Yes both Hbl n kernex cannt fulfil it. So in that case extension should be the only scenario. Atleast they have approval, so no point cancelling unfulfilled part and retender. Hbl n kernex will have major pie till new approvals

While your comment makes sense, but unfortunately govt babus tend to treat the text of the contracts as if its carved in stone. While a proactive officer can move the wheels of govt machinery to get the contract modified, the process is long and one can easily be accused of trying to favour certain companies. This is not worth the effort for many govt officers and so I think the extension may not be given.

I am copy pasting an image, which was originally posted here - HBL Power: Signs of change - #186 by faltooinvestor

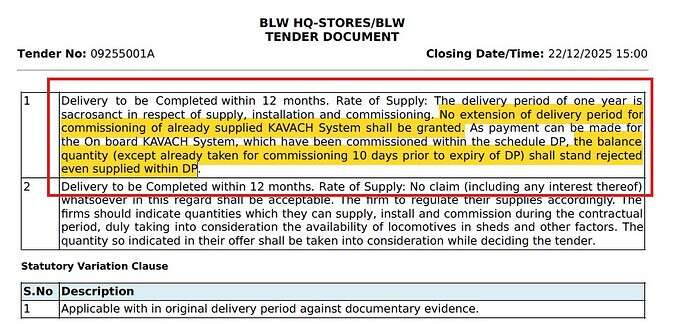

The CLW tender had similar clause on the end date.

6 Likes

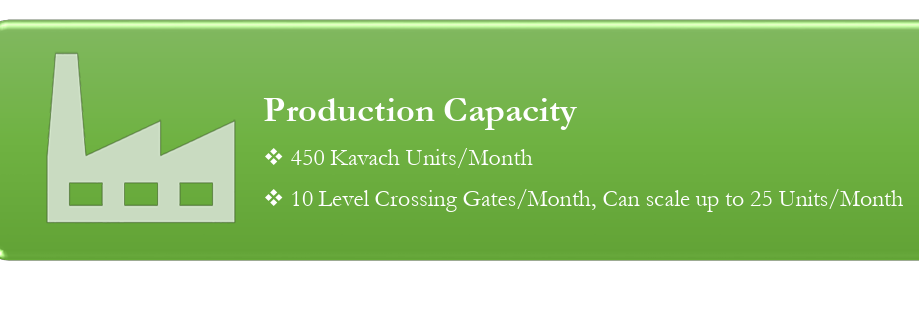

Kernex in their PPT has mentioned the peak capacity at 450 Kavach units/ month:

So even if partial order gets cancelled, they can do around 350 cr sales (450 * 0.80) at peak capacity in Q3 this year, asumming they got roughly one month of time after approval. Conservatively, we can assume they will do around 250-300 cr sales from Loco Kavach alone.

Also it is safe to assume that trackside execution should be negligible in Q3 as the main focus is on Loco orders, as HBL had also mentioned in the AGM.

Overall, ~275 cr sales in Q3 could be a fair guess in my opinion, which is not bad and infact, would be their best ever quarter.

The question is.. what next?

My understanding is that by the end of Q3, the new tenders (CLW, ICF) should get finalized, followed by fresh orders for the OEMs. It remains to be seen, what slice of the cake will Kernex get?

Till then, happy volatility. :)

6 Likes

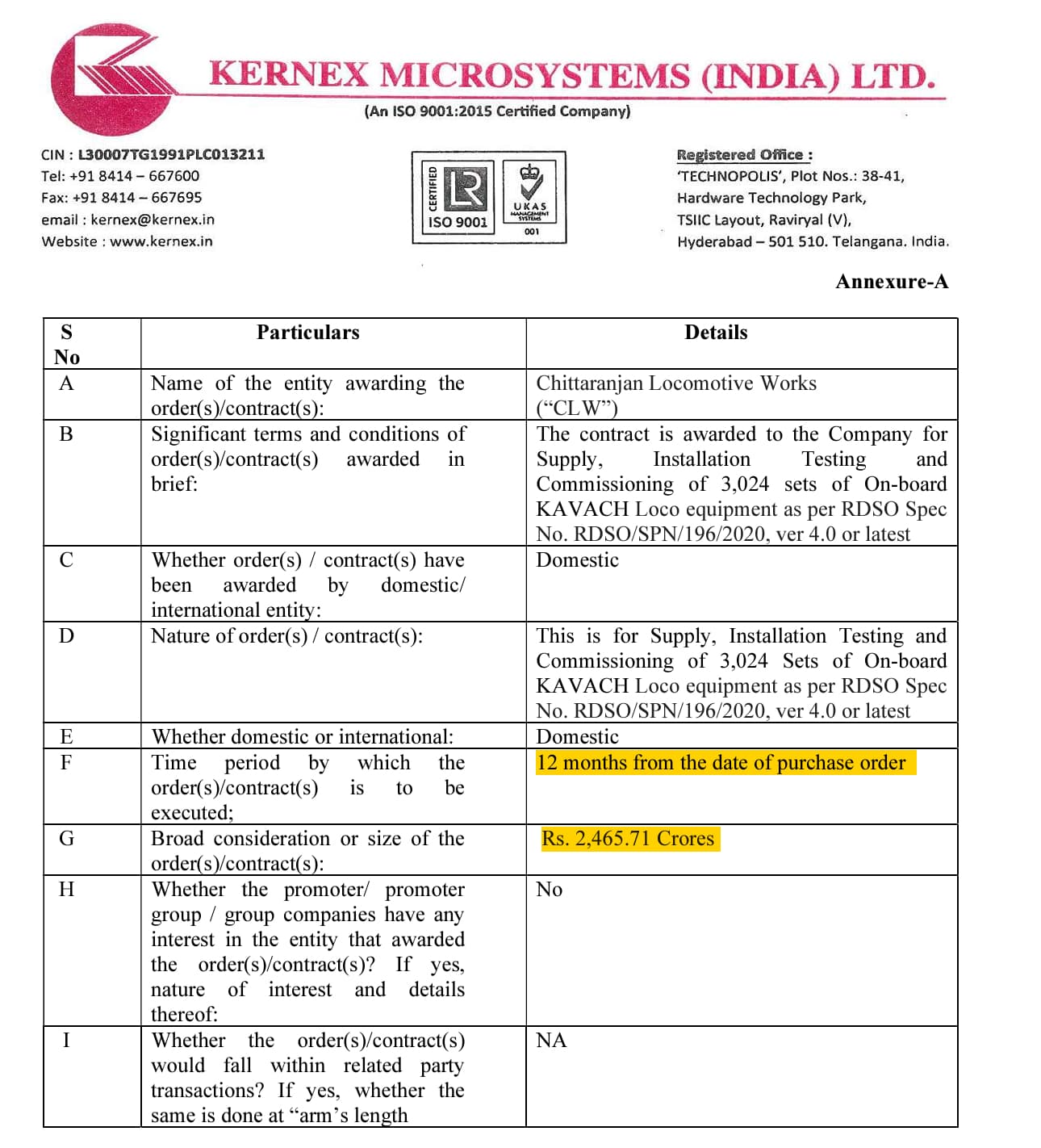

The CLW order is not just for supply of KAVACH units but also for installation and commissioning.

There are the following steps involved in installation and commissioning:

- CLW first has to make the loco unit available at the designated railway shed for installation

- Some metal cutting and welding work has to be undertaken for installation of onboard KAVACH equipment (RFID scanner underneath the loco, brake control unit, communication equipment, driver interface etc).

- Post installation the locomotive will undergo certain tests on the trial track inside the shed. This will require a loco pilot to be present.

- Commissioning: I have no idea what steps are involved in commissioning. I am guessing that the Railways have come up with some Acceptance Testing Procedure (ATP) to certify whether the installed equipment is functioning as expected. But one can imagine that officers will be required for inspection and their sign-off will be required.

So the revenue from this order does not depend only the manufacturing capacity of the company but also on the timely allocation of locomotives, shed space and manpower (loco pilot, inspection officers) by Railways.

6 Likes

What are your views on Quadrant Future Tek?

Thanks for the clarification.

I was aware of the installation and commissioning part, but I wasn’t sure how the revenue recognition is handled.

My assumption was that revenue is recognized once the equipment is supplied to the customer (i.e., once invoicing is done).

3 Likes

if CWL order get cancelled then Kernex would do less than 50 cr in 3rd qtr as per one person who talked to CS recently. So more clarity would come by current month end.

If we take relative growth in share price from current price, which do you think will do better Mighty HBL or low base Kernex ?

1 Like

Yes very well put. Kernex CS clarified that due to no shed availability not much revenue so far. So if CWL order get cancelled kernex would do very less in 3rd qtr.

HBL is certainly better in terms of execition but which company do you feel can grow better relatively from current base ? I feel Kernex has more scope to grow in terms of price rise in 1 year time frame.

1 Like

Thank you. Yes agree to that. More than efficiency India babu work culture in Govt departments is deep rooted.

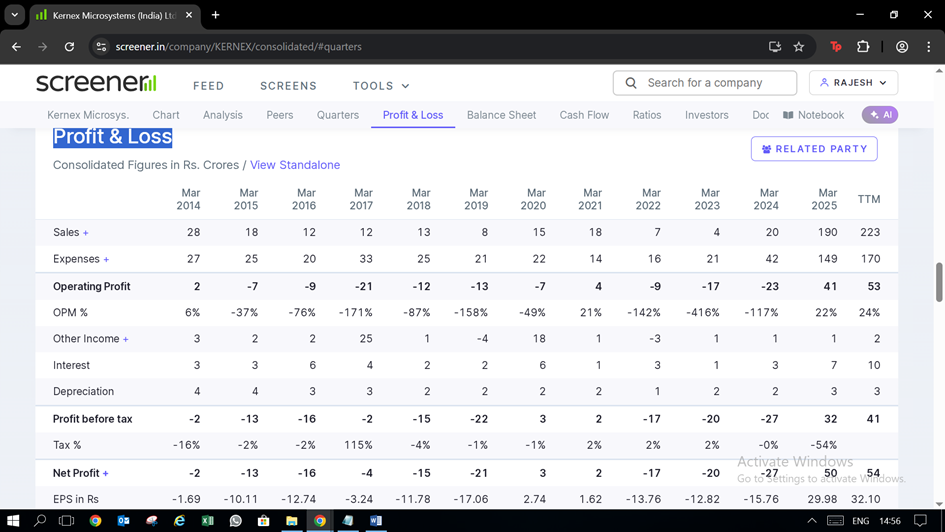

I have not studied Kernex and I hold HBL. Apologies if this is already answered in the thread. Why was Kernex struggling till 2023? Is kavach the only reason for the operational turnaround? If yes, what will happen after kavach?

Kavach is just starting, it is a 3-4 year theme minimum for Kernex. After that since Kernex is R&D and EMS company they would use their resource for defence and other related projects as pointed out in AGM. In these 3-4 years kernex will work for future as well. What is important is technical skillset and execution capabilities. Skillset we have seen as its only among 3 OEM to have kavach 4.0 license and execution needs to be seen in coming year.

2 Likes

Some people are raising concern about Problem with locoshades and allotting trains for fitment to Kernex. Any particular reason ?

Why HBL posted such spectacular execution and Kernex fails to get locoshades for fitment ? Why is it so ?

Somebody having deep understanding of how this execution work could throw some light.

3 Likes

Big update on Kernex:

₹2,400 crore order for Loco Kavach units from CLW.

Honestly, this is much bigger than I expected.

Execution timeline 1 year.

2 Likes

Does it mean less share for other players like HBL?

Good detailed post.

I differ on one key assumption — that the current orders are a combination of the earlier ~7,000 unexecuted units plus the new CLW tender.

In my view, the recent orders awarded to Quadrant & Kernex are entirely from the new CLW tender for ~7,000 units, not from a merged pool.

The reason is procedural. Retendering unexecuted quantities takes time. The delivery period for the earlier tender ended in the second week of December 2025, and even after that, some buffer may typically be allowed for final installation and commissioning. Railways generally cannot lift unexecuted quantities from a closed tender and directly merge them into an already-floated one. If that were possible, granting an extension of the delivery timeline would have been an equivalent and simpler step.

That said, even within the new ~₹5,600 crore CLW tender, the allocation to Kernex is meaningfully large.

Until we see the corresponding numbers from HBL, it’s difficult to form a complete picture of market share and execution distribution across companies.

6 Likes

I am deleting my previous post because after the update from HBL its clear that Kernex got the order for 3024 locomotives out of 6300 being the L1. (20% for developmental vendors and rest 60:40 ratio allotment for L1 and L2. Looks like Medha must be the L2 vendor and they must have matched the price of L1. The updated information is:-

Kavach update:

2024 CLW loco order - 10,000 worth 8000 crores.

2025 CLW loco order - 7000 worth 5600 crores.

2025 BLW order - 2679 worth 2100 crores

2025 ICF order - 2400 worth 1900 crores

Regarding 2024 CLW order for 10,000 locos, many remained unexecuted because of delay in RDSO approvals for Kavach version 4.0. The total executed number from last year order is different from different sources but it generally ranges from 3000-5000. As per HBL management, they have executed 1659 and the total execution is about 3000. Some other sources quote the executed number to be around 4154.

As of now the order for 6300 loco is out. Out of which Kernex got 3024 and Quadrant 353.

More than 12000 loco orders still left to be finalised and Kernex may not bid that aggressively going forward because of capacity constraints and the orders have to be fulfilled within 12 months else it will be cancelled just like the last year.

However, since all the current tenders were announced almost at the sane time, so there is a high probability that they already might have bid for the remaining BLW as well as the ICF tenders (totalling 5079 locos). So, probably they will get more orders because all vendors might have put the same pricing for all tenders.

Significant delay in the finalisation of tender for the unexecuted tender from the last year (6000-7000) will give them extra fulfilment timelines which may encourage them to bid aggressively again for the unexecuted order from the last year.

Somehow, it looks like Kernex is now in the best position to benifit from the loco part of kavach story as of now.

Disclosure: invested in Kernex as well as HBL with significant allocation.

Regards.

10 Likes

The million-dollar question:

Can Kernex execute this time?

Let’s do the math, backed by logical assumptions:

Kernex got an order for 3,024 Loco Kavach units. Their production capacity is 450 units per month.

**So at peak capacity, they can produce **

450 × 12 = 5,400 units per year.

If we also consider some backlog inventory from last year’s partial execution, annual capacity (for the current year) can touch ~6,000 units. Which is well below the order size they’ve just received.

But here’s the catch:

Kavach execution is not just about the supplier’s production capacity.

The real bottleneck is installation + commissioning at loco sheds. Availability of loco sheds is itself a constraint, because there are many locomotives and limited sheds.

But here’s another catch:

Last year, when installations began, not a single locomotive was equipped with Kavach 4.0.

So contention for limited loco sheds was very high, given the large number of “unequipped” locos.

Now the picture is different.

With a portion of the loco fleet already equipped with Kavach, contention for loco sheds should reduce going forward, thereby reducing execution delays. Add to this.. no approval-led delay this time.

Coming back to the main question – can Kernex execute?

Theoretically, a big yes!

Now for practical reasons, let’s assume they manage to supply & install only 50% of peak capacity per month, i.e.

450 / 2 = 225 units per month.

That still means:

225 × 12 = 2,700 units in one year, quite comfortably.

Verdict:

Yes, Kernex can execute this time – a good chunk of the order, if not the entire order.

Caution:

These are just guesstimates. Nothing can be guaranteed in foresight.

Disclosure: Holding both Kernex (added recently) and HBL (since 2022).

6 Likes

Challenge here is not Kavach systems form Kernex or Loco availability from Railways . It is Brake Interface Units .

Let me explain BIU first

The Brake Interface Unit (BIU) produced by Faiveley Transport (now a Wabtec Company) is a critical safety system in Indian Railways, designed to interface with the locomotive’s existing brake system (such as IRAB or E-70) to implement braking commands from the KAVACH (Train Collision Avoidance System) or Distributed Power Control System (DPCS/DPWCS).

It’s key functions are

- Safety Integration: The BIU receives signals from the KAVACH/DPCS system and translates them into pneumatic actions, such as applying brakes during red signal violations (SPAD) or potential collisions.

- Compatible Systems: The BIU is designed to work with various brake systems, including the IRAB class of brakes used in Diesel and Electric locomotives and the E-70 brake system.

- Operational Modes: The unit handles different braking levels: Normal Brake (BP 4.4 kg/cm²), Full Service Brake (BP 3.6 kg/cm²), and Emergency Brake (BP 0 kg/cm²).

- Fail-Safe Design: If the KAVACH system fails or is isolated, the BIU ensures that the normal brake functionality of the locomotive remains unaffected.

- Component Structure: The unit typically consists of an electronic module with control cards and a pneumatic panel with valves, pressure transducers, and manual cocks.

Challenge is that all the Kavach Players get BIU supply from Faiveley Transport

Basis past orders Kernex may have a inventory of 450-500 odd units in inventory and may be able to order and procure more basis current orders .

Execution may not be a challenge as most of the workers required ( Normally a team of 5-6 workers for one location ) are contractual and can be ramped up very fast basis no of BIU units available .

They have been awarded LOA ( Letter of acceptance ) as of now . They are required to deposit SD ( security deposit ) now , post which a PO ( Purchase order ) will be issues . This may take anywhere around a month post which they will start actual installation .

I feel they will get around 10 months of clear runway and if they are able to streamline all the suppies and installations , they should at best install approx 1500 units in next 1 year . With approx 80 lac a unit this should be a topline of approx 1200 cr . With 20-22% Op margin this should give us 240-250 cr op profit and almost similar PAT . Assuming no more diluation this should be approx EPS of Rs 110- 130 .

With above extremely consevative calculations also looks to be available at a decent valation multiple today

Don’t have too many insights plans of company post Kavach , after 2-3 years runway , so difficult to ascribe any terminal value .

Looks like good trading play for few quarters .

12 Likes

I’d like to add a clarification here, as some of the information above appears dated.

As of today, the Brake Interface Unit (BIU) for Kavach is not manufactured only by Faiveley. HBL and Medha also manufacture BIUs. Even Concord Control Systems have the capability to manufacture BIUs and they’ve mentioned the same several times in their concalls.

In fact, since 2022, both HBL and Medha have been approved by RDSO as Developmental Vendors for BIU.

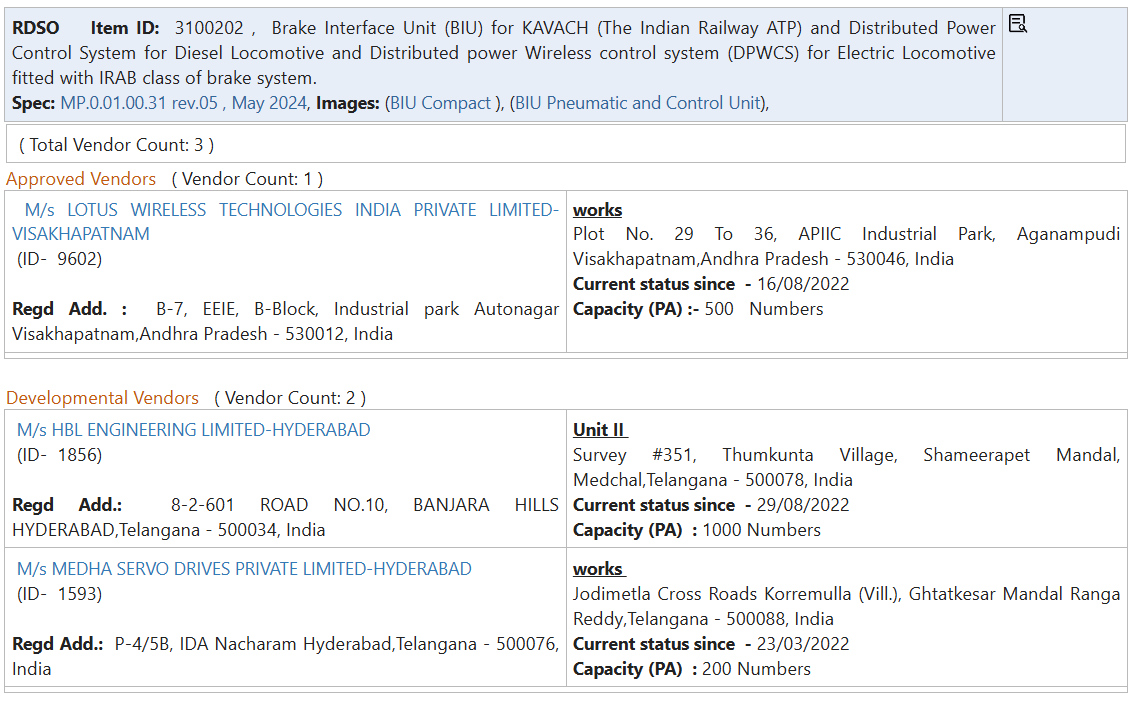

BIU approved sources information is publicly available on IREPS website:

Capacity constraints do exist, but the capability is there.

HBL, in particular, has reasonable in-house BIU capability and capacity, which allows it to internalise this critical subsystem of the Kavach stack. This also explains (partly though) why HBL’s electronic segment margins tend to be structurally higher compared to players like Kernex.

So while BIU availability has been a bottleneck at times, the supplier landscape today is broader and more diversified than it was a few years ago.

14 Likes

Great finding! So whom does Kernex purchase the BIUs from? I am guessing that pricing from any Indian vendor would be cheaper than Faiveley, which seems to be a foreign vendor with a manufacturing facility in India.

Would you have any idea, in terms of costing, what is the contribution of each system loco KAVACH set? :

- Communition antennae on the roof

- Control unit

- Driver interface

- BIU

- RFID card readers

There is another bottleneck: pre-dispatch inspection at vendor premises. For the previous tender RDSO appointed an engineer for each vendor to do this. There is a checklist and each unit is inspected/tested as per this checklist before dispatch to the shed. The engineer, apparently, would only inspect 7-8 sets per day. If RDSO appoints multiple engineers then that should speed up the process.

The good thing about the CLW tender is that installation has to happen at 46 different locations. So shed availability may not be such a big constraint as loco availability. But the fact that HBL was able to do 1600 odd installations in 6 odd months, for the first large tender (where everybody from RDSO, vendor to shed personnel were new to this) indicates that even loco availability may not be such a big issue.

2 Likes