No, Sinha Ji, this is not fact. @sreered is right. I am a commercial farmer by inheritance. Capsicum seeds, we buy every year very costly. We can get it free by our crop but it doesn’t work this way. Kitchen garden is different. I have Kitchen Garden too in city. I do the same what you do. But in farm there is no viability without purchasing new seeds. It is always a repeat business in Vegetables. In grains it is repeatable for two years with slightly less yeild. Companied give to farmers zero age seed with buy back guarantee. This seed is sold again to farmers to grow crops. It is asset light model. There is no cheating. Farmers know this fact that it is F1 or F2.

20 Likes

Yes, that’s true.

You can plant F2 generation seeds for one time only & that too generates lesser crop compare to F1 generation (From Kaveri).

1 Like

This has been posted in most agro threads… think it’s most relevant for kaveri though. If anyone wants to draw inferences from it for kaveri please do. Cheers

I think the main kicker would be contract farming. If large corporations get into contract farming, they will be looking to buy good quality seeds from organised players. Seeds costs only 5% of the total farming costs. So can improve demand for seeds

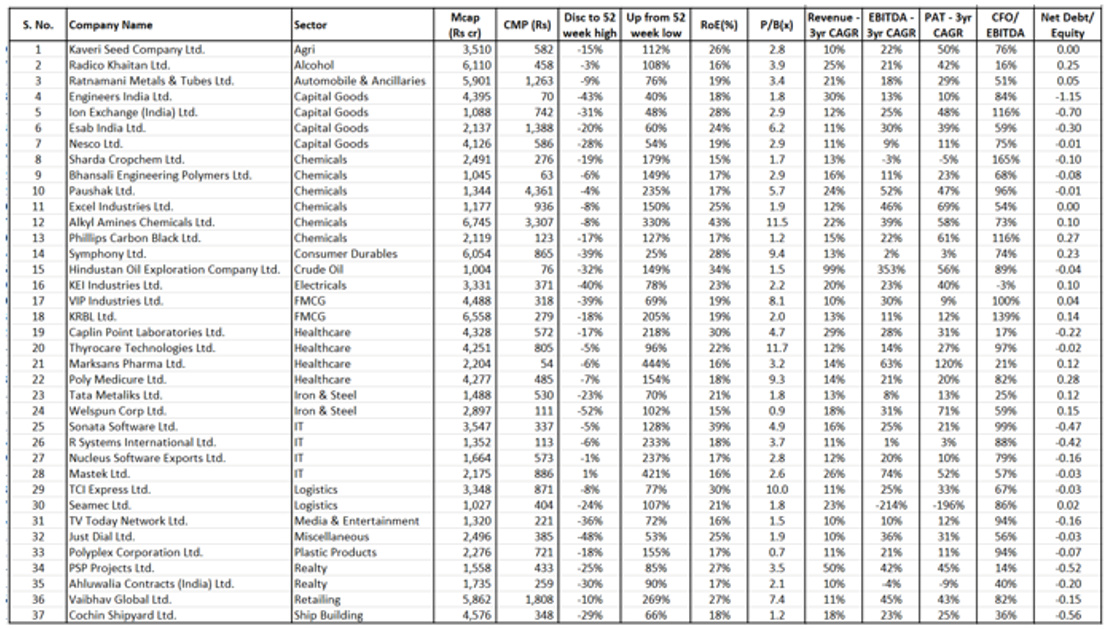

Btw, I ran some quality screens using Min revenue cagr at 10% cagr, net debt to equity < 0.3, ROE > 15% for small caps. Only around 10% of the companies in Rs1000-7000cr market cap pass this filter. Kaveri is one of them.

Source: Small is Beautiful Again...

2 Likes

In my opinion these are the two important points if someone is looking to get into Kaveri from a medium to long term:

a) Rice Hybrids: Will the growth in Rice hybrids sustain? From my own understanding and some work, Kaveri at present has a very good hybrid and is doing quite well at the same one really needs to understand the upcoming rice hybrids of Bayer-Monsanto, UPL, Rasi seeds etc.

b) Cotton: The question here is can Kveri sustain its marketshare in Cotton? If one looks from peak Kaveri’s no. of packets sold have come down but it still has a significant market share. The bigger issue in my opinion is Kaveri has lost significant market share to Rasi seeds in its home states of Telangana and Andhra and has moved to Gujarat and Maharashtra. From what I understand Rasi has a very strong pipeline of cotton hybrids and Kaveri wil lhave a tough time going ahead. There is also one significant change in crop pattern in Telangana where due to very good availability of water the farmers now have an option of moving away from Cotton to Paddy.

The one issue that will keep coming back again and again is the tax issue where Kaveri claims that it is farming income and hence has paid no tax and the IT department claims it is trading income and will be taxed as per corporate tax laws. The issue has both short term and long term ramification in short term the penalty could be significant depending upon settlement (betwen 350 cr to 1000 cr) but the bigger long term issue is that the bottomline will fall by 25% owing to newer tax structure. As an FYI seed companies like DCM Shriram pay taxes as per corporate structure.

For folks discussing Kaveri my suggestion would be to focus on seed varieties, newer hybrids, competitive positioning, talking to farmers etc. Price discussions and what an investor is buying or selling or what his competencies are is a futile discussion.

27 Likes

Hi Anant,

Thanks for your thoughtful response. How does one get data or track the market share shifts between Rasi and Kaveri?

Thanks,

The search on Kaveri Seeds was conducted in January 2018. As per IT rules, assessment will be completed within two years from the end of the month in which the last of the authorisations for search were executed. So, in all probability, the assessment orders on the Kaveri Seeds search case should have been out by know. But the timelines have also been extended due to the pandemic.

So we should be asking the company about the outcome of the assessment (if finalized). Since any adverse order will be bad for the company. Even for filing appeal, they will have to deposit 20% of demand.

Maybe Pabrai fund is privy to any adverse result of this income tax enquiry on kaveri and hence selling the shares.

Disc. Tracking

The issue with income tax and seed companies isn’t restricted to the search in 2018. It’s part of the overall tax system as seen here https://www.smartindianagriculture.com/why-kaveri-seed-monsanto-india-escape-tax-on-part-of-their-income/

For kaveri to lose the benefit of no income tax on seeds it would take an entire change in the system and considering its upto each state to do it individually i cant see this being a major issue. This issue popped up first in 2002 when companies started investing in their infra for seeds… https://m.economictimes.com/news/economy/policy/agri-income-from-seeds-may-be-taxed/articleshow/901502.cms

Nothing happened post that. Then in 2016 murmurs propped up again and yet again in 2018. I believe that there can be no outcome that can happen without an actual change in the system… and that these raids will continue for the foreseeable with the I-T dept hoping they find wrong doing so that they can get individual companies under the tax umbrella(in previous years any issue led to an audit… from Monsanto to farmers claiming seed companies were lying about leasing land to them but each time nothing happened). There’s always a threat that the government could change the overall tax structure for agri with a stroke of a pen though but that looks like the only way for it to happen(luckily the new bill had no mention of this). Last point is that kaveri has 500 cr in cash and they’ve said they’ll keep 300 cr for their warchest. This could cover the appeal if it comes down to that. And IT assessment is a period of 2 years and end of Jan wasn’t a full blown pandemic for an extension to occur(I think)

PS: The reason I mentioned Mohnish above wasn’t because he is a superstar investor or anything like that. It was because it was just a few months after this that he bought 10 percent and he would have met the management and scrutinized all of this before buying and hence why confidence in kaveri increased since we did not get a chance to do that(and hence why I even mentioned him selling above could lead to some worry if he takes away his entire position)

Disc: Invested since Id rather bet on the business prospects than worrying about regulations which could happen in any sector at any time though I do hope that the management is asked this in the next concall so that all worries go away.

2 Likes

In my opinion, the biggest factor holding this stock back is the audit issue, otherwise valuations look very good. Have collected the replies of the management (from conference calls) since the first call. People who understand the law and how these audits work, please help out

Feb-2016

- It is a routine process by SEBI to appoint a forensic audit

- It will go on. It will go on for long and they will not inform the company whether what is they are looking at and what is there in the report. That will be directly submitted to SEBI

- SEBI says this is a regular activity, nothing more

May - 2016

- It will go on because they do not have any set timeline for it given SEBI does not reveal anything to the Company regarding the progress of the audit or what they are looking at exactly. But it will take some time and we do not have any timeline as I said earlier, it will go for some more time.

- And coming back to the auditor M. Bhaskara Rao & Company is very renowned auditor in Hyderabad you can go, and see their profile in their website and they do auditing for many companies they are equally good like Big Four. Hence we appointed them as internal auditor. And we have got one more year left for existing statutory auditor.

- Everything our current auditors do in terms of credibility and capability is in line with the Big 4. And at the same time even if you look after the cost when we are getting a same service from the different reputed auditor the cost what they offered and what they are offering there is huge variation so we thought we will go with them

- Regarding the forensic audit, that was more a routine thing, in terms of SEBIs norms and as per the auditor. Another thing I want to state is we are a very transparent company and there is really nothing to hide.

May & Dec - 2017 & May - 2018

- Same status. From August 2016 to now we have not heard anything from the auditors or SEBI. We are also waiting, there is no change in the status. We do not know about when the regulatory authorities will close

- IT raids have been conducted on mostly all companies from the industry. We do not know why

Nov - 2018

- For our company, we do not have any litigation with any government departments

Aug - 2019

- Yes. As we mentioned earlier, regarding the case, we had last communication with the SEBI appointed auditors in 2016. After that, we do not have any communication

Also with regards to the taxes, some thoughts from them in the last couple of years;

- The government said that the seed value plus royalty and applicable taxes is what will derive the MRPs. And the definition of the seed value they have given as the cost incurred to produce the seed plus trade channels plus overheads plus R&D expenses plus reasonable return on the investments plus reasonable profit and scope for write-offs

- Industry enjoys a tax free status. We only pay tax on other income

- Yes, if we want to reward shareholder as we are generating cash, we want to distribute to the shareholders, we think we will continue with our stance (With regards to tax on buybacks)

- Since farmers & good farm practices are a priority for the country we do not foresee any change in the tax system, in the near future.

My personal opinion is that if some fraud was going on with the accounting, chances are that it would not take 4 years for a conclusion to be reached. Otherwise, having spent sometime understanding their competitive standing, I can tell you that they are probably in the best place (along with Nuziveedu seeds) to gain market share and dominate this industry in quite a few crops. The free cash is real and the light balance sheet and ROCE proves the good economics of the business. The trailing PE is merely 10, and based on their guidance and the recent sector tailwinds, I do not see 15-20% growth as a problem for years to come. Current selling by Pabrai could be holding prices back temporarily

Invested

16 Likes

in my my opinion kaveri seed is pure play in seed and rallis india also in seed but not pure play , rallis india had diversify portfolio, how we make diffrentiate

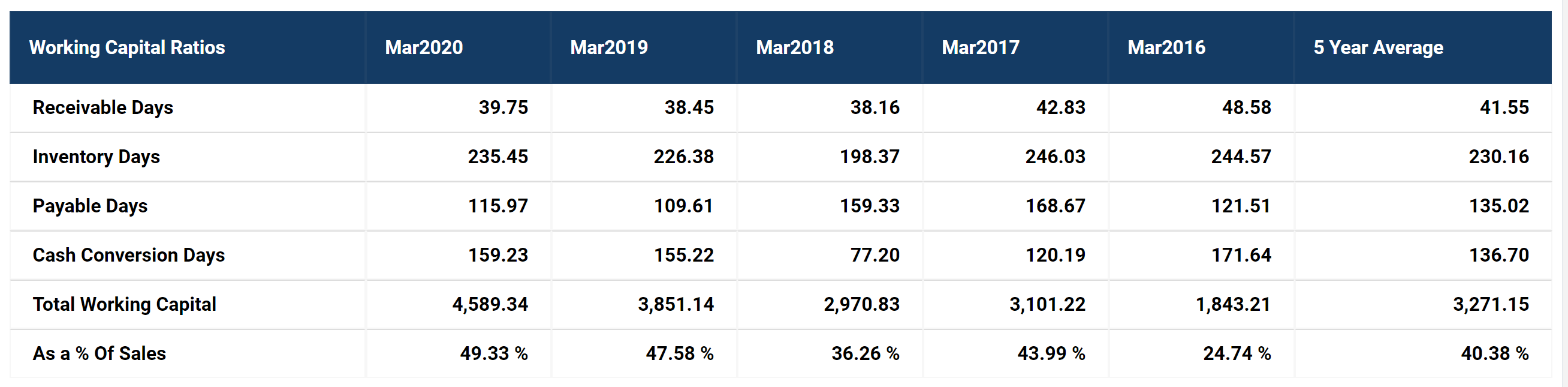

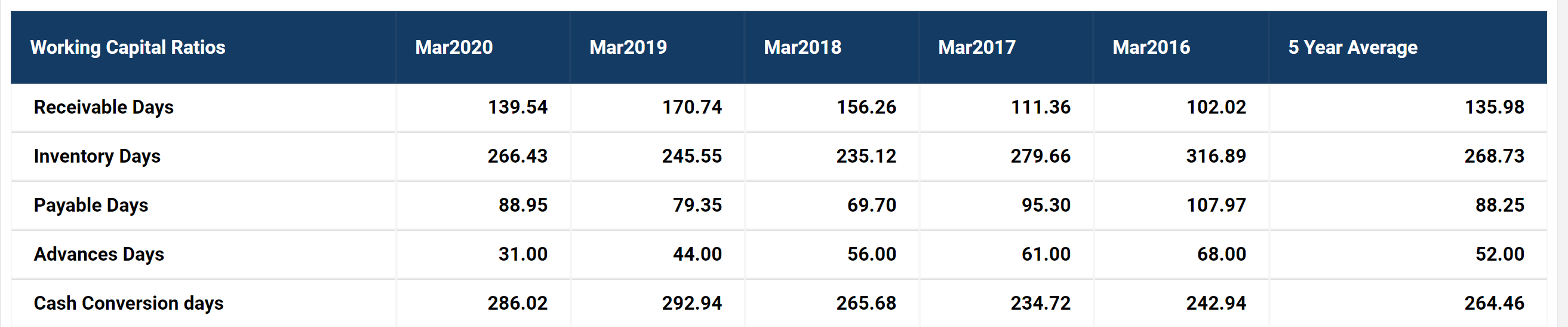

One of the other mysteries am trying to unravel is the hugely lower working capital requirement of Kaveri vis-a-vis it’s peers. Here I have compared with Nath Bio-genes, another pure seeds company. Kaveri doesn’t pay any advance to farmers to grow it’s seeds and takes advance from customers where it sells seeds. Checking with Nath, this seems virtually impossible. Heard maybe they have got bank finance for the farmers, but nothing shows up even in contingent liabilities. Anyone has clue, please share here

This one is Kaveri

This one is Nath Bio-Genes

Source:GIA Stocks

1 Like

If I’m not mistaken the business model is…

Kaveri leases land from farmers… trains them and gives them cash for expenses… and then buys the seeds from them(the good quality ones) and charges the farmers interest on the earlier expenses hence why there’s no advance as such. I can’t confirm this in the balance sheet. This is just based on their business model and was part of the reason for the income tax raid in 2018(since some farmers ended up in loss and claimed the land wasn’t being leased by Kaveri). I’m assuming nath bio follow a different process(in-house and then takes advance) but I do not know since I don’t really track it.

3 Likes

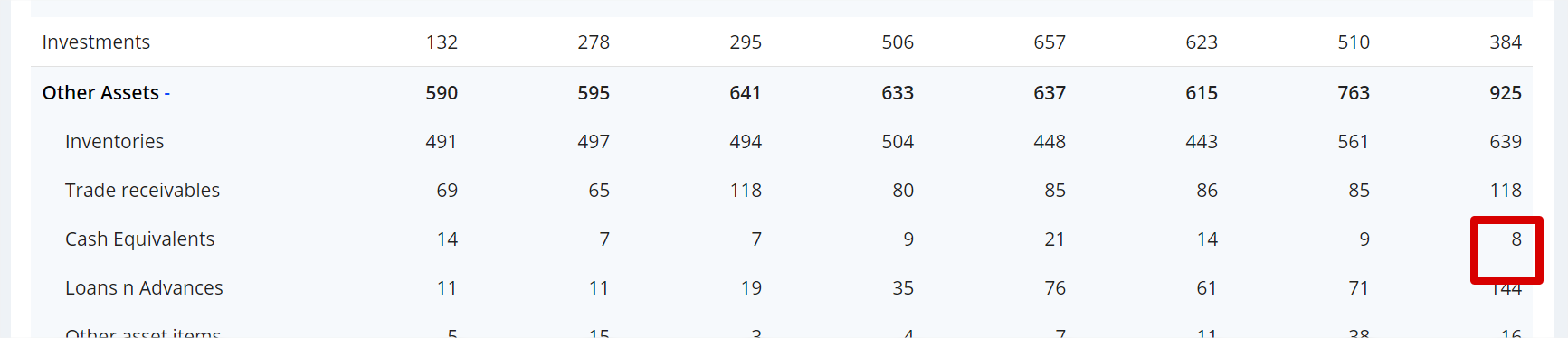

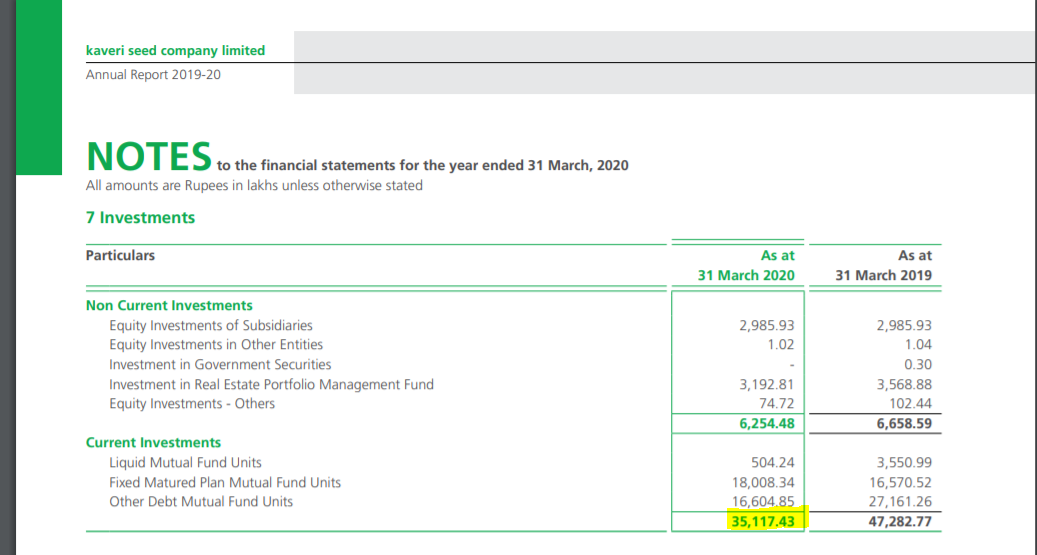

Hi, does anyone knows how much cash equivalent company has? I was reading one of the research report from August which says cash equivalent on books is 524 crore as of 30th June. But screener is showing 8 crore.

Also company has 48% of its revenue coming only from cotton which is a risk. Govt might put price control on the seed price. How do we see company mitigating this risk? Company seems available at attractive valuation. Hence wanted to understand the risk.

1 Like

Large part of Cash Equivalents is shown under Current Investments, in form of Debt instruments. That’s for Mar End. I dont know of the report you spoke about, but it does makes sense that with sales in June Quarter, the additional 160-170 Odd Crore should have freed up . Inventories have decreased substantially in June quarter and part of it should be either cash or trade receivable.

3 Likes

For Kaveri Seeds, their lowering Inventory turnover is surely a cause of concern. In 2016, they had to liquidate this at throwaway prices. The same can happen now. But if we compare the competitors, the ITO is not that low. Any insights:

Source: https://www.tickertape.in/screener?src=stocks&subindustry=Seeds&stock=KVRI&tab=valuation

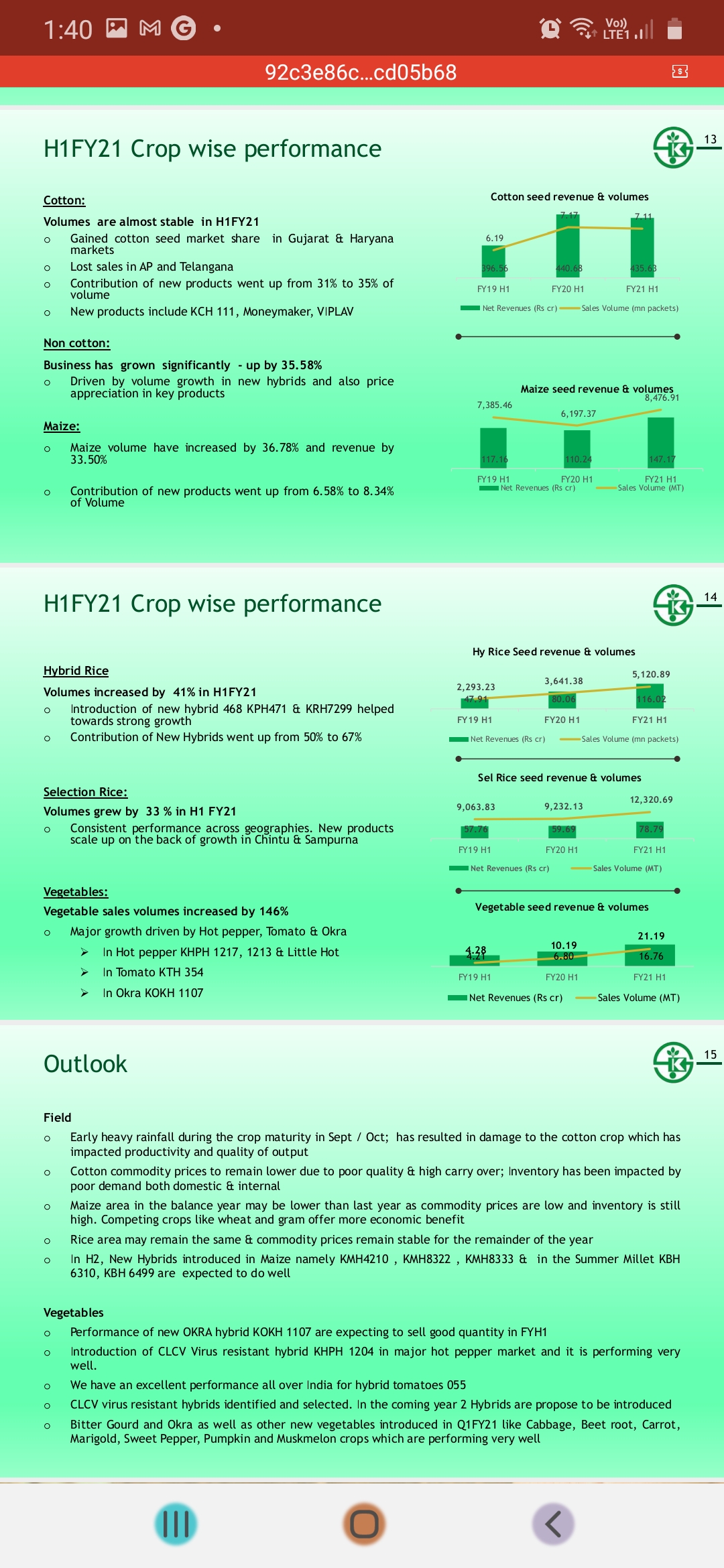

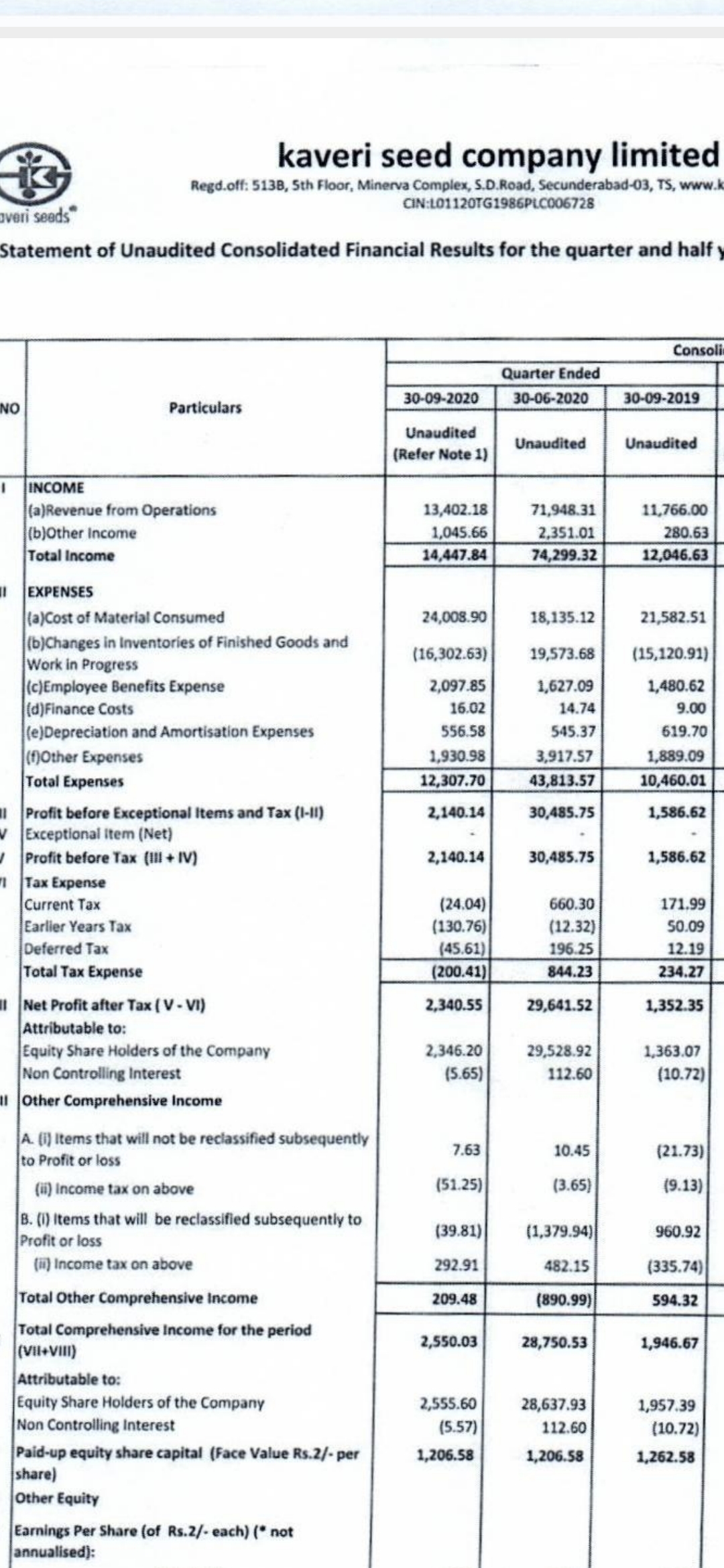

Kaveri posted it’s results and an investor presentation yesterday. Both are on the bse website

Even excluding other income and deferred taxes everything looks good considering this is usually a weak quarter and there was an increase in employee benefits(what crisis? Haha). Remember that you need to compared YoY and not QoQ due to the nature of their business.

Company has gone a long way from posting losses and poor profits in quarters apart from Q1.

Management was spot on with their commentary and guidance and have been for a few quarters now.

Few hiccups due the late showers in Oct/Nov, issues in Telangana And low pricing of maize and cotton but overall very happy with this especially since they are performing well with these factors against them and could be in for bumper quarters soon. The audit issue may never go away and may even be a non issue now but as long as their earnings keep being this positive then it’s only a matter of time before the market stands up and takes notice.

Other takeaways:

Cash In books 481 crores

Consolidated long term debt decreased from 380 crores to 130 crores

Ebitda Margins have improved substantially to 28 percent from 18 percent which is a godsend for their usual poor quarters(2,3,4) if sustainable

Inventory costs has risen(assuming this is due to the aforementioned issues regards rainfall in sept/Oct , pricing)

Receivables have increased. Hoping we get clarity on both along with the audit during concall(here’s hoping lol)

As a bonus we get rs. 4 in interim dividend. Management promised use of their cash in books for shareholders benefit since not much capex needed to maintain 10 topline and 20 percent PAT growth and This dividend is a good start.

Overall management hasn’t put a foot wrong regards guidance for this H1 and Kaveri looks set to continue growing at 20+ percent PAT with rice and maize as the growth drivers and vegetables finally contributing meaningfully. Add their cash in books and on EPS expansion alone kaveri looks good. Market won’t let these kind of earnings and growth go unnoticed without a re rating at some point either. It’s been a tough few months since June but hopefully patience prevails soon and it looks like there isn’t much downside left considering its currently trading at single digit PE.

Disc: Invested… At CMP(510) we are getting the past H1 results and information without paying a premium for it due to all the mitigating factors of the past few months(Prabhai sale especially) preventing this H1 from being priced in yet

Also, does anyone know if they conducted/are conducting a concall? If so please leave notes. Thanks

10 Likes

Kaveri Q2FY21 Concall Notes:

Was a good concall and all of the issues were addressed including the tax/legal issues. Posting my notes below.

- On tax/audit issues:

Direct question was asked about this and finally a direct answer too. No pending litigations or notice against the company confirmed. Concall was a bit inaudible here but from I understood there’s no issues anymore(there was some inaudible audio here that mentioned a case that Kaveri has filed that’s in court but they double downed on no litigations and notices VS kaveri) - On AP and Telangana:

Company dint seem too bothered about Telangana since it’s only a few districts in Telangana that cause issue with seeds and pricing competition and they lost market share to some new players . The same were well received in Maharashtra , Gujarat and a couple other states so they don’t care at all about Telangana and it won’t affect them since growth elsewhere is huge. Also, no more loss in market share expected. Infact in 2 years Telangana will pick up again. Volumes will be maintained and market share will increase all across India except the 2 districts in Telangana - On Long term Guidance:

Nothing changes for the long term guidance ie the 7 year guidance that was given ie 10 to 15 topline and 20 bottom line even if cotton stays flat or de grows - On buybacks:

Will be done next year after 12 months pass from last buyback. No capex needed as of now for growth to be maintained so it will be distributed to shareholders. Buyback over open market since they want shareholders to benefit more. - On Inventory:

Cotton sales were not as expected so inventory is up. Sales for cotton will be muted rest of year too. So inventory will continue to be high. Inventory will be used next year though so it won’t be an issue next year. Small inventory write-offs will be there as per usual. Entire year write off should be 15 to 20 crores which is the usual every year - On Maize:

Prices are low (13 to 14 instead of 20) and this year won’t be as good as last year. But rice, vegetables and wheat will cover the deficit here so overall no issue this FY. Going forward expecting it to be the preferred crop for farmers going forward. So long term no worries here. - On receivables:

No collection issues seen and most money will be collected. Can’t see any bad debt here. Better than most companies - On other income:

Investments mature and they book. Nothing untoward and historically has been similar and they’ll continue booking as and when required - On employee benefits:

First quarter benefits have been added in this quarter. Esops have been added too. Will go down back to normal next quarter - On exports:

Already exploring. Nine countries in the pipeline. Majority in Bangladesh. Pakistan affected due to covid. However export market is for the long term and over 5 years expect it to come to fruition. - Overall Market share and next quarters:

8 to 9 percent across India in hybrids.

Coming quarter will be similar to last year quarter. Even with maize cut down better placed than most in market due to product mix. H2 could be flat due to maize but could compensate with vegetables ,rice, wheat. Will grow faster than the industry next 3 to 5 years - Other expenditure decline reason:

No royalty this year. Also, travel expenses decleined in Q1 due to pandemic. But overall mix that gets covered due to other expenses. - If no good rainfall in next few years what happens in southern states?:

Improved ground water etc will help even if monsoon isn’t as good as this or last year. So sentiments have improved. But good monsoons will always be key. - Can paddy be the next big growth crop and beat cotton?:

Can beat cotton going forward. Top 3 in paddy and will grow above 25 percent next 2 to 3 years. Cotton is double paddy right now. Overall non cotton will be 58 to 60 percent soon and cotton will be 40 to 42 percent in 2 years - On vegetables:

Huge market and very positive about the future in chilli, okra and peppers. Will grow at 25 to 35 percent in vegetables. Should be at 100 crores in 5 years.

Disc: invested. I may have misheard some parts. Overall, all red flags were cleared and the audit worries don’t look present anymore. Guidance for 5 years looks good. Growth engines are in place. Cyclicality has been neutralised with product mix. Dependancy on cotton will continue to reduce. Shareholders will get benefit of the cash in hand. And it’s still at a single PE valuation

27 Likes

A question on buybacks to the management in the concall asks why they are not doing buybacks via open offer route instead of tender offer. Following is the exchange:

Moderator: Thank you. We have next question from the line of Rohan Modi from RSL Advisory.

Please go ahead.

Rohan Modi: Why we are doing the buyback in tender offer, instead of open market buyback?

Page 12 of 16

Mithun Chand: There we have stated earlier, it is a Board decision that has taken. Definitely, we

want to distribute everything to the shareholders, and I think we have done it.

Rohan Modi: But open market, there is the price for around Rs. 500 and your tender offer is

around Rs. 650, there is around 30-40% saving we can achieve by open market

buyback?

Mithun Chand: But anyhow that the shareholders will be getting benefited out of it, so that is the

different thing whether we can get it in that way, but definitely we will consider this.

We will again discuss in the Board meeting.

Buyback via tender offer is resulting in an additional outgo of Rs 150 assuming Rs 500 purchase price via open offer. Not only that, they are paying an additional buyback tax of Rs 30 @ 20% per share. They could just pay Rs 10-15 per share as dividend instead instead of paying an extra tax. Also, this premium over market rate is going to reward exiting shareholders instead of existing shareholders. Instead they could reward both exiting and existing shareholders if they could just focus on increasing book value by say hiring a capital allocator. It’s easier said than done but tender offer route for buyback seems definitely value eroding. Why pay Rs 650 when you could buy for Rs 500?

Also, the IPO price was around Rs 170. So, by buying for 650 they are paying 20% of (650 - 170) = Rs 96 as buyback tax. Company should instead just invest in mutual funds till the tax situation improves in terms of both buyback tax and tax on dividends.

1 Like

Usually id agree with you regards buybacks. But in this case it’s different. Kaveri currently has a very profitable business with good visibility for 5 years. The problem is a lot of investors have lost faith due to the issues in 2016. This buyback addresses that in a way.

- Promoters sold in the previous run up in 2015 signalling overvaluation. A buyback at 650 clearly would signal undervaluation and make the market notice.

- There could be some pressure from a lot of big investors of late for eg Prabhai. And this would give him an exit without putting price pressure on the stock which is currently in a danger zone of free falling

- It gives surety to long term investors. I know that in a few months I can tender about 10 to 20 percent of my shares at 30 percent higher if I need an exit… and keep the rest long term since I know the business prospects… so why sell now. It gives an option and makes it a bit more secure

- It gives a broad signal to the market that audit issues are behind them since why would the promoters buy at 650 if they aren’t sure about the future long term. Their livelihood runs with the company so buying at 650 means they are taking a bigger risk than us at 500. For eg Even after the concall I have lingering doubts in my mind regards this and I expect a LC every other day since we are usually the last to know. Promoters buying at 650 would give some peace of mind to me as an investor

It’s all about changing people’s perceptions about Kaveri and giving the market a signal to take notice since it’s very under the radar ATM and pain from a few years ago is still fresh in people’s mind. The risks of a bad monsoon and government involvement etc will always exist in the future but that’s the risk with any agri based stock(and resolves itself over a long time period) but currently the market is still wary about the past and so I’m fully in favour of this buyback even if it doesn’t make economic sense on paper since the business itself looks like a home run but the sentiments and memories of investors are holding the price back even with good results.

Disc: invested. Not a sebi advisor. Please do your own research

3 Likes