- The Company was established in 1981 and currently operates through two distinct business verticals, Retail and Distribution , each with its predominantly own customer base, sale channels and product range. The Company has successfully established an identity as an affordable fashion brand , catering to the entire family for all occasions. Fashion doesn’t need to be expensive.

- Khadim as a brand very well fits in the both the parts of the Country . On One side it offers premium yet affordable range of products across its retail stores in the metros (Tier 1&2) with its top retails sub-brands like British Walker, Lazard, Cleo, Pro etc. On the other side it also caters largely to the demand of Bharat (Tier III cities, semi urban and rural areas) by capitalising its distribution network and products under the sub-brand of Wash N Wear, Kalypso, Fitnxt which offers a perfect mix of fashionably durable and extremely pocket friendly footwear.

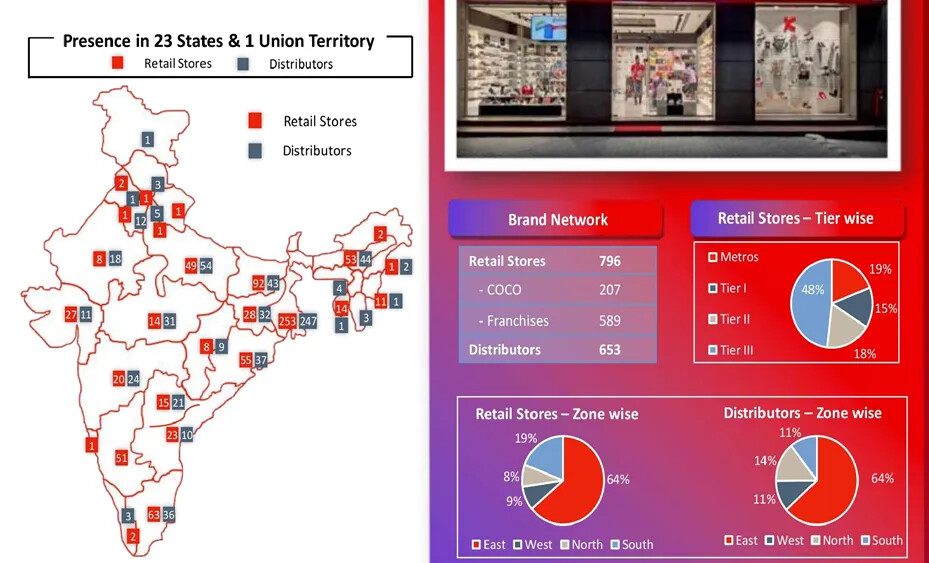

- Retail : The Company’s retail business is operated under the ‘Khadim’ brand, through 757 brand outlets (as of FY21) catering to Middle & upper middle income consumers in metros (including mini metros) as well as in Tier I, Tier II and Tier III cities. Given the aspirational nature of customer base, we have increased focus on sub-brands to drive premiumization, which will lead to higher ASP and gross margin. Keeping in mind the rising demand of casual and sports wear during this pandemic period, the Company has come up with fashionable and vibrant range of products to cater to market demand.

They are consciously making a significant effort to upscale the mother brand Khadim. We are also repositioning the following subbrands:

In Retail, the Company has been expanding its store network across India with focus on premiumization, asset light model and optimum capacity utilization.

The retail segment is what drives profitability due to high gross margin, ability to pass on price hikes. As a result of premiumization of its products through various subbrands, there has been an increase in ASP leading to higher gross margin. This segment decides overall profitability of the company. So pay special attention as you read further.

- Distribution : In the Distribution segment, Khadim has always been known for the quality and durability of the Hawaai and PVC chappals. However, in the last few years, even this business has become fashion oriented and has started demanding freshness every season. To be able to cater to the various categories of products, we have introduced subbrands in this business segment as well:

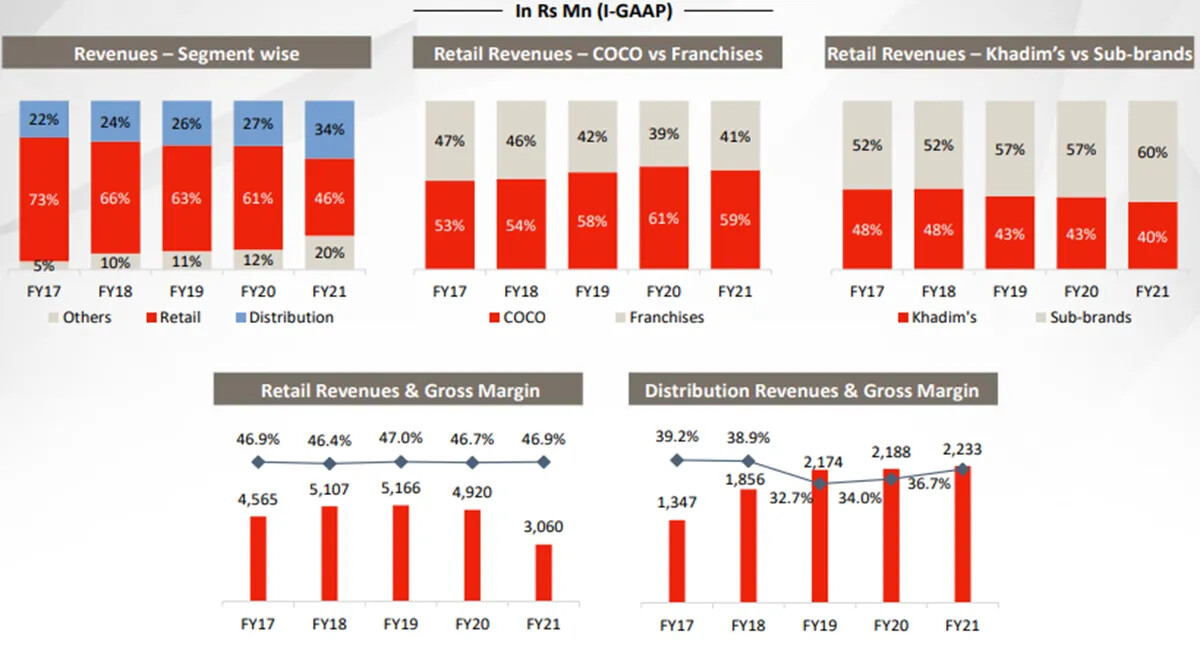

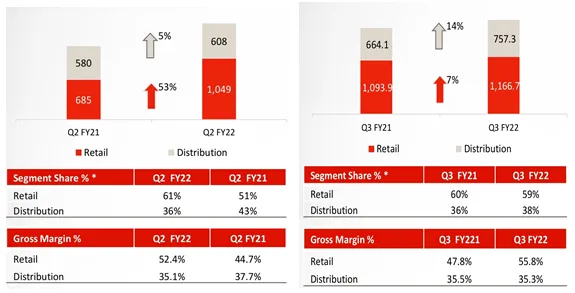

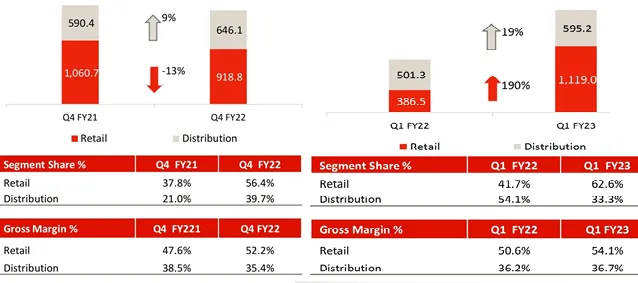

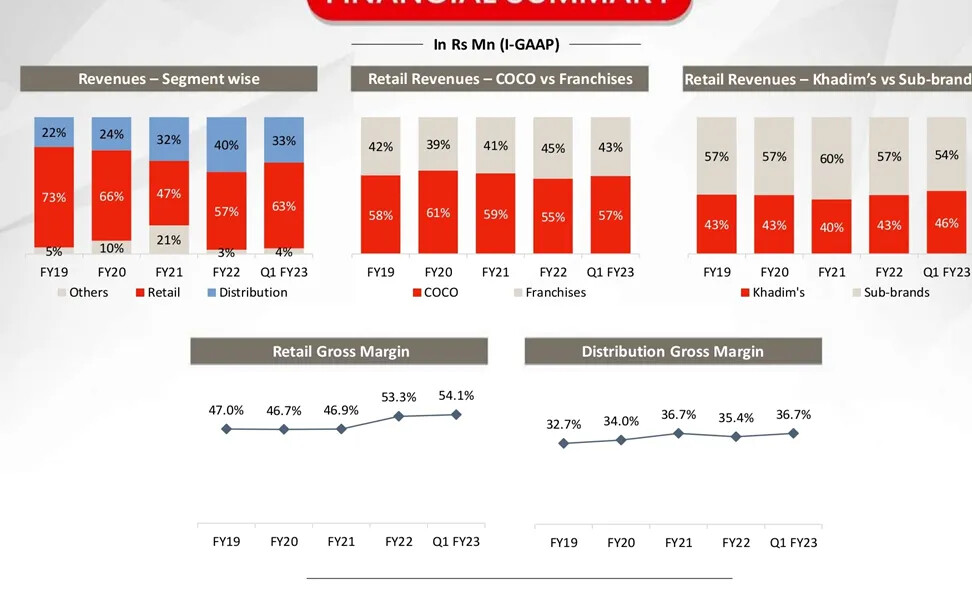

The distribution segment is a volume based business and is a highly scalable model on the front end mix of in-house and contract manufacturing. The distribution business operates through 575 distributors, selling products to various outlets across India. With affordable and competitive pricing the Company targets lower and middle-income people from Tier I to Tier III, who shop in Multi Brand Outlets (MBOs). The distribution business offers EVA, basic and premium Hawai, PVC, PVC DIP, PU and Stuck On products. - Revenue Trend of Retail and Distribution segment along with the gross margins:

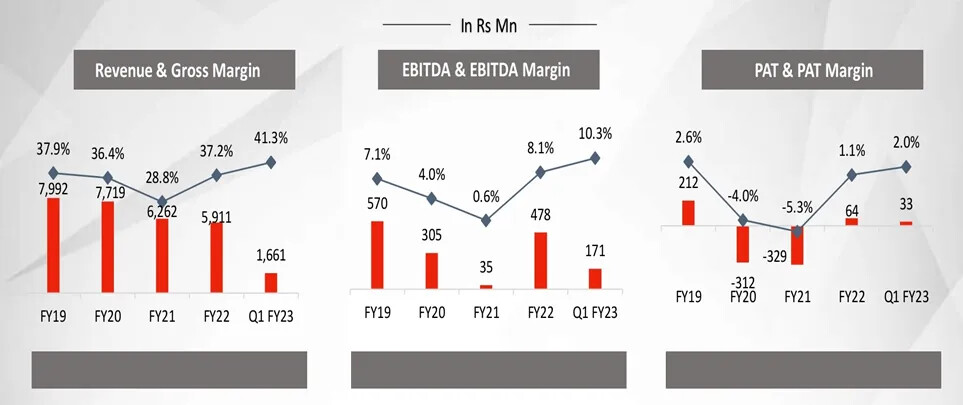

Retail sale in FY21 was 306 cr vs FY22 336 cr. - Marketing and Advertisement : In FY19 they did marketing with Bollywood stars like Kangana, Farhan Akhtar and cricketer Dinesh Kartick. Now they are doing it also with local Celebrities. I’m from West Bengal and recently I saw one youtube advertisement featuring famous youtubers Bong Guy and Wonder Munna. Doing advertisement with local celebrities cost less and serves the purpose.

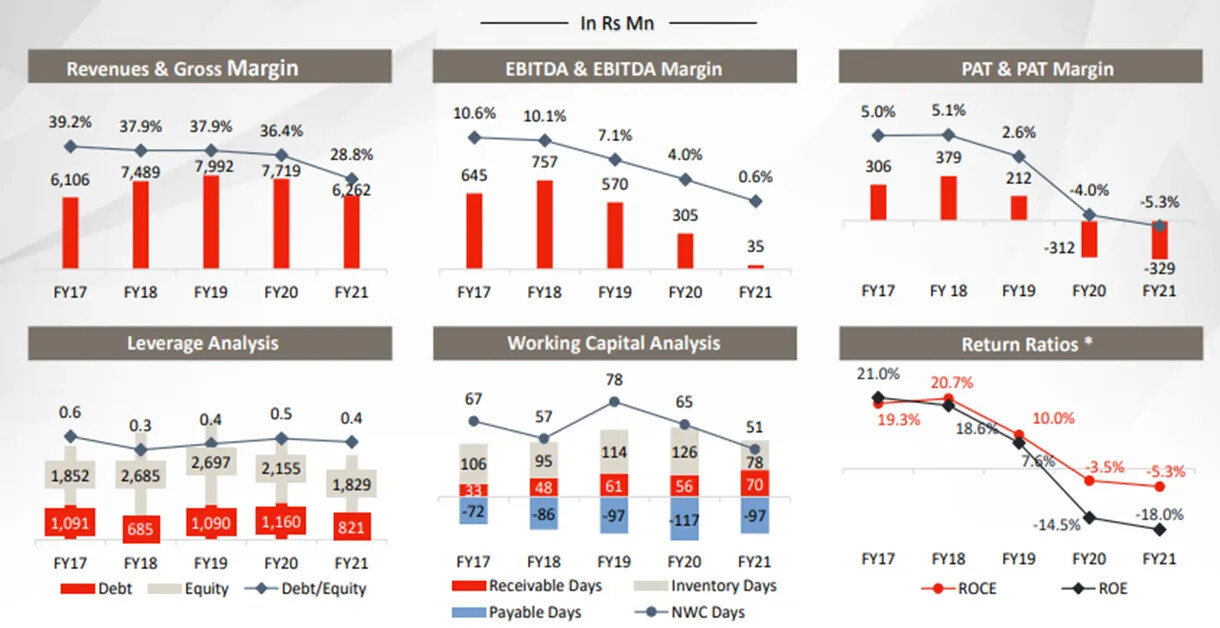

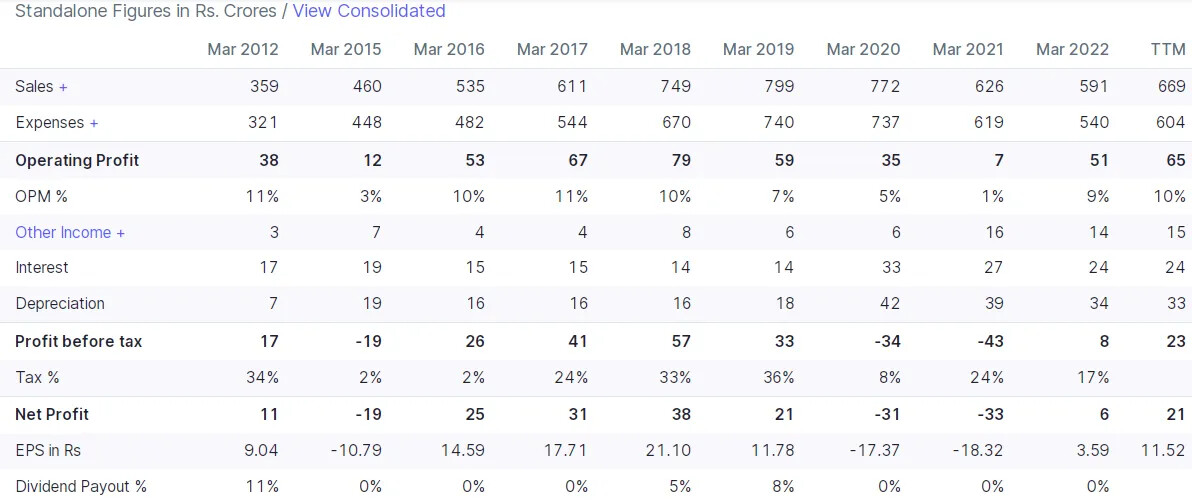

- Revenue Trend and Margin Trend

- Return Ratios

- Retail & Distribution Mix and their margins : The retail business represented 47% of the revenue share at INR 2960.5 million during the year, while the Distribution business, which represents 32% of the revenue, stood at INR 2018.2 million during FY21. The corresponding gross margins stood at 45.1% for retail and 30% for distribution business.

- Management:

11.Focus on Profitability: The focus has transitioned from only sales to profit first. Every possible lever is being worked upon to ensure it is profit accretive. Some of the initiatives taken are listed below:

· Focusing on product gross margin through premiumization and price increase

· Rationalising inventory purchases which limits liquidation costs

· Fixed cost reduction

· Asset light growth model

· Working capital efficiency

· Leaner organisation structure

· ROI focused marketing spend

· Discontinued Institutional sale having low margin: in FY19 it was 69 cr and in FY21 ot was 90 cr and 0 in FY22

· Shut underperforming stores

A data driven approach has helped us drive some of the above changes towards lower breakeven sales and increased profitability. Every decision is taken keeping in mind profit.

12. Market Outlook:

• India is witnessing a significant shift in the consumption pattern of unbranded vis a vis branded footwear, The gap between the two is getting narrower YOY with sharp inclination towards branded footwear. The current figures stand at 45% in favor of branded footwear. Also 40% of the population is expected to reside in urban areas by 2030.

• India is witnessing a significant shift in the consumption pattern of unbranded vis a vis branded footwear, The gap between the two is getting narrower YOY with sharp inclination towards branded footwear. The current figures stands at 45% in favor of branded footwear1. Also 40% of the population is expected to reside in urban areas by 2030. This places the Company at an advantageous position to penetrate into a wider market.

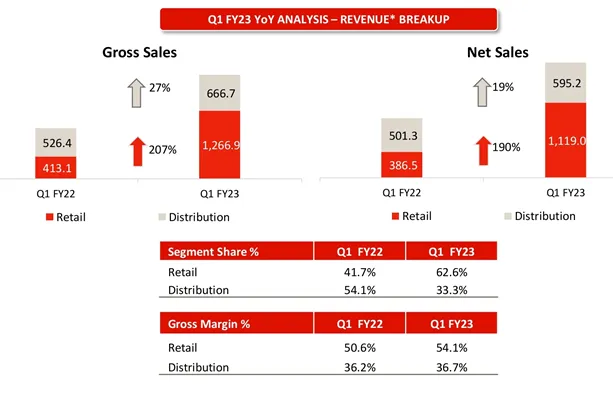

13. Retail and Distribution Sales Growth and Discontinued Institutional sale : Net sales in FY21 had been impacted on account of significant impact on the retail sector which declined y-o-y by 38% due to the pandemic, however, increase in lower margined institutional sales partly made up for the decline in sales during the year. In FY22, the net sales decreased y-o-y from Rs.623 crore to Rs.588 crore, due to company’s strategy of discontinuing lower margin institutional sales. However, the retail and distribution segment grew by around 15-16% y-o-y in FY22. It must also be noted that sales were adversely impacted in Q1FY22 due to the second wave and in Q4FY22 due to the third omicron wave and increase in GST rates. Even though increase in GST has led to some moderation in demand, adjustment of accumulated service GST is expected to ease working capital requirement going forward. On the current demand front, the retail segment has shown improvement since then and the distribution segment is still facing relatively slower demand due to inflationary pressures

14. Key raw materials are Poly Vinyl Chloride (PVC), leather, rubber, EVA, Poly Urethane (PU) and other compounds. A large part of this compounds are crude derivatives (PVC, EVA and PU) and the prices of natural rubber are also volatile depending upon demand and supply scenarios. Khadim’s manufacturing division caters to the distribution segment, where pass on in increase in prices is difficult. The distribution segment, however, has seen a hike of around 20-22% in FY22. The company majorly relies on outsourcing for its retail division (~84% of retail sales in FY22). Khadim has a large base of outsourced vendors who are having long relationship with the company. Due to better negotiating power of Khadim, it is usually able to manage short term volatility. Further, as demand elasticity is relatively lower at the consumer level the company has taken multiple price increases in the retail segment.

15. Retail & Distribution Sales trend with Gross Margins in past few quarters:

See how retail sales are increasing considering the seasonality effect. But it’s yet to be know whether there is any volume growth or the whole sales rise is result of increasing margin due to rise in average selling price.

16. Future Guidance:

Management is guiding for 800 cr gross sales for fy23 considering gst hike. If we exclude gst hike then it will be 750 cr. and ebitda margin guidance of 12%. In q1fy23 ebitda margin is 10%. with increase in sales and operating leverage the ebitda margin should increase naturally. they intended to do 1000 cr sales by fy25 and ebitda margin of 14-15%. Presently the pat looks down due to operating deleverage

So with increasing sales the ebitda margin should rise and the PAT should increase very fast. To give some perspective they did 590 cr sales in FY22 with 9% EBITDA margin of 50 cr ebitda and 8 cr pbt. with sales going to 750 cr in fy22 the ebitda at 11% will be 80 cr and pbt should be around 38 cr. Similarly do the math for mgmt guidance of 1000 cr sales at 14-15% ebitda margins. But take all the guidance with pinch of salt because in retail business you can do all the right things yet don’t get the desired result. Human nature is not like 2+2=4.

17. Findings Based on recent Scuttlebutt to franchise store in my home town:

a. Cleo and Pro are selling more. both are retail brands.

b. They are selling wallet, belt, socks, ladies bag in franchise store under the pro brand.This is new and it’s mentioned in the recently published annual report also.

c. The sales should be good due to all durga puja shopping are done in q2 because durga puja is main festival in wb and ppl do most shopping before it. then the festive season is coming followed by wedding season. Most Khadim retail stores are in West Bengal.

18. 1. Antithesis:

a. Intense competition b. They have good brand recall among our parents who are in their 50s and 60s for products being value for money. But they are now trying to capture the young generation. They have to make brand image among young generation. The results of their efforts are yet to be seen in retail sales in coming 2-3 quarters of fy23 in terms of volume growth which is a normal year. The revenue growth will happen naturally due to rise in average selling price.

c. The retail sale should increase along with volume growth (which is yet to be seen). Because till now retail sales growth seems to be result of Asp increase due to gross margin increase. The thesis fails if retail sales doesn’t grow accompanied by volume . They faced loss on pat basis in past because of declining retail sales only.

d. Debt on balance sheet. The debt is of wc capital loan type. Though the debt to equity ratio is around 0.5 (screener showing 1.17 which considers lease liability as debt). The interest cost is eating the PAT. How ever with increasing sales the PAT will increase due to operating leverage and that should reduce the wc loan going ahead.

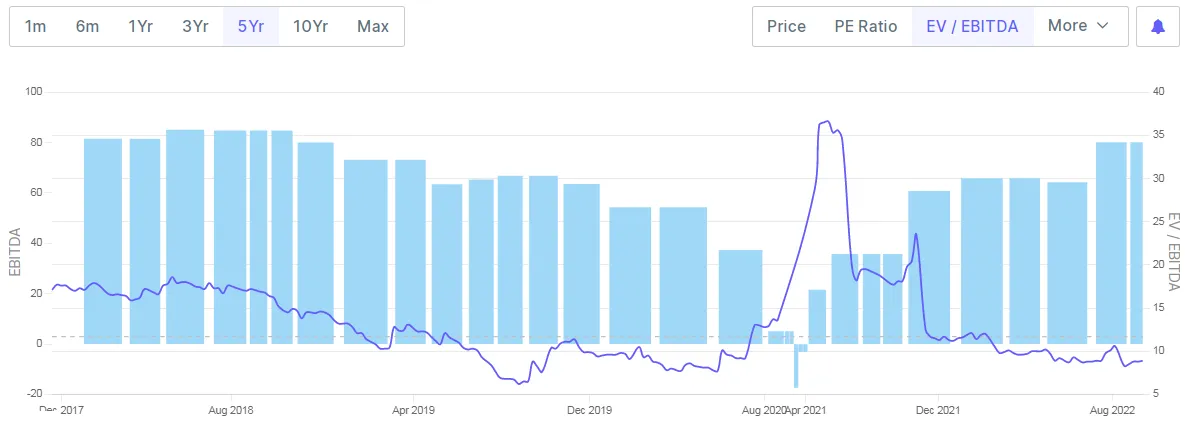

19. Valuation:

Company is a turnaround so it should be valued by ev/ebitda or mcap/sales as pe ratio will be misleading due to co going under oeprating leverage.

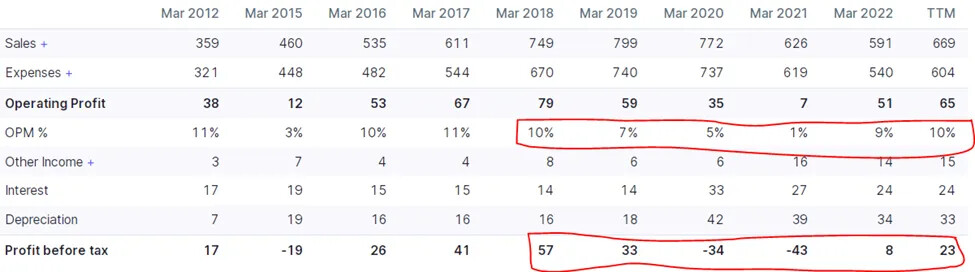

Based on ttm ev/ebitda they are trading at 9 & ttm mcap/sales of 0.7 and with increase in profit they should be re-rated. Here see the historical valuations

So if they do 1000 cr sales and even if they do 14% margin (should not be a big deal they already done 12% in q3fy22 w/o operating leverage) the ebitda should be 140 cr. 2.8x from fy22. if the valuation multiple gets restored to historical valuation during 2018 (mcap/sales of 1.8 and ev/ebitda of 17) the the price should be 2x-3x from here on conservative basis. But again the condition for this is to increase in retail sales with volume growth in coming 1-2 quarters. However the present valuation is cheap enough that even if growth in retail doesn’t happen accompanied by volume the downside is very low. So head I win, tail I don’t loose much type of situation.

Q2FY22 Updates:

-

Sales of COCO & Franchise store: No, if the product is sold at MRP, it is recorded at MRP price. If it is sold at a discount in COCO, it is recorded at a discounted price. Namrata was saying that in COCO sales recording is in MRP whereas in case of EBO we give a trade discount of around 30% to 35%. So the Company records the primary sales of 65%. So that is why the COCO numbers are higher compared to the franchises

-

Last year we had already shut down 13 COCOs which were at a negative run rate. Out of 207 COCO, only 10 stores are not in breakeven terms,otherwise all the COCO stores are breakeven

-

Last year in H2 there was an institutional sale of around 90 Crores. FY22 it’s going to be 0.

-

During COVID time, our fashion-wear contribution had gone down tremendously in retail. So, are we seeing that coming back strongly in ensuing quarters?: Yes, sure. We are already seeing it at normal level in Q2. In fact, during the festive season, we have seen normalized buying in all the categories, and we have also seen the trend currently. So we are hoping that the fashion buying continues.

-

Price Pass on: See, on the retail side, we are hoping to be able to pass on the increased raw material prices and still make an incremental margin. The pricing is relatively on the higher side compared to distribution. So, there we should be able to absorb and pass on and grow. But on the distribution side, it is a bit choppy and the raw material pricing is very sensitive to the pricing of the product because you are dealing over there in Hawaii chappal, PVC chappals, PU chappals, low priced sports shoes where the price is a very, very sensitive aspects of the product. So, we are hoping that the raw material pricing stabilizes, there can be some sanity and stability to the pricing as well. Till the raw material pricing stabilizes there will be some chopping in the gross margin. We are hoping to pass it on as much as possible. We also have to be careful with the MRP because we are dealing with the mass audience. So, there will be that much price increases that one should take, to be able to pass on to the customer, but we are trying to do our best

-

On the retail side, we will have to ensure that our existing base of store grows at a healthy pace of SSG, which is around 5% to 6% and we intend to grow the retail business overall around 10% to 12% with the balance coming from store expansion. On the distribution side, it is going to be purely an increase in the market share with the existing base of distributors and also building the base of new distributors

-

Revenue per square foot vs Revenue per store: In terms of pairs sold in quarter, in distribution it is around 67 lac pairs and in retail it is 22 lac pairs. If you compare our COCO store, average revenue is around 1.25 crores per store. Yes, compared to Bata it is less because the ASP of Bata is higher compared to us. The product mix also matters, 75% of our products are below ₹ 1000 as compared to Bata who are selling 50% of the product over ₹ 1000.I would like to add over here, this is revenue per store you are comparing. If you compare revenue per square feet and gross margins per square feet, we are as good as them and in some cases even better

-

Increasing price in retail w/o impacting demand: Just to give you a history, over the last two years we have taken regular price increases on all our existing range and new range. I have not seen any impact on demand owing to the price increases. You know, our base is generally low and secondly the product range at the prices we are selling at, we do not see too many brands do that. So we are very confident of our product offering and I do not think 3% to 5% increase in prices are going to impact the volume pressures incidentally

Q1FY23 Updates:

-

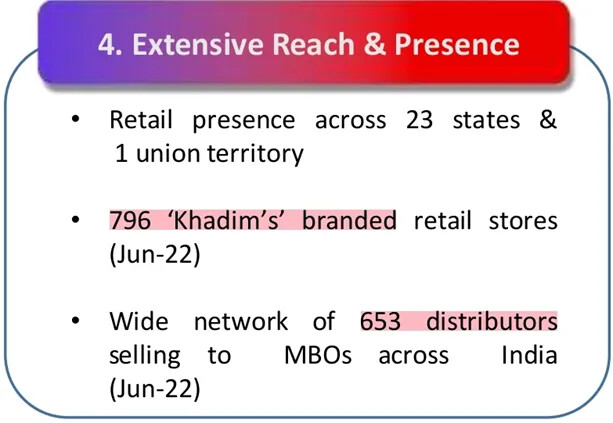

We continue to strengthen our retail presence and expanded our store network to 796 stores with an addition of 25 stores

-

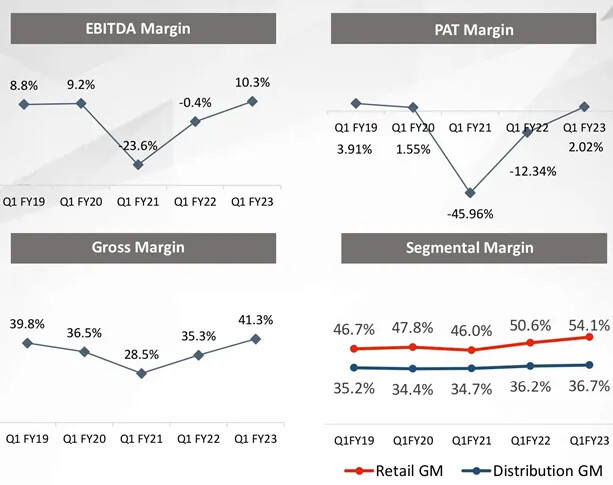

Retail gross margin increased qoq as well as yoy : it’s function of price increases to adjust for the raw material price increase and the GST. And also the premiumization which we are doing in our product mix to ensure that the sub-brands sell more, which drives the ASP increase and the gross margin increase. And mainly the gross margin increase is there in the retail segment, where from 50%, it has gone to 54%.

-

The overall gross margin increase is mainly driven through the ASP increase, which is driven through the entire premiumization and the requisite price increases to make up for the inflationary pressures and the GST increase

-

Can the retail gross margin increase further : Sir, it’s definitely possible, but to put a minimum or a maximum does become tough. We are right now at our healthiest and the highest ever gross margin. And if you compare to the industry standard, I think we are pretty much there. In fact, if you compare any apparel or a footwear retail company, our gross margins are pretty comparable. So I think we’ve reached healthy numbers. The idea from now on is to ensure that we are working on the range architecture to ensure the ASP increase, which will be driven through the premiumization which we are trying to do through our range architecture and also which will drive the gross margin increase. But we also want to ensure that we are continuing to keep the products affordable. Our positioning is affordable fashion. We don’t intend to become premium, so to ensure that we continue to remain affordable, this is a very healthy margin given that position that we’re looking at.

-

How the EBITDA margins will improve going ahead : So it’s going to be a function of the fact that the growth will come back, will normalize much more. If you’re seeing that in the last quarter, also inflation and COVID was a reality. But I think we are looking at growing in terms of sales, our retail expansion. The operating leverage coming in will definitely improve the EBITDA margins. That, there is no two ways about it. On the distribution side, as you said, see, distribution is the very different business compared to the retail business. Distribution, the product mix is very different. There is Hawai chappal, PVC chappal PU chappal and 80% of your product mix or the product range is below ₹ 500. So there, the ASP increase is not something which we are significantly looking at as much as we’re looking at the volume growth because there the business is grown in terms of volume, we will take more market share. And the operating leverage itself will drive you the profitability improvement. So I’m hoping, over the next couple of years, we’ll be looking at the number you’re talking about.

-

Increasing Same Store Sale : we are constantly trying to figure on a regular basis, analyzing the stores which are performing lower than the average or a healthy EBITDA margin to ensure that we are working on the range architecture and we’re working on the cost lever either to increase sales or to reduce cost to ensure that store continues to remain healthy, profitable. So that’s an ongoing exercise by the entire team

-

I think one would appreciate that in the last 5 to 6 quarters, we have continuously given profitability and managed to turn around despite COVID. And I think at 10.5%, we are doing good numbers. In fact, some of the companies in the industry are at similar levels as well. So I think, yes, there is definitely an endeavor to perform significantly better, and we are definitely looking at doing it. But I think it’s the process of time. I think second and third quarter, given that will be significantly better, hopefully, given the festive is around the corner, margins should be better.

-

How is q2fy23 so far : So, I think the consumer sentiment is definitely improving. We are seeing a slow improvement in the consumer behavior. Yes, inflation is a reality. None of us can shy away from it, but consumer behavior is normalizing compared to the COVID period. We are seeing people purchasing the products across various categories, including work, festive, party, casual, sports shoes. I think so the offtake is good across every category, not only in retail, even distribution. So yes, we are hopeful that this quarter will be good

-

Short term outlook : So on the retail side, I think we are seeing an improvement coming into the numbers. As of now, up to 15th August, discount sales will be on across the entire industry, retail industry. The numbers have been healthy. And in terms of the festive, I think at least what we are hearing the festive will be good. But having said that, the Eastern side, especially Bihar and Bengal, they have been impacted by relatively lesser amount of rain this year. So the agricultural impact of it will have to be seen, but we are hopeful for a good festive season. And I think that’s the feedback that we’re getting from the ground level market.

-

Our stock base was at 98 days in 31st March 2022. So it has gone up slightly higher to 104 days. Second quarter also, the stock level will be high. But once the festive has gone, the stock level days will come down

-

What categories doing well : In terms of category, as I said earlier, during the COVID period, there were some categories which were performing decently well and some categories were underperforming significantly, like there was no demand for workwear, there was no demand for school shoes, there was no demand for party wear. So there was more basic demand requirement. Home wear or sport shoes, athleisure was very huge during COVID period, which continues to be significant. But now there is a demand of work wear. School shoes have come back pretty significantly. But if you see on a normalized basis, there’ll be spurts of demand because of the pent-up demand which has come owing to limited shopping in the last couple of years. But then on a normalized basis, we are seeing all categories perform the way they were doing pre COVID.

-

ASP : So I think in terms of growth, at pre-COVID levels, we were approximately at ₹ 500 as an ASP at our retail level. We have gone up to approximately ₹ 600 in terms of average selling price, which is a good increase in the ASP, which is driven through the entire premiumization that we’re looking at, the price increase that we have also taken adjusting for the raw material and the GST. So the improvement has also been reflected in the gross margins as well. So that is definitely something which has been a significant reason for even the recovery for our business.

-

So in retail, our ASP is approximately 600. And in distribution, it is approximately 100

-

Growth : I think the ASP increase that we will be looking at in the range of around 4% to 5% and the balance coming through the SSG and the new store openings on an annual basis. We’re looking at growing approximately 70 to 80 stores on a year-on-year basis across the markets that we are currently present and in new markets through COCO and franchisees, but largely driven through the franchisee model

-

Growth Guidance: 800 cr revenue at 12% EBITDA margin for FY23. This 800 cr is including GST.

-

So just to give you a perspective, if you look at even in our investor report, just to give an understanding as to the pre and the post impact of GST. If you remove the impact of the GST, the growth for the distribution business was almost 27% and retail was almost 207%. Vis-a-vis the net sales is 19% and 190%

-

Headwinds : There have been a couple of abnormal years and the reasons also is that the inflation were there, the GST was there. And given that the GST increase was almost from 5% to 12%, which is in the below ₹ 1,000 category wherein almost 80% of our retail product range is there and almost 100% of our distribution product range. So the GST impact was quite significant

-

So this quarter was very difficult for footwear industry, especially for value retailers like us because there was a GST increase also, which we had to pass on along with inflation. And still, we actually did well. Even demand also did not get impacted much. So just wanted to understand, how should we read consumer sentiment? Because the pure price increase and GST increase and the kind of cohort that we are servicing to, I’m assuming that it has to be price sensitive, but what worked for us? : in general, the kind of product mix and the price assortment that we have, and I’ve said this in many calls and conversations which I’ve had with the larger investor base, is that on the retail side, I don’t think there’s any other brand that is able to offer the kind of product mix at the price point that we are offering. It is with utmost modesty that I’m stating that because we’ve done the recce across most brands. The range that we’re offering at the price point that we’re offering, there are not many brands who are able to do that. And that’s also the DNA of the organization, which has been built up over many, many years. So because of this, the impact on the retail side has been relatively lesser in terms of the impact of inflation. I’m not saying it’s not there, but it’s relatively lesser because our strength is our affordability and fashion. On the distribution side, yes, there has been an impact in terms of volume and price point purely because the consumer today, he has to juggle with, for lack of better words, atta, sugar, tea at much higher prices than they were being used to. So then they today have, if they’re earning ₹ 100, their income has not increased significantly as much the cost has increased. So today, they have to make a choice of whether they want to go for a branded player or a non-branded player because even if they want to go for branded player, does their pockets allow it. Maybe it’s a short-term issue, but it is definitely a concern for most of the brands in the country.

-

FY25 Guidance : So I mean if you take approximately a 15% compounded growth rate, it’ll come up about ₹ 1,050 crore. So if you can possibly think that as a number. But I mean the idea is to reach to cross the ₹ 1,000 crore mark by FY’25 and achieve 14%-15% EBITDA margin.

-

Last 5 years contribution of retail sales has reduced. However since FY21 it has increased. So can we touch 500 cr retail revenue like precovid? : Yes. We are expecting that level of sales this year. And if you see the contribution, the retail this first quarter is around 63% of the total sales and distribution is at 33%. And online is 4%

-

Marketing : Doing more digital add campaign than offline. Doing with local celebrities targetting specific ge groups and gender. I saw adds in youtube of Bong Guy & Wonder Munna doing Khadims add. Not doing national level add campaign.

Disclosure: Invested.