There is a trend in the financials of this company. Every Q1 has lower numbers as compared to PY Q4 . It may be because of execution difficulties or slower development of projects in monsoon. It then recovers from gradually from Q2 .

To me numbers looks fantastic, Consistent improvement in EBITDA margins from 11.20% to 11.28% vs 10.48% last year. There is an improvement in PAT margins as well.

Q1 is generally slow compared to Q4, this time, one differentiating factor could be Elections. Exports generally picks up in Q3.

Company is now zero net debt.

Really impressive set of numbers.

3 Likes

KEI Industries Q1 FY25 Analysis: Key takeaways!!

KEI Industries continues to demonstrate robust growth, with Q1 FY25 net sales increasing by 15.72% year-over-year to INR 2,060.50 crores. The company’s EBITDA grew by 24.55% to INR 232.41 crores, while profit after tax increased by 23.77% to INR 150.25 crores. The management expects to maintain a CAGR of 15-16% in the coming years, indicating a positive business outlook.

Strategic Initiatives:

- Capacity Expansion: KEI is undertaking significant capacity expansions, including:

- Brownfield expansion at Chinchpada for wires and house wires

- Greenfield/Brownfield expansion at Pathredi for LT power cables

- Major Greenfield expansion in Sanand, Gujarat for LT, HT, and EHV cables

-

Export Focus: The company is actively working to increase its footprint in international markets, particularly in the U.S. and Europe.

-

Product Mix Optimization: KEI is focusing on high-margin products like extra high voltage (EHV) cables and expanding its presence in sectors such as solar, wind, and oil & gas.

Trends and Themes:

- Increasing B2C Sales: The company’s distribution network sales (B2C) grew by 29% YoY, contributing 53% of total sales in Q1 FY25.

- Growth in Real Estate Sector: Strong demand for wires and flexibles from the real estate and rental markets.

- Shift towards Renewable Energy: Increasing demand for cables in solar and wind power projects.

Industry Tailwinds:

- Government infrastructure push

- Growing renewable energy sector

- Increasing industrial capex

- Revival in real estate sector

Industry Headwinds:

- Fluctuations in copper prices affecting short-term demand

- Logistical challenges in exports

Analyst Concerns and Management Response:

- Export Decline: Management clarified that the 24% decline in exports was due to logistics issues and expects to make up the shortfall in Q2.

- Margin Expansion: The company expects margins to improve by 1% in the next 3-4 years due to economies of scale from capacity expansions.

Competitive Landscape:

KEI Industries maintains a strong position in the cable and wire industry with an estimated 12% market share. The company’s focus on direct exports differentiates it from competitors who are shifting towards distributor-based models.

Guidance and Outlook:

- Revenue growth guidance of 16-17% for FY25

- EBITDA margin guidance of around 11% for FY25, with potential expansion to 12% by FY27

- Expectation of INR 200-300 crores revenue from the U.S. market in FY25

Capital Allocation Strategy:

- Total planned capex of INR 1,400-1,600 crores over FY25 and FY26 for the Sanand project

- Financing mix of INR 300-500 crores in term loans and the rest from internal accruals

Opportunities & Risks:

Opportunities:

- Expansion into new export markets

- Growing demand from renewable energy sector

- Potential for margin expansion with scale

Risks:

- Fluctuations in raw material prices

- Dependency on government infrastructure spending

- Intense competition in the wire and cable industry

Customer Sentiment:

Strong customer sentiment in both B2B and B2C segments, driven by infrastructure development, real estate growth, and industrial capex.

Top 3 Takeaways:

- Robust growth across segments with a focus on high-margin products and B2C sales

- Significant capacity expansion plans to support future growth

- Strong export potential, particularly in the U.S. market, with expectations of substantial growth in FY25

3 Likes

The company as committed has completed its brownfield expansion by incurring ₹125 crore funded through internal accruals at its Pathredi plant, which will enable it to generate additional ₹800-900 crore of annual revenue.

This Plant expansion will increase the capacity of LT power cables, and hopefully will enable KEI to grow by 16% to 17% in this financial year itself.

4 Likes

Key takeaways from KEI Q2 con call

-

Drop in Margins is mainly due to increase in raw material prices of Copper, Management is extremely confident in maintaining their guidance of 10.5% to 11.0% for FY 25. For H1 FY 25 it is 10.88%

-

Revenue growth is in line with guided growth of 17% (guidance 15%-17% long term)

-

EPC business will continue to stay at 5%-6% of total revenue, drop this quarter will be compensated in the next couple of quarters.

-

QIP is done with a

- broader vision of staying a debt free company in the long run. Management does not believe in spending cash on interest costs.

- purpose to utilize the QIP proceeds for Sanad plant, which has a total capital outlay of 1800-2000 Cr, and a revenue capacity of Rs. 5,000 Crs.

- purpose to restrict the credit line / borrowing facility only to meet working capital requirements

-

Management is confident of not going for further fund raise either through debt or QIP for next 5-7 years post this fund raise, and will continue to grow at 15-17%.

-

Order book is around Rs. 3,847 Crs

-

Total active dealers are around 2038 numbers, an increase of around 33% YOY.

3 Likes

1800 crs of capex for 3x asset turns(7-8x at present) and 2000 crs of QIP in the business will lead to total asset turns declining drastically as gross block triples over next 2 years. Till the time they sweat the new assets completely, ROEs can take a hit with increasing depreciation and reducing financial leverage(Net cash). Back of the envelope calculations - ROE to come down to 15% for next 2 years from 20% currently …consequently the stock is getting punished

1 Like

KEI Industries | Management Interview

9MFY25 margin less than 10% Vs FY25 guidance of 11%

Management said margin should normalise in Q4 to the guided range for FY25

Watch the interview here - https://youtu.be/wMkpG8S8zgQ

2 Likes

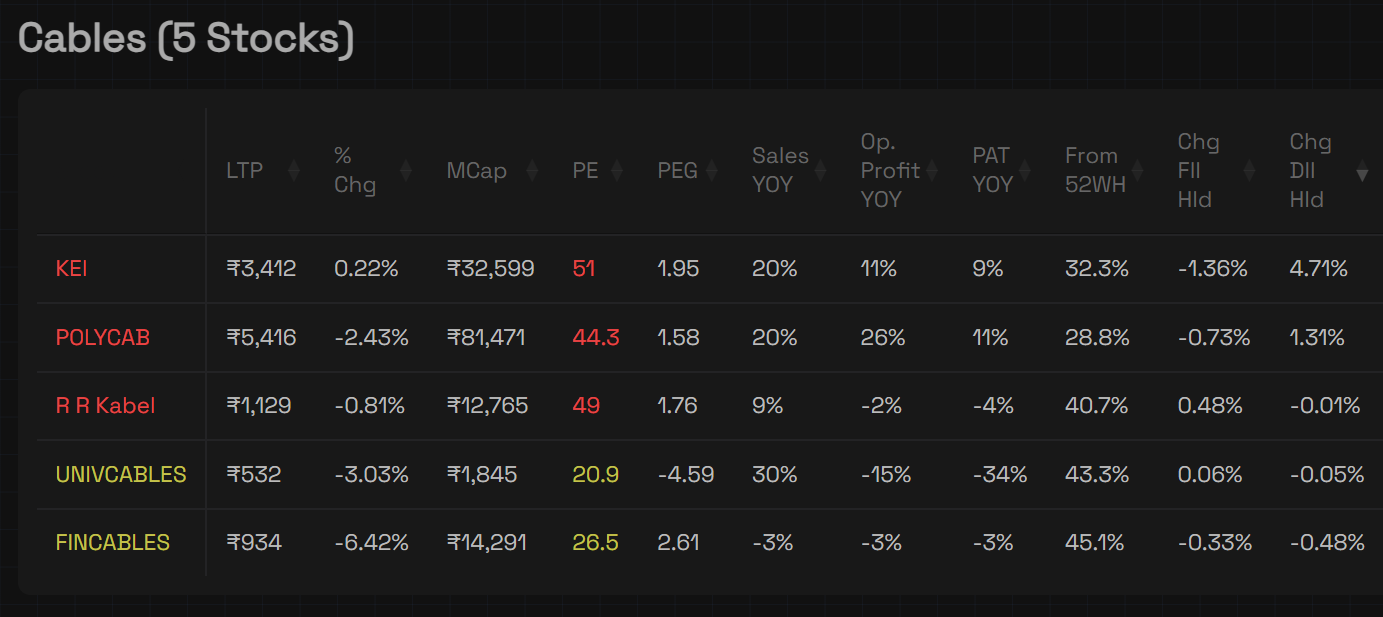

DII’s have driven KEI’s valuation to new heights. After a 32% correction, the stock is still trading at 51 PE TTM, with a growth rate of 20%.

And they continue accumilating.

Disclaimer: Not invested anymore.

With Ultratech entering the cable and wire space, share already down close to 20% in half a day trade, what is the future hold for KEI industries now?

1 Like

Markets are clearly exaggerating a lot of news. Ultratech announced its foray in C&W with capex of ~1800 cr over the next 2 years & we see today, KEI down 20%, Polycab and RR Kabel 15% and Havells down 7-8%.

KEI Ind management clearly told that it will take Ultratech Cement 5-8 years to get the brand right & will take 3-5 years for Ultratech Cement to establish plants but markets are in no mood to think and react.

I remember few days back - Morgan Stanley initiated coverage on KEI Ind with a price target of Rs 4391 & forecasted a 23% earnings CAGR for FT25-28. Yes, with competition emerging now, the multiples may come down, but it will take atleast 3-5 years to make a meaningful dent in the market.

With 1800 cr investment and 4-5 asset turnover, Ultratech’s revenue potential turnover can be estimated at 5-7% if C&W industry in FY29e or beyond. So, 95% industry will still be with old players. And don’t forget Power transmission, industrial cables generally reqire 2-4 years for prequalification.

These are opportunities for brave hearts and potential investors? ![]()

Analysis by a Research person

10 Likes

KEI Industries, Chairman and Managing Director, Anil Gupta, believes the cables and wires industry is large enough to accommodate new players and says there is no concern about business or margins, as UltraTech Cement will take years to scale.

Also he said that “UltraTech will take a minimum of three years to start production, whatever someone may say on paper about two years. From our long experience in developing industries, we know this process takes time”

Watch the interview

3 Likes

Management view :

(349) KEI Industries Share Price Plunges 20% In Trade | Here’s What Triggering The Fall - YouTube

3 Likes

So what is next? Is it a knee jerk reaction and good time to buy?

let us wait for management commentary. few days ago when Birla announced a similar news, KEI management gave positive commentary and stock managed to bounce back but today, we are still waiting for the management to say something. Need to also look for Polycab management commentary

1 Like

Additionally, I will track the sales growth and profit margins. Not sure how much investment they are going to put in and the timelines. I learned that Wires have low entry barriers but Cables have high entry barriers so need to see how that plays in real-time.

Disc: Invested and added more today.

2 Likes

Also, it is important to see what areas of cables and wires the new entrants plan to get into. KEI specialises in UHV cables. Would deep pockets really make a dent in that segment in a short timeframe? I suppose it will take anyone many many years. I’d say, if anything, Polycab faces a higher risk than KEI from new entrants.

4 Likes

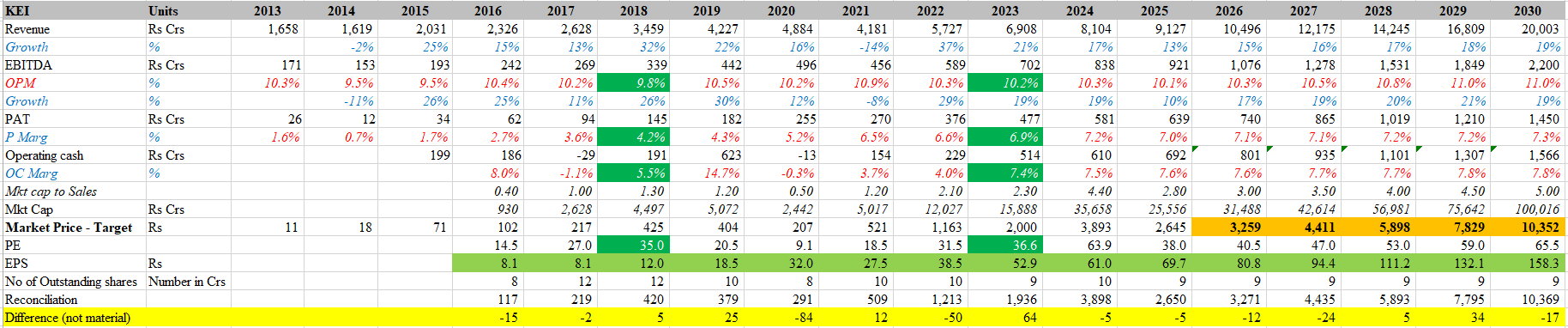

Here is my two cents on the valuation and price visibility of KEI in long term.

Suggestion invited to make this more rational and close the estimates.

Growth in revenue 17-20% & Margins till 11% based on current capacity expansion in Sanand and recent management call of Q3, Market cap to sales estimated based on Polycab todays numbers.

DIs: not an analyst, invested,

Source data - Screener

1 Like

My back of the envelope calculations appear to tell similar story.

As per management commentary (in past and Q3), they are looking to target 25000Cr revenue by 2030 (20% CAGR sales). They had hinted at better OPM than current (13 to 13.5%). Considering increasing domestic competition and ever evolving tariff situation, they might see some pressure on OPM. Chinese players might dump heavily in Australia and EU region. However no one can predict how global export trend will look like in near future, but having heard KEI management during concalls for some time, they will take appropriate calls on business/capex execution.

All these considerations might put some pressure on OPM. Taking a conservative estimate of 10-11%, the OPM might look: 2500-2750Cr by FY2030. The PAT margin might come out to be 6.5 to 7.5% i.e. 1600 to 1800Cr on conservative basis. So the 5 year forward PE ratio looks reasonable: 13 to 15 ish. Mr. Market might reward this ~20% grower business with PEG of 1.5? Then we are looking at a doubler in 5 years time with ~15% CAGR returns on a conservative basis.

Disclaimer: Invested in the stock from 3-4 years, adding in small quantities. Not a buy/sell recommendation.

2 Likes

I think PE of 15, doubler in 5 years at an growth rate of 20% is far too conservative. World largest cable and wire companies with a market cap of $ 500-900 billion trades at 11-13 PE.

My sense is it will command a PE north of 50 at a PAT of 1400 Crs +

1 Like