Seed cos challenge Maharashtra’s move to cut Bt cotton price

http://newshunt.com/share/40686705

Source: Business Standard

Sowing area under cotton declined by 18%

Good time to observe the staying power of Kaveri.

Disc: Invested and will add on further dips.

1 Like

Thanks Ishan for bringing this important issue up.

While it is addressed to Ishan, this is for the consumption of all newcomers tracking/invested in Kaveri Seeds

- I remain invested fully in Kaveri.

- Do not get swayed by media reports so easily. If you track the history of such reports over past 3 years in this thread itself - you will see that 80% of the time you will get it wrong if you go only by the reports

- If monsoons play truant, cotton is a crop that benefits the most, as it needs only a few brief showers. There are many regions in Maharashtra, AP (the largest markets for cotton seeds) where there is no alternative crop

- In times of stress, it is the smaller players who face the music the most - especially those who have lots of piled up inventory accummulated over 2-3 years or more - they will liquidate stocks at any cost

- The premium hybrid seeds in demand - folks like Kaveri - stand to benefit from the stressful situation. Farmer still wants the best hybrids for himself

- Banning sale or forcing reduced price sell hasn’t dampened sales of premium in demand hybrids in the past. Sometimes it works to their favour - as cross-border sales become rampant

Having said all that, we do not know what will happen. Things can go wrong for Kaveri too. I am willing to take that risk - despite not having the time this time to drive scuttlebutt efforts in AP & Maharashtra - as I have got busier with another passion - rural education for the underprivileged.

Disc: Invested from over 3 years; haven’t reduced holdings

@gaurav12123 - could you provide an update on on-the-ground situation at Beed, Jalna districts of Maharashtra. And collate for rest of Maharshtra too as possible, please

@OM_1417 could you do the same for AP/Telengana regions, please

8 Likes

Information from dealers/distributors in AP

by the time of regulation most of the premium seed companies sold forty percent of total quantity . Lower inventory situation along with this Price cap will lead to lower allocations to Maharashtra . Dealers anticipate almost same volume of last year . Dealers expect a tougher year - as the companies may naturally reduce commissions to distributors/ dealers . As per dealers, this year companies are focusing more on Cash collection. Volumes may be maintained or slightly better in Andhra Pradesh .As monsoon progresses more details may emerge .This is all about Ground  situation.

situation.

Having said this however Market’s main worry is not only about Maharashtra government regulation but if any other states follow similar path then? Governments too much worry on Seed cost (Five percent of total cost ) is really a big concern by leaving spurious pesticide segment which is ten times bigger market than seeds .In one state where company located , government notified to pay only 50 rupees royalty to Monsanto and now the matter is in courts .

Disc : NO holdings . Sold last year .

4 Likes

Kaveri is a classic Peter Lynch stock ie a fast grower in a slow growing market due to superior product quality thanks to superior Germplasm and R & D capabilities.

I also don’t expect atleast Telengana govt to reduce prices as it wil damage the prospects of a company promoted by a fellow Velama member but not so sure for Seemandhra.

What could be the worst case scenarios if prices are reduced? I think it will lead to consolidation and Kaveri will be a direct beneficiary at cost of other players.

1 Like

Thanks for the ground update Om Prakash.

I think that the whole issue of monsoons and price reduction in Maharashtra has been over blown.

If we look at the Met departments record of predicting rainfall, it has been mediocre at best if not abysmal. An 88% prediction for a country as large as India with very little information on spatial distribution , in my opinion has very less meaning.

Also, it is easily assumed that the farmer has one or two back up crops if the monsoon prediction is for a higher or lower rainfall. In reality a farmer is adept at growing a crop and he or she sticks with it to a very large degree. It is in very rare circumstances that they switch. The best example is that of sugar cane farmers in western UP. Before they even sow the crop, they know that they will have delayed payments from the mills. This saga has been going on for years and still the sugar cane production is higher every year. Thousands of crores of payments are pending. The farmers still continue with sugar cane as they have done it for years and are not comfortable with other crops. Sugar cane has one of the highest returns in that belt despite the delayed payments. Cotton is the same. It has the highest returns for farmers who have been growing it for years and are adept at doing it.

On price reduction we should attribute higher intelligence to the farmers. At Rs 100 reduction in price per packet and someone using 1.6 packets per acre, saves Rs 160 per acre. Seed quality and familiarity of the farmer with the seed is the single biggest factor that determines the yield. Of course water and other inputs matter but a farmer will spend this extra Rs 160 in trying to control what he surely can that is buying the seed that he is comfortable with.

Harsh industry environments from time to time are very important in any industry as it leads to the death of the fringe players and leads to consolidation. A consolidated industry structure is very important to drive higher return on capital in the long term.

Some of us who are invested in Kaveri seeds for the long term welcome this harsh environment as this is good for the surviving players in the long term.

Disc- Invested and will add on declines.

3 Likes

Any long term investment , we need to worry only when there is a ebitda de-growth. It is safer to get out and then re-enter later. This strategy I use for all my LT investments. It may look laughable but as a retail investor we are not privy to all that is happening in industry or in the company. Sometimes, the bias will fool us to look/analyse things that have changed.

In KSCL, i have not seen any ebitda degrowth so far and we can confirm the same when they announce June qtr results as it is a very important qtr for them. I exited 2 investments Sriram Transport and Suven on this principle of ebitda de-growth.

Technicaly also you can confirm, but I will not venture into that in this forum.

Posted elsewhere under a wrong head corrected now.

1 Like

Mansoon is not in full flow in Maharashtra but major cotton area jalna , beed and aurangabd have sufficient rain.

major sowing is completed in 3 district and kaveri product r in demand and definitely will show growth in beed and jalna…

will try to collect data form other parts of Maharashtra also.

5 Likes

Hi All,

Found this article in a Marathi newspaper today (18th June), but unable to trace it on other English sites.

It briefly reads/translates as follows :

- Nagpur bench of Mumbai High Court has rejected a petition by Seeds Industries Association filed against Maha Govt on reduction of cotton bt seeds packets

- The Hournable Court has noted that looking at the draught situation and farmers suicides, the Govt has taken this decision and it is well within its rights to do so.

If other State Govts take clue from this, it could spell trouble for the industry.

Thanks Advait. Got it in the times nagpur branch edition

http://www.cottonyarnmarket.net/news/news.php?action=fullnews&showcomments=1&id=16860

Kaveri seeds popularity leading to counterfeiting problem

Some key points fromthe news item appeared in The Hindu today

Annual suicide rates of farmers in rain-fed areas are directly related to increase in Bt Cotton adoption.

Suicide decreases with increasing farm size and yield but increase with the area under Bt Cotton.

The study is significant for 2 reasons. 1)Most cotton Cultivation in India is rain fed . 2) Between 2002-2010, the adoption of Bt Cotton Hybrid went up significantly to 86% to total cultivated area of Cotton in India.

Though cultivating Bt Cotton variety may be economic in irrigated areas , the costs of seed and insecticide increase the risk of farmer bankruptcy in low yield rain-fed settings.

The study challenges the common assumption in economic analyses that cotton pests must be controlled to prevent monetary losses thus encouraging Bt cotton adoption.

The annual emergence of the key cotton pest pink bollworm in spring is poorly timed to attack rain-fed cooton and large populations of pest fail to develop in non-Bt rain fed cotton. This reduces the need for Bt Cotton and disruptive insecticides.

The authors recommed that high density short season cotton could increase yields and reduce input costs in irrigated and raid fed cotton.

India is second largest country cultivating Bt Cotton and this study disproves the earlier studies which showed yield from Bt Cotton grown 19% over time.

If these finding are true and people beleive this , negative for KSCL and Monsanto. There may not be immediate reaction but negative for long term.

Please comment about how seriously we can take this study done by reputed scientists.

Kaveri seems a good pick at cmp.Nice article explaining little impact of price cut in Maharashtra on Kaveri.

The article mentions that Kaveri would be able to pass on some of the price drop to Monsanto. Now I am not too sure or optimistic on that; there is a court case going on, but no one knows the possible results.

And without courts ruling against Monsanto,I do not see any way how Kaveri could pass on price drop to Monsanto; Monsanto is the one with pricing power here and not the other way around.

And the concern is not Maharashtra alone, what if the same pricing action is followed by other states. It may lead to consolidation among players and lead to better profitability of the surviving firms; however in short term there is expected to be pain.

Cotton planting up by 20% till date compared to last year as per below.

Recent reports by CS and MOSL mention this year we may see decline in cotton acreage and lower sale of cotton seeds - this is after they had interaction with industry experts/channel checks/dealers.

Thanks. Can you please share the link?

It is open for all and not behind a paywall.

http://www.motilaloswal.com/Financial-Services/Research/Detailed-Report/Company-Updates/13260/532899

Kaveri Seed Co: Multiple headwinds to drive growth lower

30-Jun-2015

Multiple headwinds for growth in FY16

Our interaction with industry experts suggest multiple headwinds in FY16 for companies in hybrid cotton seeds business. We learn while acreage growth in cotton is down ~5% YoY and corn is down ~2%, pulses and rice have seen major growth in acreages due to strong monsoon in June and better realization to farmers for pulses (up from INR5000-6000 per quintal in FY15 to ~INR8000 per quintal currently). FY15 saw 10% of the seeds demand coming from re-sowing of seeds, which was absent in 1QFY16 due to higher-than-expected rainfall.

Lower production of seeds to impact Kaveri in FY16

Our interaction with the management indicates that lower cotton yield in FY15 impacted production of seeds in FY16. Our interaction with industry experts suggests that this has been an industry wide phenomenon. While KSCL’s production was 12m packets in FY15, it has managed to produce only 10m packets in FY16. Of the 10m production, further 5-7% has been lost due to poor quality owing to unseasonal rainfall last year bringing down net production to 9.3-9.4m packets only which are available for sale. We hence expect 2.5% volume de-growth for Kaveri in FY16, driven by lower production of seeds, lower re-sowing and some loss of sales due to pricing issue in Maharashtra.

To download the complete report, you have to wait for 48 hrs…

Disc: Invested

Monsoon plays spoilsport for cotton seed companies

1 Like

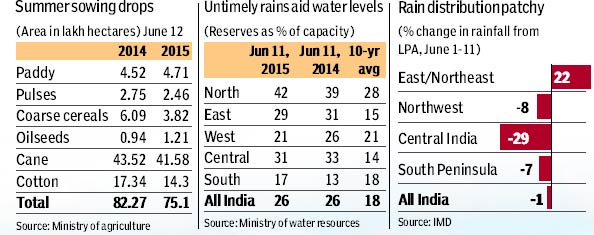

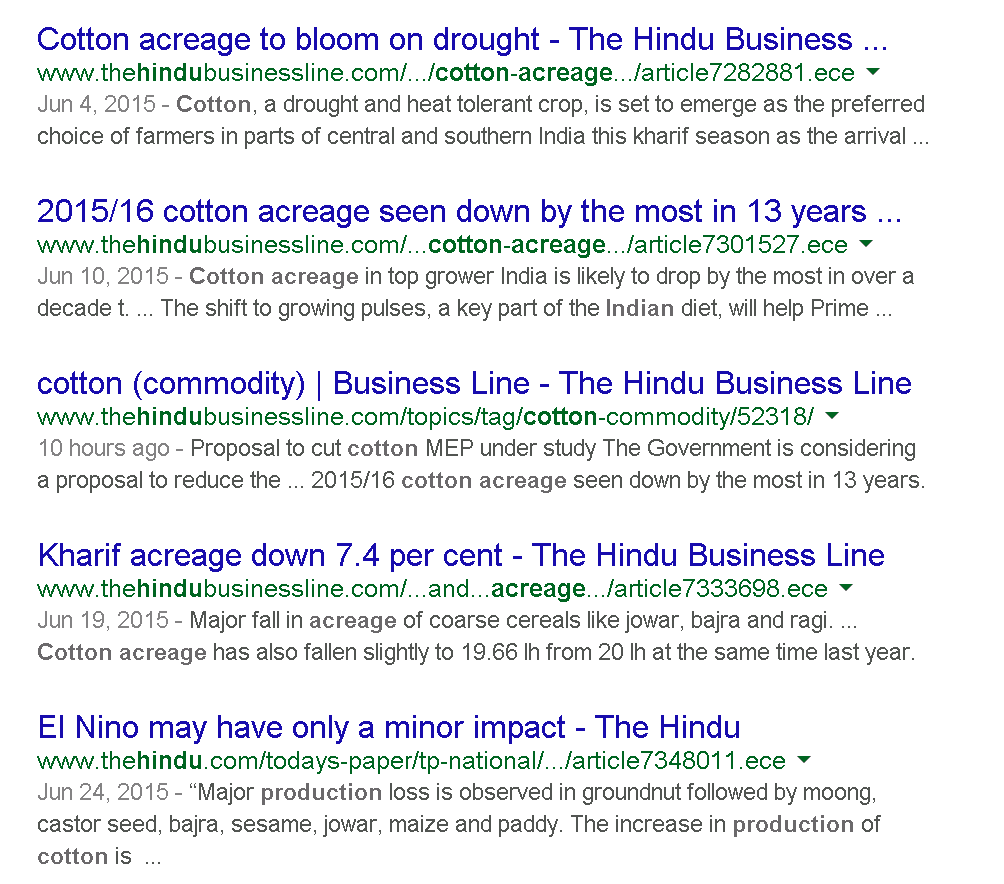

There is a flip-flop going on in newspapers about cotton/kharif acreage will go up or down. Below is the snapshot of last 1 month news from The Hindu group.

So these news items are useless I think.

Can any of the fellow boarders who are tracking Keveri Seeds for long time can help us? I would be more willing to trust their prediction based on past experience.

Thanks,

Rupesh