Thanks @alexander and @sahil_vi for your insights on KEI. Here are my 2 cents:

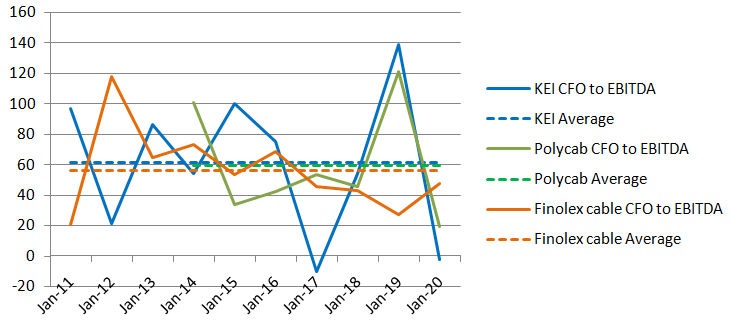

Check on CFO to EBITDA:

This check is to find out how much of the EBITDA is converted into operating cash. The ratio is very erratic for KEI and varied widely across years, however the same is observed in two of its peers viz. Polycab and Finolex cable. The average, though, is almost identical within these companies with KEI slightly better than the rest.

Auditor Check:

From FY12 to FY17, the auditor was JAGDISH CHAND & CO. whereas for FY18 and FY19 the auditor was Pawan Shubham & Co. I was doing checks in Google but did not find anything adverse for both these auditors. The auditor’s fees did not increase significantly over years and is way lower than company’s profit growth. Hence, any possibility that the company is bribing the auditors to fudge the books, can safely be ruled out.

Remuneration of key managerial personnel

The compensation of the key managerial personnel is extremely high and they seem to utilise the maximum limit allowed under company act. Growth of the remuneration is almost similar to profit growth of the company. Apart from high compensation, no anomaly found.

The company delivered better ROCE and sales growth than its peers (Polycab and Finolex cables). Naturally, the CAGR growth of its share price exceeded that of Polycab and Finolex. Overall the company looks fundamentally alright. I could not figure out the moat of the company, seniors can throw more light on it. Why someone will prefer KEI over Polycab of Finolex cables is a question.

Per se, the domestic use of cable seem to be a limited growth driver for any cable manufacturer, and I think the non-retail and industrial market is the main contributor of the growth [my ancestral house did not undergo any meaningful electric wiring revamp in last 30 years]. Unlike a paint or an adhesive company, most likely, cables have more or less one time use in each household. Please correct me if this interpretation is wrong.