Hi guys, I recently analyzed a very interesting company , Keltech Energies

Into manufacturing of explosives and perlites

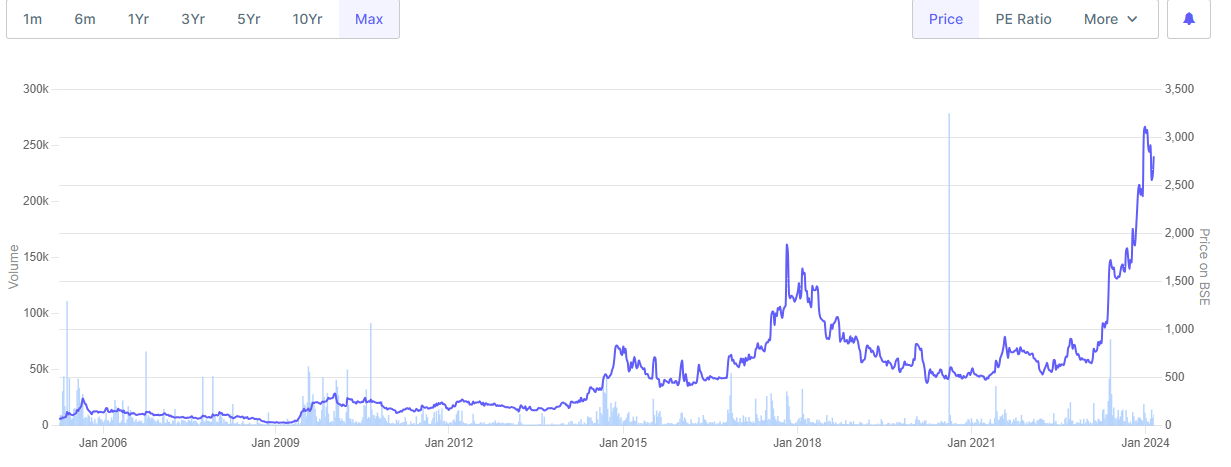

Cmp : 2803

market cap : 280 cr

This yearly profit could be around 20 cr and trading at a pe of just 14 where peers are quoting above 50

company is having recurring contracts with psus , also doubled down on revenues in last two years. Now even its peer solar indusries also having a degrowth and still quoting pe of above 60.

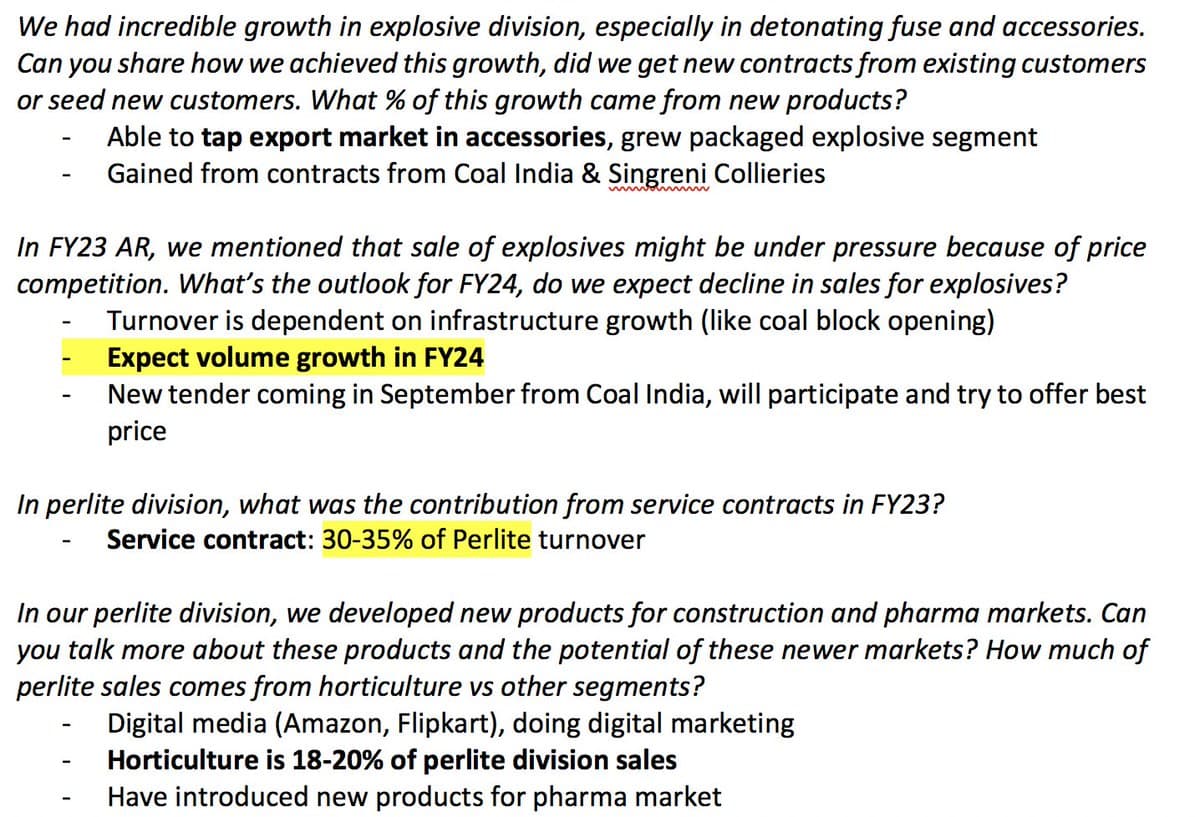

This year keltech has expanded pat margin. Seems very reasonably priced at current price.Keltech energies is participating in auctions with coal india. Even though it will have good competition, its worth to track this.

Any idea why is it still trading at such low pe ? we need to track this.

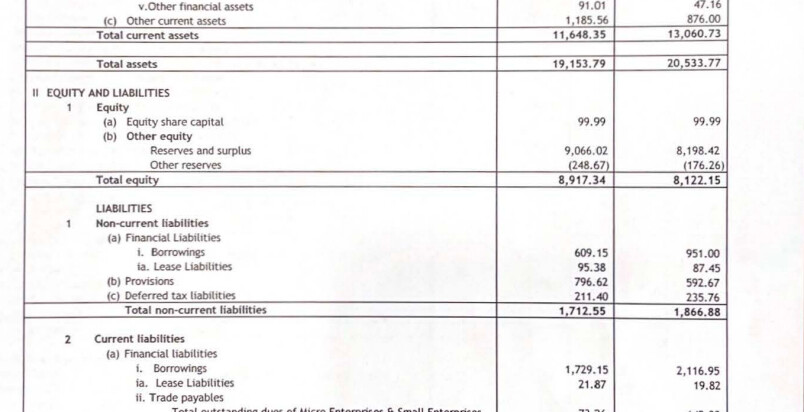

Also in the half yearly we can see this redicing debt and increasing reserves