Stainless steel bracelets finished well add a lot to a watch and it’s quality perception. The Tissot PRX (A sub 1000$ watch) is appreciated not only for it’s movement but the integrated SS bracelet. If they can get approval for supply to some of the more lower end Swiss/Japanese watch makers like Tissot,Seiko,Orient etc , it can be a huge recurring revenue source. (Tissot,Seiko,Longines etc sell Billions of Dollars of Watches every year,bracelets on their higher end watches can contribute as high as 10-15% to COGS).

6 Likes

High end good bracelets retail for around Rs 10000. A Good bracelets may have same revenue potential as a good dial. So effectively we are talking about potential of doubling revenues if plan and execution falls in place.

So 25cr is not huge investments.

A sample

https://www.amazon.in/Ceramic-Bracelet-Silver-Stainless-Deployment/dp/B07M9XZ28N/

3 Likes

Q2 ConCall Summary

https://x.com/amannaprerana/status/1727313135650951255?s=61&t=_sKVYHr1p58inm8VOpUs3g

2 Likes

Hi, why is the CFO/EBITDA only about 50% for the years 2019-2023? For its subsidiary Ethos, it’s even worse. Any thoughts on this?

You have shared ETHOS’s SAST details in KDDL’s discussion. Please verify before posting.

Sorry my mistake! I will remove it

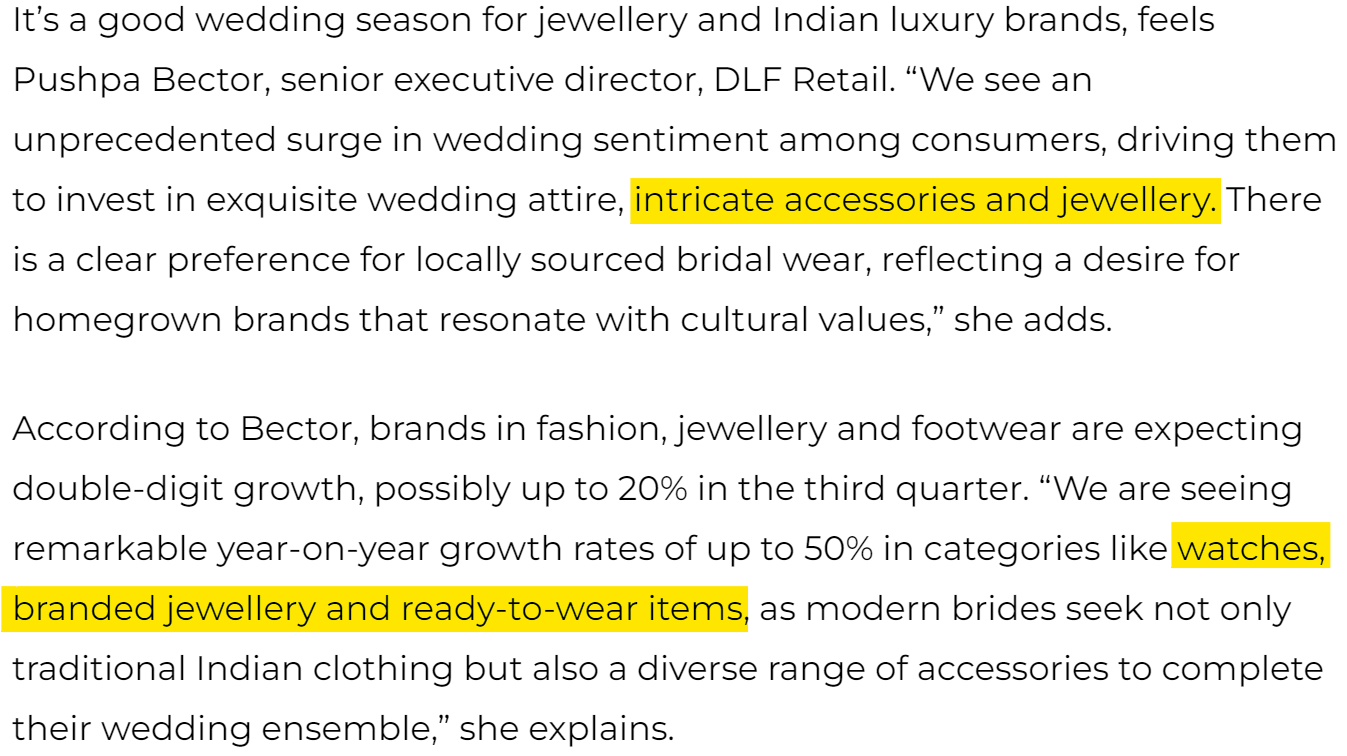

As the disposable income of Indians is at an all-time high and social media is motivating people to go a step further while spending, is it wrong to expect a good jump in the quarterly numbers this time?

4 Likes

Mohit Ji, May I request you to please share the link of above Transcript

Sure

https://www.financialexpress.com/business/industry-the-big-fat-indian-wedding-business-3310689/

1 Like

3 Likes

Can Titan or other retail jewellers disrupt this model or take market share from Ethos ?

Tata is already in this segment with Helios but unlike Ethos, it doesn’t currently deal in the ultra-luxury segment yet (won’t). There is also Tata Cliq Luxury (orders fulfilled by Helios) but none of these provide the boutique experience and exclusivity like ethos, not even close. Jewellers like Malabar sell watches too but has been a flop scene.

2 Likes

When you say “won’t” , do you mean that Titan dont want to ,as in its not in their plan or is it that Ethos has already gain exclusive partnerships with these luxury brands?

Ethos Limited Q3FY24 concall summary, please add your thoughts or any corrections

Key Financial Highlights – Q3 FY24

● Revenue of Rs. 281.2 crore with 22.4% YoY growth

● EBITDA of Rs. 50.8 crore with EBITDA margin of 17.7%

● PAT grows to Rs. 25.5 crores in Q3FY24 vs Rs. 20.7 crore in Q3FY23

● Strong revenue growth across offline and online channels

● A higher share of in-house brand sales continues to aid margin expansion

- Potential benefits from an India-Swiss FTA could aid Ethos in saving currency rate costs, targeting 13-14% SSG for the decade, and 46% repeat customers. RIMOWA store profitable from the 1st month, CPO rev 49cr for 9mFY24

-

Planning to launch Favre leuba globally by Aug24 at a watch event.

-

Guidance of 25% rev growth for decade, aims to be top 3 retailer by this decade and currently has 20% market share in luxury watch segment.

-

Plans to open 15-20 new stores in FY26, with 25 planned for FY25; still in the testing phase for jewelry; considering adding a maximum of 2 more boutique luggage stores in the next 12-15 months.

-

Opened 1 new store in Q3, unaffected by inflation, and witnessed bumper earnings from the stock market.

-

Exclusive brand contracts range from 5-9 years, with marketing costs shared, aiming for >40% market share by the decade.

-

Payback period for stores is 3 years, with a CAPEX and WCInv of 7.5Cr per store (same guided in last call).

-

Margin expansion strategies include leveraging operating leverage, normalizing CHF/INR rates, and increasing EB watch sales.

-

CPO growth is gradual, focusing on building relationships; RF Brands (which ethos incorporated it this month Feb24) will distribute watches below 1 lac price point to retailers (expect high sales but lower margins going ahead on a consolidated basis).

-

Previously were not focusing on >1 lac watches but the watch brands find them as preferred brand to distribute their watches, therefore incorporated RF brand where they will act as a distributor to distribute to other retailers in the >1 lac price point watches, RF brand will hold inventory of 2 months, sale to be on hand and inventory risk to be brone by the retailer means planning no credit sales . Therefore high sales but expect less margin.

-

Hiring 6 people per store for FY25 (as they planned 25 stores for FY25), with 60 people hired this fiscal year, therefore expect the employee cost to be high for Q3 and Q4 of FY24.

-

Favre Leuba targets 100,000 volume sales at CHF 2500 ex-factory price in FY25-26, aiming for higher margins.

-

Top cities: Delhi with 9 stores, Mumbai with 10 stores.

-

No issues with watch shipment due to the Red Sea situation.

-

Focus on expanding watch and store offerings; facing challenges in hiring skilled watchmakers for CPO therefore not focusing much on it.

-

Their framework is to maintained long term relationships with brands; they have 60 brands as of now which have been for a long time in the middle just signed out 7 brands.

-

The CPO business is usually 35% of luxury watch retailers, refer Ahmed Seddiqui for Middle east and Hourglass for South East Asia which had first mover advantage in their region for luxury watches, study their case studies for more idea on how ethos can move ahead.

8 Likes

Just sharing what I found about KDDL on Twitter.

Please check the below link for the source.

https://x.com/LearningEleven/status/1758700503427395695?s=20

Hope this helps

Disclaimer - Holding at average of 2000 and Biased.

dr.vikas

3 Likes

As ETHOS is hitting new high and at 85 PE. KDDL is consolidating and available at 35 PE. We understand there is discount of holding company. However, KDDL has his own business of watch dials/hands etc.

Any thing I miss, why KDDL is not moving?

D: Invested

4 Likes

KDDL’s own business is not growing. See this quarter’s numbers.

3 Likes

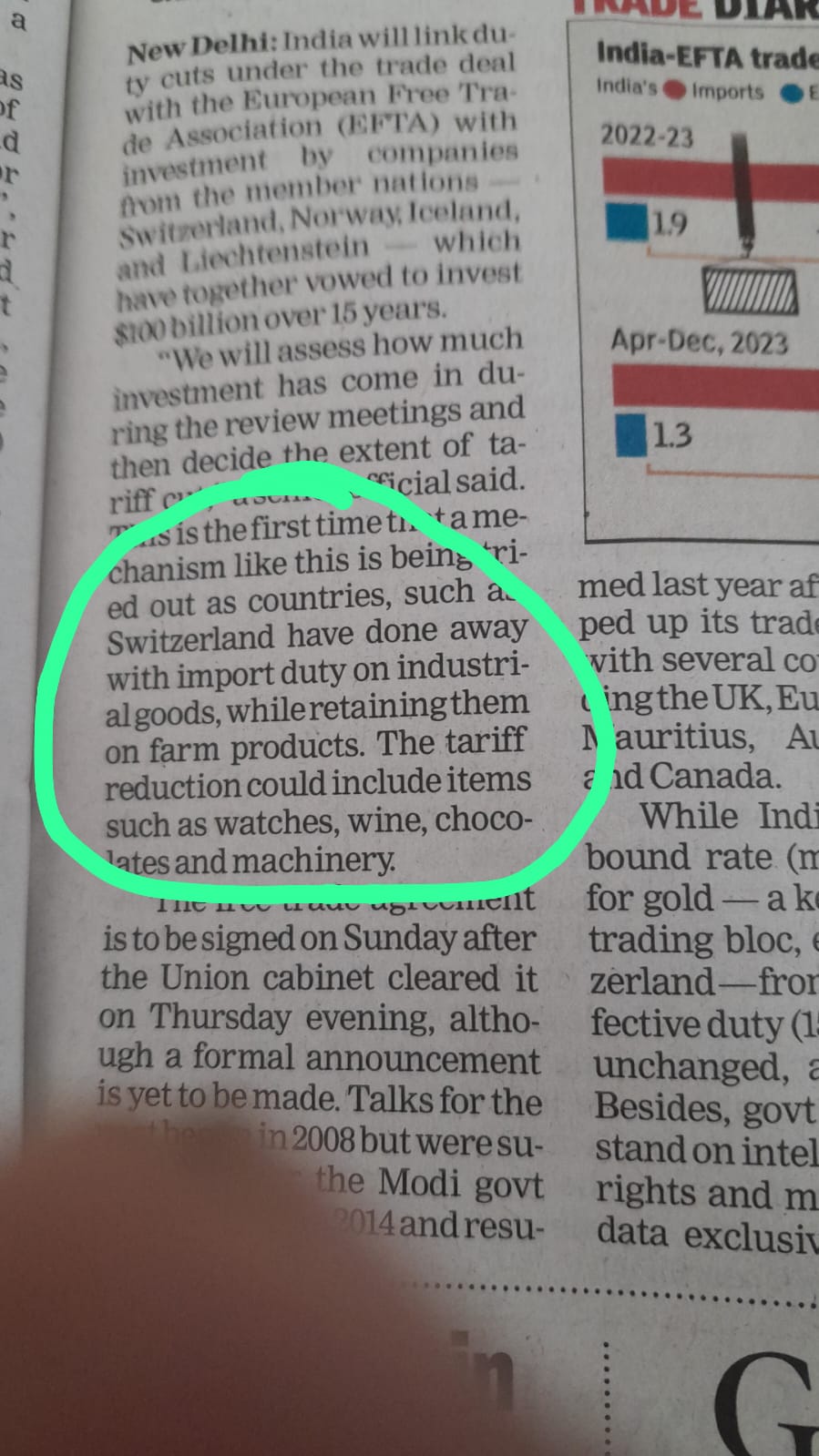

EFTA deal news dated 09/03/3024.

EFTA Deal: EFTA deal: Tariff cuts to be linked to investment by companies | India Business News - Times of India (indiatimes.com)

6 Likes

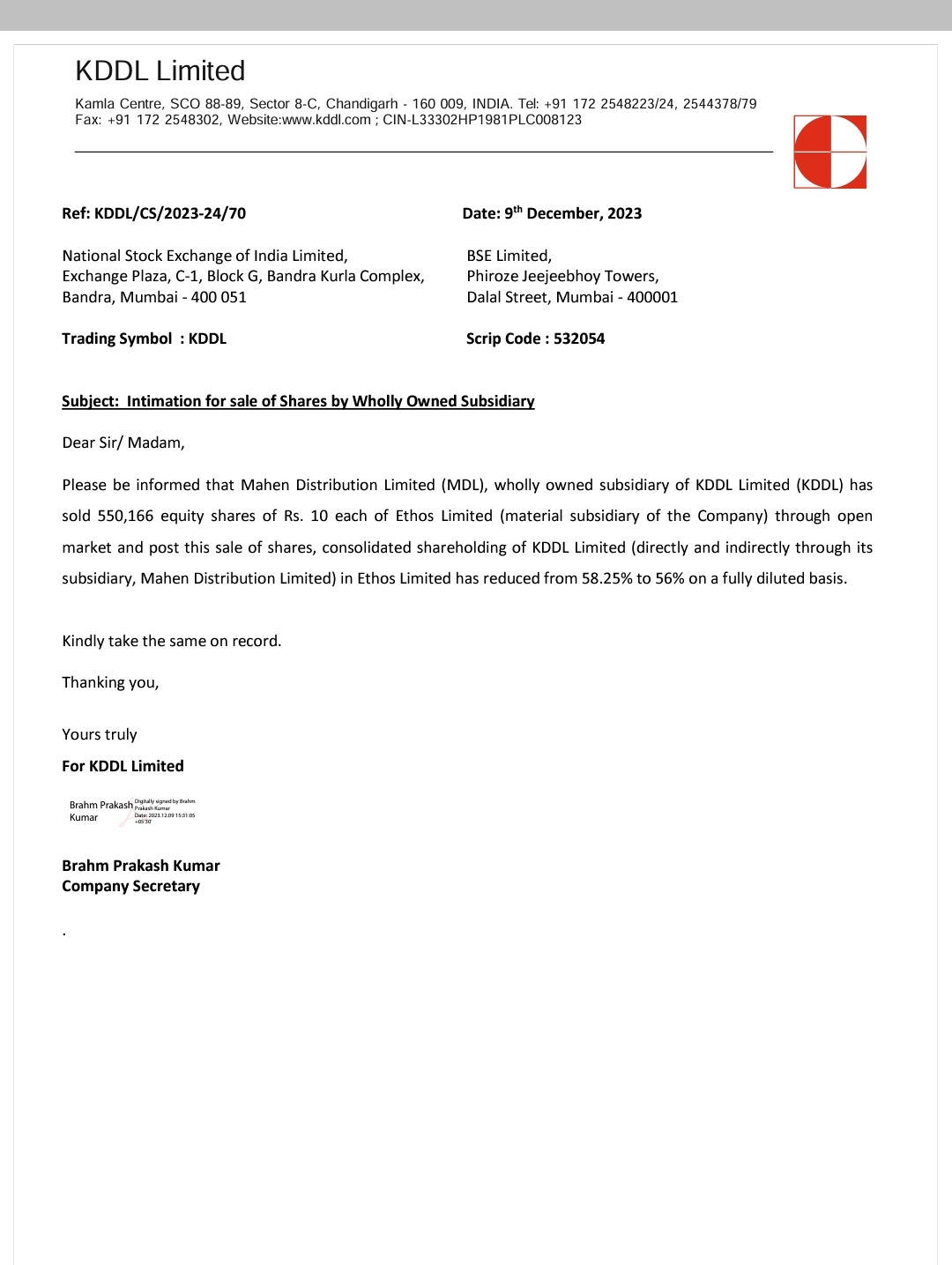

What is it with Ethos suddenly reducing their stake in Silver City? That recent notification was really perplexing, and the market doesn’t seem to like it either? Anyone got any clue kn this?