Update #5 || Feb 21, 2026

Portfolio Index

|

Index |

Period Return |

Source / Method |

| Portfolio |

106.6 |

+6.63% |

Fresh capital addition normalized |

| Nifty 500 |

98.9 |

-1.05% |

NSE close 23,644 (Dec 19, 2025) → 23,395 (Feb 20, 2026) |

| Alpha |

|

+7.68% |

|

Index methodology: Return is computed using the Modified Dietz method per bucket — cash injections are removed from the numerator so performance reflects genuine price movement, not capital deployment. Net fresh capital this period was +1.9% of portfolio. Base = Dec 21, 2025 (Index 100). Nifty 500 current = 23,395 confirmed (smart-investing.in, in.investing.com; NSE closed Feb 21 Saturday). Nifty 500 base ≈ 23,644 (estimated from surrounding trading days; will be locked once verified from NSE records).

Capital Flows (% of Portfolio)

| Portfolio |

Direction |

% of Total |

| Self India — 5 tranches (Jan 14, Jan 23, Jan 27, Feb 1 ×2) |

Cash in |

+2.4% |

| Mother India — 3 tranches (Jan 1, Jan 16, Feb 9) |

Cash in |

+1.6% |

| US — 3 withdrawals (Jan 13, Jan 22, Jan 26) |

Cash out (profit repatriation) |

-2.0% |

| Net injected |

|

+1.9% |

Bucket Performance

| Bucket |

Allocation (U1) |

Period Return |

| Self India Direct Equity |

65% |

+4.37% |

| Mother India Direct Equity |

21% |

+12.49% |

| Self US Direct Equity |

8% |

+12.96% |

| India MF SIPs |

6% |

+2.19% |

1. Self — Indian Direct Equity (~64%)

Positions below 0.2% of portfolio are summarised as Tracking Positions.

| Company |

Avg Price |

Weight |

Unreal. G/L |

Strategy |

| Balu Forge Industries |

₹338 |

7.93% |

+45.40% |

Hold; reduce on price above 600 to rebalance. Revenue from defense line to be watched. |

| EFC (I) Ltd |

₹295 |

7.07% |

-10.85% |

Hold; track execution and seat occupancy above 90%. EBIDTA margin depression mainly due to accounting norms. |

| Power Mech Projects |

₹1,789 |

6.45% |

+22.16% |

Hold; track cashflow. Main trigger O&M revenue to ramp up. |

| P N Gadgil Jewellers |

₹613 |

6.04% |

-8.25% |

Hold; awaiting consumer recovery. |

| Yatharth Hospital |

₹445 |

5.80% |

+61.67% |

Hold; reduce if valuation stretches. |

| Zaggle Prepaid |

₹315 |

5.55% |

-25.53% |

Reduce on >15% jump to rebalance. — Q3 results positive; stock divergence review. Cashflow positive in next quarter result is key trigger along with AI based disruption in business. Reduce on >15% jump to rebalance. — Q3 results positive; stock divergence review. Cashflow positive in next quarter result is key trigger along with AI based disruption in business. |

| S J Logistics |

₹361 |

4.66% |

-11.06% |

Hold; awaiting financial year end results. Working capital days reduction and cashflow to be analyzed. |

| K.P. Energy |

₹200 |

4.27% |

+47.25% |

Hold, business performance and execution remains strong. Strong order book. |

| Manorama Industries |

₹1,368 |

4.19% |

+3.73% |

Hold. Amazing execution, next 3 year growth visibility |

| Satin Creditcare |

₹148 |

4.16% |

+4.60% |

Hold for MF upcycle |

| Transrail Lighting |

₹524 |

3.81% |

+8.49% |

Hold. Watch cashflow and order book building. |

| Capri Global Capital |

₹182 |

3.72% |

-5.03% |

Hold; Q3 was good. Q4 validation needed |

| Sammaan Capital |

₹123 |

3.72% |

+25.37% |

Hold, turnaround story. |

| Vishnu Chemicals |

₹363 |

3.71% |

+41.18% |

Hold, expected gains of Cr mine to kick in FY27. |

| Techno Electric |

₹1,106 |

3.69% |

+3.47% |

Hold; EPC order pipeline key. Vision for 2.0 provided, watch development in data centre theme. |

| EPack Prefab |

₹243 |

3.39% |

-22.45% |

Q3 results were bad, watch Q4 to meet full year guidance. Accumulate after that. — see churning |

| Danish Power |

₹815 |

3.36% |

-18.65% |

Hold with some tax loss harvesting. Guidance was strong, wait for year end results and cashflow. |

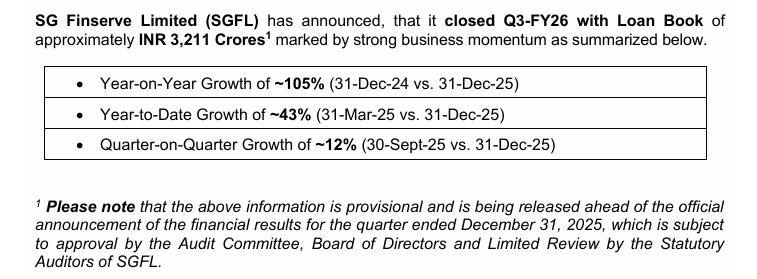

| SG Finserve |

₹392 |

3.31% |

+4.82% |

Hold |

| Waaree Energies |

₹2,946 |

3.11% |

-1.63% |

NEW — Q3 results outstanding; diversification outside Solar and tariff war subsiding along with China subsidy on exporters reduced is favorable. |

| Vilas Transcore |

₹402 |

2.54% |

+4.50% |

Hold to monitor execution in Q4. Realizations expected to be low but margin to be intact. |

| Motilal Oswal FS |

₹629 |

2.48% |

+22.22% |

Hold. Add if >15% correction, long term wealth management play. |

| Cartrade Tech |

₹2,099 |

2.27% |

-5.74% |

NEW — Q3 record quarter; watch out how ad revenues go down with uptick in auto sector. |

| Shanti Gold Intl |

₹206 |

2.27% |

+2.87% |

Hold, exit on >20% jump as hedging principles on gold are weak. |

| Emerald Finance |

₹76 |

2.24% |

-15.80% |

Hold with some tax loss harvesting. If guidance missed in Q4, exit. |

Tracking Positions (< 0.2% weight, 1-share or near-exit residuals): Balaji Amines, Blue Jet Healthcare, Ceinsys Tech, Coforge, CSB Bank, Data Patterns, DDev Plastiks, Deepak Fertilisers (residual tracking share), Deepak Spinners, Dynamic Cables, Epack Durable, Garware Hi-Tech Films, Gujarat State Fertilizers, Hind Rectifiers, Indiamart Intermesh, Interarch Building, Optiemus Infracom, R R Kabel, Stallion India Fluorochemicals, TCC Concept, Urban Company, Varanium Cloud, Varun Beverages, Zen Technologies.

2. Mother — Indian Direct Equity (~23%)

| Company |

Avg Price |

Weight |

Unreal. G/L |

Strategy |

| Sky Gold & Diamonds |

₹162 |

30.79% |

+122.70% |

Hold; good plan presented until 2030. Watch cashflow targets being met or not. |

| TD Power Systems |

₹336 |

12.54% |

+162.47% |

Hold; guidance upward revision key. Trim if PE crosses 70. |

| Jeena Sikho Lifecare |

₹728 |

8.24% |

-5.11% |

Hold; building on correction. Amazing execution and growth guidance. |

| Power Finance Corp |

₹360 |

6.99% |

+13.99% |

Hold; dividend + value |

| Time Technoplast |

₹180 |

6.69% |

+8.87% |

NEW — entered on >40% correction. Good guidance with new capacities and lines getting live in Q1FY27 |

| Smartworks Coworking |

₹464 |

5.49% |

-5.32% |

NEW — Watch on cashflow getting converted into profit. |

| NCC Ltd |

₹198 |

5.34% |

-24.58% |

WC trigger still unactivated, promoter buying. Watch orderbook target met or not after Q4. |

3. Self — US Direct Equity (~6%)

| Company |

Avg Price |

Weight |

G/L |

| AMD |

$147 |

21.7% |

+36.15% |

| QQQM |

$111 |

21.4% |

+125.42% |

| Micron Technology |

$206 |

13.6% |

+108.03% |

| MicroStrategy |

$159 |

11.3% |

-17.58% |

| ASML Holding |

$848 |

11.2% |

+73.37% |

| Vertiv Holdings |

$126 |

10.5% |

+93.75% |

| Marathon Digital |

$8.47 |

10.3% |

-5.94% |

4. Self — India MF SIPs (~7%)

Unrealised return: +22.37% | XIRR: 13.86% SIPs: Helios Flexi, Mirae Mid, Quant Small, Quant Momentum. Pausing/restarting selectively.

Churning Log (Jan 2 → Feb 21, 2026)

Personal India

EXIT — Shyam Metalics & Energy Rationale: Booked gains from a cyclical metals name after +159% gain. Capital redeployed to higher-conviction ideas. Latest developments: Steel/metals sector faces ongoing margin pressure from Chinese overcapacity dumping. Domestic demand softening in H2 FY26. Right time to have exited. Verdict:  Excellent — booking cyclical multibagger gains on schedule.

Excellent — booking cyclical multibagger gains on schedule.

EXIT — Deepak Fertilisers (position reduced to tracking share) Rationale: +125% gain largely represents the fertiliser cycle call made at entry. Retaining 1 tracking share. Latest developments: Fertiliser stocks globally correcting as urea prices moderate. DFPCL’s Q3 FY26 revenue grew modestly but margins compressed. No strong next leg visible near-term. Verdict: Good — not overstaying a cycle play. Tracking share preserves optionality without commitment.

EXIT — Bajaj Housing Finance Rationale: Build was slow due to lack of fresh capital; opportunity cost too high versus conviction names. Latest developments: BHFL Q3 FY26 — loan book grew ~25% YoY, asset quality holding. Business is fine, but the stock has been range-bound since its IPO pop. No near-term rerating catalyst. Verdict: Neutral — the thesis was long-term and hasn’t broken. Exit was about capital allocation priority, not stock failure.

NEW — Waaree Energies (₹2,946 avg, 3.11% weight) Rationale: India’s largest solar module manufacturer. PLI beneficiary, strong US export presence, capacity expansion in full swing. Latest developments (Q3 FY26, Jan 22, 2026): Record quarter — revenue +119% YoY to ₹7,565 Cr; EBITDA margin expanded to 25.5% (highest ever); PAT +116% YoY. Order book at ₹60,000 Cr, providing multi-year visibility. First Indian manufacturer to achieve 1GW+ module production in a single month. Raised ₹1,000 Cr equity for 20GWh battery facility. Management raised EBITDA guidance to ₹5,500–6,000 Cr for FY26. Stock rallied ~9% post-results. Entry context: Entered at ₹2,946 near correction lows vs ₹2,640 post-result price — entry timing slightly early, but thesis fully validated by results. Verdict: Strong — fundamental thesis confirmed emphatically. Hold and possibly add on dips.

NEW — Cartrade Tech (₹2,099 avg, 2.27% weight) Rationale: Digital auto classifieds platform with improving unit economics. Upgraded from tracking list after conviction increased. Latest developments (Q3 FY26, Jan 28, 2026): Record quarter — revenue +18% YoY to ₹228 Cr; EBITDA +56% YoY; EBITDA margin hit all-time high of 37%; PAT +35% YoY to ₹62 Cr. All three segments (Consumer, Remarketing, OLX India) delivered record revenues and margins. CarDekho acquisition shelved — management confident enough in organic growth. 85Mn avg monthly unique visitors, 95% organic. JM Financial upgraded the stock post-results. Entry context: Entered at ₹2,099; stock at ~₹1,978 currently (-5.74%). Post-results, stock rose to ~₹2,536 intraday but has pulled back. The market hasn’t fully re-rated this yet. Verdict: Good entry — results validate thesis. Price underperformance is market overhang, not fundamental. Patience warranted.

ADD — Manorama Industries (weight: ~2.8% → 4.19%) Manorama Industries is a specialty fats/cocoa butter equivalent player.

Mother India

EXIT — Federal Bank Rationale: Blackstone investment thesis partially played out; capital redeployed. Latest developments: Federal Bank Q3 FY26 — NII growth moderate at ~10% YoY, CASA ratio stable. Blackstone strategic angle not yet fully priced in. The exit may have been slightly premature if the private equity angle materialises. Verdict: Disciplined — partial thesis exit, not a full thesis break. Monitor for re-entry.

EXIT — Rolex Rings Rationale: Auto forging weakness — no near-term catalyst. Latest developments: Auto ancillary sector broadly weak in H2 FY26. EV transition headwinds to forging volumes. No guidance upgrade expected in near quarters. Verdict: Correct — exiting a cycle stock without a catalyst is the right discipline.

EXIT — Bellacasa Rationale: New capacity not showing margin improvement; execution uncertainty rising. Latest developments: No major analyst coverage updates. Capacity expansion plays typically need 2–4 quarters post-commissioning before margins improve. Exit may be slightly impatient but avoids further capital impairment if execution delays persist. Verdict: Marginally impatient — original thesis wasn’t wrong, just slow. However, holding through execution uncertainty in a small-cap is high-risk. Exit defensible.

NEW — Time Technoplast (₹180 avg, 6.69%, +8.87%) Rationale: Rigid plastic packaging + EV battery casings. Tracked from personal watchlist (U2) before entering. Latest developments (Q3 FY26): Revenue +29% YoY, driven by composite cylinders and automotive segments. EV battery casing segment growing from a small base. Management guiding for 20%+ revenue growth in FY27 on capacity additions. Entry context: Entered after >40% correction from highs. Stock has recovered +8.87% from entry, validating the technical entry. Verdict: Disciplined — tracked before buying, entered on correction, early results constructive.

NEW — Smartworks Coworking (₹464 avg, 5.49%, -5.32%) Rationale: Enterprise flex-leasing in India. Growing enterprise client roster, IPO-stage company. Latest developments: No Q3 results disclosure yet at time of writing (recently listed). Coworking sector seeing strong enterprise demand from MNCs setting up GCCs in India. Comparable listed player IWG (UK) reporting strong India pipeline. Entry context: -5.32% from entry, early days. The sector thesis is sound but IPO-stage execution risk is real. Verdict: Too early to judge — needs minimum 2 quarters of post-listing results. Watch occupancy rates and enterprise client adds.

Self — US

Overview of US portfolio reshaping (Dec 21, 2025 → Feb 21, 2026):

| Ticker |

U1 Wt |

U5 Wt |

Δ Weight |

U1 Shares |

U5 Shares |

Δ Shares |

$ Moved |

Action |

| QQQM |

41.4% |

21.4% |

-20.0pp |

89.3 |

39.8 |

-49.5 |

-$12,639 |

TRIM |

| AMD |

27.6% |

21.7% |

-5.9pp |

72.5 |

50.5 |

-22.1 |

-$4,559 |

TRIM |

| MU |

7.9% |

13.6% |

+5.7pp |

16.3 |

14.8 |

-1.5 |

-$528 |

PRICE DRIFT |

| MSTR |

5.1% |

11.3% |

+6.2pp |

24.3 |

40.3 |

+16.0 |

+$1,990 |

ADD |

| VRT |

5.3% |

10.5% |

+5.2pp |

18.3 |

20.1 |

+1.7 |

+$348 |

ADD |

| MARA |

5.7% |

10.3% |

+4.6pp |

478.6 |

605.4 |

+126.8 |

+$928 |

ADD |

| ASML |

6.2% |

11.2% |

+5.0pp |

3.3 |

3.6 |

+0.3 |

+$337 |

PRICE DRIFT |

Gross sold: ~$17,726 · Gross reinvested within US: ~$3,604 · Net repatriated to India: ~$15,100 (3 tranches: $7,000 + $5,100 + $3,000)

TRIM — QQQM (41.4% → 21.4% | sold 49.5 shares | ~$12,639 proceeds) Rationale: A passively managed ETF ballooning to 41% of an active portfolio was a structural contradiction. Sold across 3 tranches, proceeds repatriated to India. Latest developments: NASDAQ 100 drifted ~5% lower in Jan–Feb 2026 on mixed tech earnings and rate uncertainty. QQQM’s G/L compressed from +133.63% (U1) to +125.42% now — confirming the trim captured near-peak values. Verdict: Excellent process — long overdue concentration fix. The only self-critique: why wait until U5? This trim could have started at U2/U3 and been executed more gradually at higher prices.

TRIM — AMD (27.6% → 21.7% | sold 22 shares | ~$4,559 proceeds) Rationale: Rebalancing alongside QQQM trim; AI chip thesis remains intact. Latest developments (Q4 2025, Jan 28, 2026): Revenue +24% YoY, data center segment +69% YoY to $3.9B. But Q1 2026 guidance of $7.1B missed consensus $7.4B, citing near-term inventory digestion. Stock fell ~6% post-results. G/L has compressed from +51.23% (U1) to +36.15% now. Verdict: Well-timed — the trim inadvertently front-ran a guidance disappointment. AI chip thesis long-term intact; current weight of 21.7% is appropriate.

PRICE DRIFT — MU (7.9% → 13.6% | sold 1.5 shares | negligible) Context: MU’s weight jumped 5.7pp entirely because the stock doubled (+108% G/L vs +32% at U1). The 1.5 share reduction is a rounding artefact, not a decision. MU is now the 3rd largest US holding at 13.6% through passive drift alone. Latest developments: MU HBM (High Bandwidth Memory) revenue tripled YoY in Q4 FY25, driven by AI inference compute demand. Strong visibility into 2026 from AI data centre customers. Verdict: Needs an active decision — a stock doubling its portfolio weight passively is a flag. At 13.6%, should MU be trimmed to recycle gains, or is the AI memory supercycle thesis strong enough to hold? This needs a stated answer in the next update.

ADD — MSTR / MicroStrategy (5.1% → 11.3% | bought +16 shares | ~$1,990) Rationale: Doubled down on leveraged Bitcoin treasury exposure as a paired bet alongside MARA. Latest developments (Q4 2025, reported Feb 5, 2026): Reported a $12.44B net loss driven by $17.44B in unrealized BTC losses — Bitcoin fell 25% in Q4. Company now holds 713,502 BTC at a cost basis of $66,384/BTC. With BTC at ~$68,840 (Feb 17), holdings are barely above water. Stock is down ~66% from its all-time high of $457. Class action lawsuits allege overstated Bitcoin strategy profitability. Positive: MSCI shelved its exclusion of crypto treasury companies (Jan 6), removing a major index-flow overhang. Management established a $2.25B cash reserve for 2.5+ years of dividend coverage — some liquidity reassurance. Bitcoin “yield” (BTC per diluted share growth) hit 22.8% in 2025 despite equity dilution. Verdict: High-risk addition at the wrong moment — buying +16 shares into a stock down 66% from ATH with BTC below the company’s cost basis requires very strong Bitcoin conviction. The add was made near the bottom of BTC’s pullback which could prove prescient, but this is speculation not investment. Hard cap: MSTR + MARA combined should not exceed 20–22% of the US bucket. Currently at 21.6% — already at the limit.

ADD — VRT / Vertiv Holdings (5.3% → 10.5% | bought +1.7 shares | ~$348) Rationale: Token addition to the data centre infrastructure theme. Latest developments (Q4 2025, reported Feb 11, 2026): Exceptional quarter — Q4 organic orders +252% YoY and +117% QoQ; backlog hit $15B, up 109% YoY; book-to-bill ratio ~2.9x; adjusted EPS $1.36, beat by $0.10. Full-year 2026 guidance: adj EPS $5.97–$6.07 (+43% YoY), net sales $13.25–$13.75B (+28% organic). Stock jumped +18.49% post-results. AI data centre buildout is creating extraordinary multi-year order visibility. Verdict: Strong hold — consider meaningful add — VRT is executing flawlessly. The 1.7-share addition was negligible relative to the conviction the results justify. At 10.5% of US bucket and +93.75% G/L, there is still room to build this into a 15%+ position given the backlog strength.

ADD — MARA / Marathon Digital (5.7% → 10.3% | bought +127 shares | ~$928) Rationale: Paired Bitcoin mining add alongside MSTR; direct BTC price leverage via the largest listed miner. Latest developments: Q4 2025 results due Feb 25–26, 2026 (not yet released). Analysts expect EPS of -$0.23. Stock at ~$7.51, near 52-week low of $6.66 vs high of $23.45 — down ~68% from peak. CEO Fred Thiel warned in November: “Bitcoin mining is a zero-sum game. As more people add capacity, it gets harder for everybody else. Margins compress, and the floor is your energy cost.” MARA is targeting 75 EH/s by end-2025 and pivoting toward vertical integration (owning power assets) to reduce cost per BTC. Verdict: Speculative punt, Q4 results are the first real checkpoint — the 127-share add at ~$7–8 is a recovery bet on BTC and mining margins. Unlike MSTR, MARA has real operational revenue — if BTC recovers above $80K and hash rate expansion plays out, the stock could 2–3x from here. But if BTC stays depressed, this position will bleed. Q4 results (Feb 25) and Q1 guidance are the triggers. Define a stop-loss level before results.

PRICE DRIFT — ASML (6.2% → 11.2% | bought 0.3 shares | ~$337 — essentially unchanged) Context: ASML’s weight nearly doubled from 6.2% to 11.2% purely via price appreciation (+73% G/L). The 0.3 share addition is negligible. Like MU, this is a passive drift situation, not an active sizing decision. Latest developments (Q4 2025, Jan 29, 2026): Net bookings surged to €7.09B — dramatically above consensus of €4B — driven by EUV lithography demand from TSMC, Samsung, and Intel ramping AI chip production. ASML reaffirmed its monopoly position in extreme ultraviolet lithography; no credible competitor exists. Management guided for strong 2026 on continued AI semiconductor capex. Verdict: Thesis intact, but active decision needed on sizing — at 11.2% via drift, is this the intended weight? ASML’s monopoly position arguably justifies a large allocation, but that decision should be made explicitly, not by default. State whether to hold at 11%+ or trim to a target weight in the next update.

Critical Analysis

Zaggle — Q3 Results vs. Stock Price Divergence Q3 FY26 results (reported Feb 12, 2026) were the best ever — revenue +48% YoY to ₹498 Cr, adjusted EBITDA crossed ₹50 Cr for the first time (+63% YoY), PAT +78% YoY. Management confirmed working capital breakeven in FY26 and positive OCF by FY27. Signed 7-year Visa and 5-year Mastercard partnerships. Stock is still -25.53% from entry. The divergence between fundamentals (improving) and price (weak) is explained by institutional selling — both FII stake (8.64% → 7.61%) and MF stake (4.60% → 3.70%) declined in Q3. The market is not wrong to be cautious on a stock that’s been -35% from its 52-week high despite good results — it signals institutional confidence issues beyond just one quarter. Revised stance: Hold, not reduce. Q3 results remove the immediate exit trigger. But if FII/MF selling continues in Q4 disclosures, the weight will need to be cut. Next trigger: Q4 FY26 results + Q3 shareholding pattern.

EPack Prefab — Q3 Results: Seasonal Decline, Thesis Intact But Watch Closely Q3 FY26 results (Jan 22, 2026) showed -24% QoQ revenue decline and -43% QoQ PAT decline, causing a 10% lower circuit hit. However, management attributed this to seasonal project delays (monsoon and design approval lags), which is standard for this business. 9M FY26 revenue grew +41% YoY and EBITDA +57% YoY — on track with IPO guidance. Order book at ₹1,215 Cr (7-8 months visibility). FY26 guidance of ₹1,500–1,550 Cr maintained. Management expects Q4 to be ₹450–500 Cr (strong recovery). Also flagged: CARE Ratings noted ₹11.72 Cr fund comingling from non-IPO accounts — a minor governance note to keep in mind. The thesis is not broken, but the stock is pricing in continued execution risk. The -22.45% unrealised loss is partly mechanical (IPO stock, low liquidity, weak market). Q4 FY26 results remain the make-or-break: if guidance is met, the stock should rerate. If revenue falls short, reduce.

Waaree — Entry Validated, Now Think About Reduce Triggers Q3 results were exceptional. The only risk is valuation — at current price (near ₹2,640–2,897 range post-results), the stock trades at a premium. The US export thesis carries Trump tariff risk (solar panels from India could face reciprocal tariffs). Monitor US policy developments closely. Action: Define the first reduce trigger — suggest reducing 20% of position if US imposes >25% tariff on Indian solar modules.

NCC Ltd (Mother) — Still No Resolution Now -24.58% on a 5.34% weight with fresh capital added. NCC Q3 FY26 results not yet disclosed at time of writing. The working capital metric remains the sole trigger for any averaging or holding decision. If Q3 results don’t show WC improvement, this becomes a forced exit situation at a loss — which is worse than a disciplined exit now. Last warning before action: Q3 FY26 results are the final check. No improvement = reduce by at least 50%.

What I Am Watching

-

Zaggle: Q4 FY26 results + Q3 shareholding pattern (FII/MF trend)

-

EPack Prefab: Q4 FY26 revenue — must be ₹450–500 Cr to validate guidance

-

NCC Ltd: Q3 FY26 results — working capital is the only trigger that matters

-

US bet on crypto heavy companies

-

Waaree: US tariff policy on solar module imports

-

TD Power: Planning exit/reduce triggers for >150% gainers

-

Cartrade Tech: Market re-rating post-record Q3 — watch institutional buying

All weights are within-bucket percentages. No corpus size disclosed. Positions below 0.2% summarised as Tracking Positions. Portfolio index base = 100 on Dec 21, 2025. Nifty 500 = 23,644 (Dec 19, 2025, est.) → 23,395 (Feb 20, 2026, confirmed). Net fresh capital = +1.9% of portfolio.