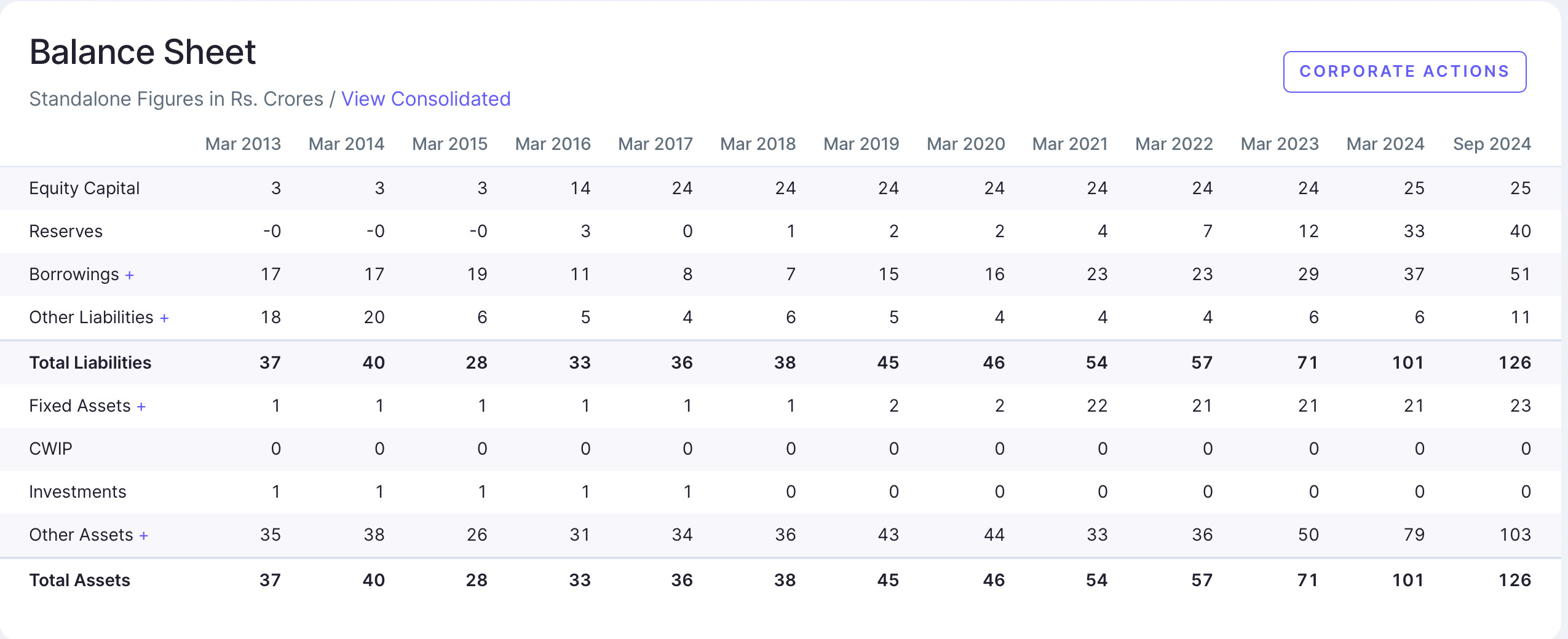

FINANCIAL HIGHLIGHTS-

Important Highlights -

-

Plan to launch a subsidiary in US to increase exports

-

Direct exports started in Europe via subsidiary in Spain. This is driving margin improvements as compared to exporting via intermediaries.

-

Maritech Eco park will add about 1600 tons in annual capacity once Phase 1 is completed in about 18 months. State-of-the-art technology which will drive efficiency and high output.

-

Exports to US had slowed down due to high working capital requirement in the past owing to introduction of countervailing duty. This is expected to improve once Kings launches a US based subsidiary in the coming months and will then help increase US exports.

-

Capex plans:

– 35-40 cr for developing 150 acres of aquaculture ponds (which should double capacity over 1-2 years)

– 20 cr for food processing facility (5cr govt subsidy available)

– Maritech ECopark around 170 cr for Phase 1. Out of this 24cr has already been infused. 36cr more to be infused via equity and 110 cr in Debt to be raised (Interest subsidy upto 3% is available via FIDF/NABARD)

– Kings Frigo + Bento (retail brands under Kings Infra Ventures Limited ) around 25cr to be funded via internal accruals over 3 years

-

Working capital requirement as % of sales should improve in the next 2-3 years as company starts exporting directly via their own subsidiaries, uses bill discounting and improves production efficiency via SISTA 360 technology

-

Company is working towards placing their largest shrimps (~80gm) in the high-end premium category in US supermarkets. This will enable them to fetch significantly higher prices (around 2x the usual) and thereby improve margins.

-

Company is aggresively looking to monetize its land parcels which are not in use. Management expects to fetch about 150cr over the next few years via this channel. This is a great boost for the company in terms of reducing debt and having sufficient working capital for growth.

-

Management expects to increase total capacity from 2600 tons in FY25 to 3400 tons in FY26 and 5500 tons in FY27. Capacity utilisation is expected to hover around 90%

Potential RISKS -

- 50% revenue contribution from China - Too much Reliability on China

- Due to Ecuador’s unsustainable and inefficient practices earlier, Kings Infra’s sales were effected. This may happen in future again.

- The land parcels that the company is looking to monetise may not turn into effect easily.

- They have an aggressive capex plan which will need a preferential round as well as more Debt.

Disclosure - Invested

5 Likes

Any foreseeable impact due to Trump reciprocal tariff ?

1 Like

Kings Infra has already shifted focus toward China and Europe. Trump’s policies may accelerate this realignment, compelling the company to diversify its export markets further rather than relying on the U.S.A. A squeeze of margins can be seen unless the company can pass on the costs to buyers or improve operational efficiency. Maybe a delaying U.S. market entry through subsidiary, overall we will have to wait and watch.

HOPE THIS HELPS

3 Likes

USA only contribute 4.3% of the overall revenue of FY24. Though management cautiously postponed to enter in USA market by 1 year.

3 Likes

Kings Infra press release.pdf (502.7 KB)

LATEST PRESS RELEASE BY THE COMPANY.

3 Likes

so the comapny updated few things, named it riding the blue wave

1] they have signed a collaboration with Aadhya Sea Foods (Andhra Pradesh) to strengthen shrimp sourcing and processing.

2] ₹150 Cr land monetization plan will unlock capital via joint developments/sales in Tuticorin, Kochi, and Bangalore

3] they have launched blue tech os which helps in monitoring real time farm,qr code trasnperency for clients,blockchain tracebility,automated compliance

4] leadership transistion, so this is the most imp one out of all as they are moving from family owned/legacy model to professional management model. so now we can hope to see a better and more structured version of the company backed by data driven decesions and more confidence by overseas investors or buyers their names are

Sreeram Inagalla → COO (International Business) – starting expansion from Dubai

Joseph Ragunath → Head of Domestic Operations (farms + processing)

5] so their main focus moving forward on broader basis are sustainable shrimp farming,growing exports,making their retail brands better, maritech eco park,Governance & ESG compliance.

3 Likes

Thank you @ca.ankitarathi for initiating thread on this company. Definitely looks interesting.

My only worry is that Receivables + Inventory as a % of B/S size is 56%. Any thoughts on this?

Already have a small qty as a tracking position

2 Likes

Negative news for Indian shrimp sector. Kings Infra for sure doing some great job but let’s see how things unfold in coming quarters

2 Likes

Lucky for them, their US exposure is not as high. Kings Infra’s focus on Tech and ready to eat segments is also something to watch for.

3 Likes

Exports to UK can be a new growth lever and lets see how management delivers

P.S: Invested recently and intending to add more on every fall

3 Likes

Unsure why managment release a commentary note on every international event. like UK FTA deal and now US tarriff these are latest. Even before I noticed they release a note upfront. I rarely see this kind of behavior in small/mid size industries unless they want to have a public exposure. May be I am interpretending wrong but previously some companies who are pump and dump showed similar trend.

P.S: Recently closed positions due to uncertaninities in the market and shrimp sector.

1 Like

i also have similar observation and a possible explanation is that the new professionals hired in this family run business have the drive to have more communication with investors. This can give more confidence to the promoters and to larger investor base as communications in promoter run bussiness is mostly lacking .

PS-Recently added positions and remain positive on the new innovations brought by company in reducing shrimp cycle time and margin of safety of un monetised land back of 1/3rd market cap at least.

5 Likes

Hey any view on company latest performance,they are growing topline and stuff but the cash flow is getting bad added with bad borrowings with high intrest rates and this looks kinda negative to me?(will reduce exposure maybe)

The sudden passing of the MD and Chairman led to a negative reaction in the share price. The Board has appointed Baby Shaji John, the former MD’s son and current Joint MD, as the new Managing Director. The market is likely to wait and watch his leadership direction and performance.

2 Likes

Hello,

I have been reading about the company recently, found the business that the company is doing to be interesting.

Had a few observations around the debt structure that the company is planning to take, wanted to understand more from the seniors if the observation is correct

1. Current Debt vs. Future Debt

-

Current Debt: As of February 2025, their outstanding Non-Convertible Debentures (NCDs) were relatively low at ₹16.45 crore. Compared to an annualized revenue of roughly ₹137 crore (based on Q1 FY26), their current debt-to-sales ratio is actually quite conservative.

-

The “Big” Debt: The ₹110–₹120 crore loan is specifically for the Maritech Eco Park. This is a “soft loan” through the Government’s Fisheries and Infrastructure Development Fund, which comes with a 3% interest subvention (subsidy).

2. The Calculation of Growth

The management is betting that the debt will be “serviced” by a massive jump in sales:

-

Production Leap: Marinetech is designed to produce 1,600 tons of shrimp annually.

-

Efficiency: They claim they can move from the national average of 5 tons per hectare to 50 tons per hectare using this new tech.

-

Revenue Goal: They are targeting a 60–65% CAGR. If they hit their target of increasing turnover by 400% in three years, the ₹120 crore debt becomes much smaller relative to a projected ₹500 crore+ revenue.

3. The “Safety Net” Strategies

To keep the debt from crushing the balance sheet, they’ve highlighted two major mitigations:

-

Land Monetization: They plan to unlock ₹150 crore from their land bank in Bangalore, Cochin, and Tuticorin over the next 36 months. This cash influx is essentially intended to act as a hedge against their debt obligations.

-

Asset-Light Farming: For their regular expansion, they’ve stopped buying land and started leasing farms. This costs ₹7.5 lakh per pond versus ₹40 lakh to buy, significantly reducing the need for more debt as they scale.

Disc: Not invested, tracking. Will keep evaluating the company for this quarter to track, how are the company numbers aligning with the aggressive growth commentary that the management has given.

1 Like